Home > Final Expense Insurance Cost > 30,000 Final Expense Insurance

$30,000 Final Expense Insurance: Cost & Options

A $30,000 final expense insurance policy sits at the very top of the burial insurance market. At this size, the coverage moves past simple funeral funding and into legacy-focused planning that only healthy buyers can qualify for.

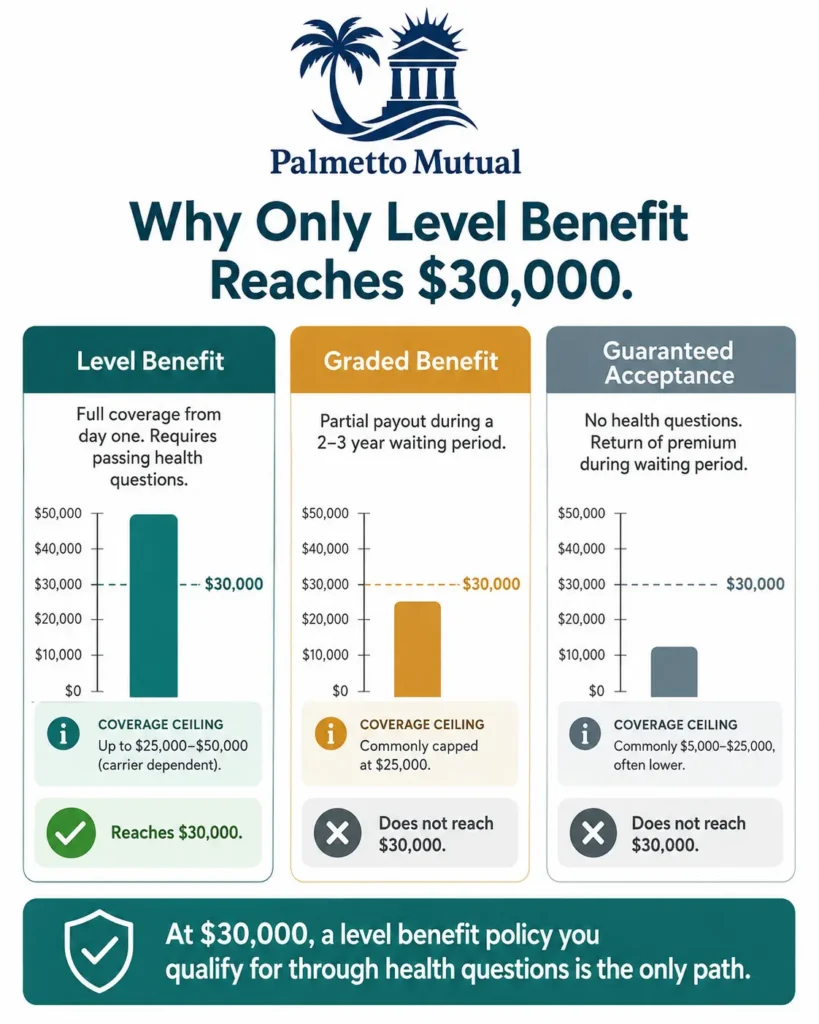

Most applicants in good health can expect a monthly premium somewhere in the range of roughly $90 to $300 or more, driven mainly by age, sex, and tobacco use, with the exact rates by age laid out in the sections below. One thing to know upfront: at $30,000 there is no graded benefit option and no guaranteed acceptance option, so the only path to this much coverage is a level benefit policy you qualify for through health questions.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a $30,000 level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

Who Should Consider a $30,000 Final Expense Plan — And Why This Much Coverage Means Healthy Buyers Only

A $30,000 policy is the point where final expense insurance stops being easy to get. At lower amounts, almost anyone can find a plan. At $30,000, the door narrows to applicants in good enough health to pass a carrier’s health questions.

This section helps you decide two things: whether you can qualify for this much coverage, and whether you actually need it.

Why $30,000 Sits Beyond Traditional Final Expense Territory

Most final expense policies are built for smaller amounts. Many carriers and well-known products cap their simplified coverage at $25,000, and some smaller whole life plans top out around $20,000.

There’s a second thing happening at $30,000. This is the coverage amount where final expense pricing starts to overlap with simplified-issue whole life from carriers that aren’t final-expense-focused at all. Many simplified issue whole life policies carry maximum death benefits between $25,000 and $50,000. So at this tier, it’s worth asking not just “which final expense plan,” but “which product category fits me best.”

Why Graded Benefit and Guaranteed Acceptance Aren’t Options at $30,000

This is the most important thing to understand before you shop. If your health doesn’t qualify you for a level benefit (full coverage from day one) policy, you generally cannot buy $30,000 of burial insurance on a single plan.

Here’s why. Graded benefit and guaranteed acceptance plans pay limited or no benefit during an early waiting period, which means the carrier is absorbing extra risk. Carriers limit that risk by capping how much coverage these plans allow.

| Policy type | How it works | Typical maximum coverage |

|---|---|---|

| Level benefit | Full death benefit from day one; requires passing health questions | Up to $25,000–$50,000 (carrier-dependent) |

| Graded benefit | Partial payout during a 2–3 year waiting period | Commonly capped at $25,000 |

| Guaranteed acceptance | No health questions; return of premium during waiting period | Commonly $5,000–$25,000, often lower |

One note on the outline here. The outline states guaranteed acceptance products “almost universally cap at $10K, $12K, or $15K.” Research shows the more common ceiling is higher — most guaranteed issue final expense policies offer between $5,000 and $25,000, with some carriers going up to $50,000. Plenty of guaranteed-issue plans do sell in the $10,000–$15,000 range, but framing $15,000 as the near-universal ceiling overstates the limit. I’ve written the section to the $25,000 figure, but flagging it so you can decide whether to adjust the outline language. The core point the outline is making still holds: at $30,000, neither graded nor guaranteed acceptance is on the table, so level benefit is the only path.

The takeaway for the reader is simple. To get $30,000 on one policy, you need to qualify for level benefit through health questions. If you can’t, you’d have to combine smaller policies or accept less coverage — both covered later on this page.

Who $30,000 of Coverage Suits Best

This amount fits people who are healthy enough to qualify and who have a real reason to carry coverage well above average funeral costs. You may be a good match if you are:

- In good health and able to answer “no” to most of a carrier’s health questions, which is what level benefit approval requires.

- Carrying meaningful debt into retirement, such as $15,000–$20,000 in medical bills, credit cards, or other obligations you don’t want passed to family.

- Hoping to leave a real inheritance for adult children or grandchildren, on top of covering your funeral.

- Living in a higher cost-of-living area or planning a premium service, where funeral costs run above the national median.

- Part of a couple where one spouse wants enough coverage to handle final costs and give the surviving partner some financial breathing room.

When $30,000 Still Falls Short

For some goals, $30,000 isn’t enough, and a different policy serves better. Burial insurance is built for end-of-life costs, not large-scale financial planning. You may have outgrown it if:

- You want one policy to cover two funerals plus a meaningful inheritance, where $40,000–$50,000 fits the goal better.

- You’re carrying large debts beyond typical final expenses, like a sizable mortgage or business liabilities.

- Your main goal is passing down wealth rather than covering a funeral. At that point, traditional whole life or term life with a larger face amount is the better tool.

When $30,000 Is More Than Single Applicants Genuinely Need

It’s just as honest to point the other direction. For many single applicants, $30,000 is more coverage than the situation calls for, and the extra premium is money that could stay in your pocket. You may be overbuying if you are:

- Planning a standard or modest service with little or no outstanding debt.

- Already holding savings that cover your end-of-life costs and provide for your family.

- Without dependents or close family who would use the leftover funds.

- On a fixed income where the $30,000 premium creates real strain that a smaller policy would avoid.

At this coverage level, overbuying is a genuine financial concern, not a minor one. The monthly difference between $30,000 and a right-sized $15,000 policy adds up over a lifetime.

When Final Expense Stops Being the Right Product Category

If you’re healthy and in your 50s or 60s, there’s a question worth asking before you buy any final expense plan at this amount: would a different kind of life insurance cost less for the same $30,000?

Final expense underwriting is fast and lenient, and you pay for that convenience. Simplified issue whole life uses limited health questions and no exam, while traditional policies usually require a medical exam but are generally less expensive because the insurer knows your full health history. For a healthy applicant who can comfortably pass a medical exam, traditional whole life at $30,000 can price noticeably lower per month than the same coverage through a final expense product.

This isn’t a reason to avoid final expense. For many seniors it’s the right fit. But at $30,000, the price gap is large enough that a healthy buyer should at least compare. The rest of this page helps you do exactly that — including an honest look at when to step outside the final expense category entirely.

What Does $30,000 Cover — From Premium Funeral Services to Family Legacy

At smaller coverage amounts, the math is about whether the policy covers the funeral. At $30,000, the funeral is almost never the question. The real question is what to do with the large amount left over.

For that reason, this section treats $30,000 as legacy planning, not funeral funding.

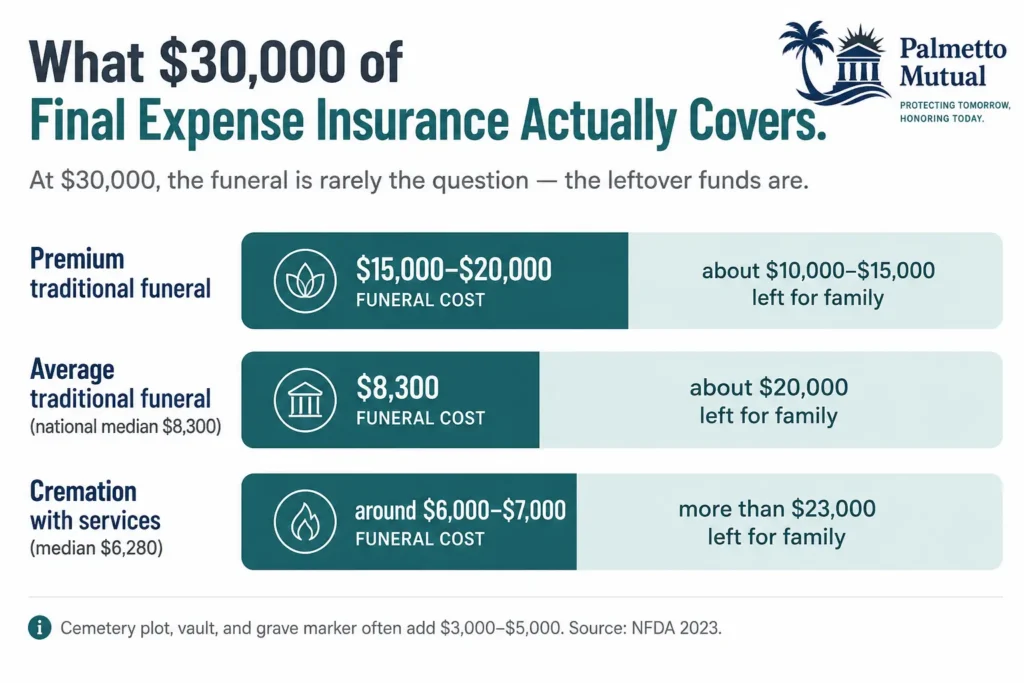

The Cost of a Premium Traditional Funeral in 2026

Start with the national benchmark. The national median cost of a funeral with viewing and burial was $8,300 in 2023, according to the National Funeral Directors Association (NFDA). Cremation with a viewing came in lower, at a median of $6,280.

Those figures don’t include everything, though. The NFDA’s median does not include cemetery costs, a monument, or a grave marker. Add a burial vault, a plot, a headstone, and a few upgrades, and a fuller traditional funeral climbs well past the median.

A premium service pushes higher still. With a custom casket, a mausoleum or upgraded plot, extended viewing, full services, and family travel, a high-end traditional funeral can reach roughly $15,000–$20,000 once cemetery and merchandise costs are layered on top of the NFDA service median. Buyers shopping at the $30,000 tier are often the ones planning exactly these kinds of upgrades.

How $30,000 Covers Any Funeral With Major Buffer Remaining

Even at the premium end, $30,000 covers the funeral and leaves a large amount behind. If a high-end service runs $15,000–$20,000, that leaves roughly $10,000–$15,000 in remaining benefit. If costs land closer to the median, the leftover is larger still.

That buffer is the real point of a policy this size. Here’s what it can realistically fund:

| Use for the leftover funds | What it can cover |

|---|---|

| End-of-life medical bills | Out-of-pocket hospital, hospice, or care costs not paid by insurance |

| Outstanding debt | Credit cards, personal loans, or other balances left behind |

| Surviving spouse support | Several months to a year of household bills during the transition |

| Family inheritance | A meaningful amount passed to children or grandchildren |

Because the death benefit is paid in cash directly to your beneficiary, they decide how to use it. The payout goes to your named beneficiary, not the funeral home, and while the intent is to cover final costs, there are no restrictions on how the money is spent.

$30,000 for Average Funeral Choices — Significant Legacy Funds Remain

If you’re planning an average or modest traditional service rather than a premium one, the leftover grows substantially. Against a median funeral near $8,300, a $30,000 policy leaves roughly $20,000 in remaining benefit.

At that gap, this is no longer funeral insurance in any practical sense. It’s an inheritance with a funeral attached.

Buyers in this position should plan deliberately. Decide who receives the leftover funds, what you want those funds to do, and whether your beneficiary designations actually match that intent. A burial insurance policy this size rewards a little estate-planning thought.

$30,000 for Cremation Buyers — Coverage Becomes Almost Entirely Legacy

For cremation, the picture is even more lopsided. A funeral with cremation runs a median of $6,280, and even a fuller cremation with memorial services rarely tops about $7,000. Against $30,000 of coverage, that leaves more than $23,000.

At that point, a cremation buyer choosing $30,000 is making a legacy decision, plain and simple. There’s nothing wrong with that — but it’s worth naming honestly.

It’s also the clearest case on this page for stepping back and asking whether final expense is even the right product. If nearly all of the benefit is inheritance rather than funeral cost, simplified-issue or traditional whole life at $30,000 may deliver the same legacy for a lower premium. That comparison is worth running before you buy.

How Families Actually Use $30,000 Death Benefits

In practice, families rarely spend a benefit this size on the funeral alone. The cash is flexible, and at $30,000 the typical use shifts heavily toward what’s left after final costs are settled. Common uses include:

- Paying off all remaining medical and credit card debt.

- Giving a surviving spouse a year or more of household expenses.

- Helping adult children with funeral travel and time off work.

- Splitting an inheritance among several beneficiaries.

- Funding college savings for grandchildren.

- Paying down a remaining mortgage balance on the family home.

The through-line is the same across all of these: at $30,000, funeral life insurance functions as a small financial cushion for the family, not just a bill-payer for the service.

$30,000 Whole Life Rates by Age (Non-Tobacco Applicants in Good Health)

These are the headline rates for a $30,000 burial insurance policy. Because graded and guaranteed acceptance plans aren’t available at this amount, this page has only two rate sections: non-tobacco here, and tobacco next.

How $30,000 Whole Life Pricing Works at the Top of the Final Expense Market

Carriers set your premium using four things: your age when you apply, your sex, your tobacco status, and your health tier. The price is locked on the day you buy, and it does not change as you age — a rate you start at 65 is the same at 85. The death benefit doesn’t shrink either.

At $30,000, there’s an extra layer. This amount sits above the standard simplified range for many carriers, so the ones that offer it tend to ask more detailed health questions and may review medical or prescription records for borderline applicants. Many no-exam final expense carriers cap coverage at $25,000 or $30,000, which means fewer companies compete at the very top of this range.

The practical effect: an applicant who sails through at $20,000 or $25,000 may be asked for a smaller amount, or declined, when applying for the full $30,000.

$30,000 Whole Life Monthly Rates by Age

The table below shows illustrative monthly premiums for a $30,000 level benefit whole life policy, non-tobacco, average health. These are representative ranges scaled from 2026 final expense rate studies built on $10,000 and $20,000 policies, not quotes from a specific carrier. Your actual rate depends on the carrier and your health answers.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $86 | $67 |

| 55 | $102 | $77 |

| 60 | $125 | $93 |

| 65 | $163 | $117 |

| 70 | $218 | $154 |

| 75 | $294 | $211 |

| 80 | $413 | $289 |

Sample monthly rates for level benefit at $30,000 of coverage, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

A word on the gap between the columns. The difference between what women and men pay is at its widest at this coverage level. Because women tend to live longer, their monthly rates are almost always lower than men’s for the same policy. At $30,000, that gap commonly runs in the range of 18–22%, which translates to roughly $40–$80 or more in monthly difference at the older ages shown above.

One regional exception is worth knowing. Montana law requires insurers to charge men and women the same rate, so women there pay closer to male pricing. Everywhere else, the gender gap above applies.

Why $30,000 Rate Variation Across Carriers Is Substantial

Few carriers compete at $30,000, and the ones that do price very differently. That makes shopping more than one carrier the single highest-leverage step in the whole process.

Two applicants with identical profiles can see $30,000 monthly rates that differ by roughly 30–60% between carriers. The reason is simple: with only a handful of companies offering this face amount, there’s less price competition pulling them toward a common number. Even within standard whole life, the spread between the cheapest and most expensive provider for the same profile can exceed hundreds of dollars per month.

Put in annual terms, the difference between the most and least competitive carrier at $30,000 commonly runs $500–$1,200 or more per year. Over a 20-year policy, that compounds to roughly $10,000–$22,000 in lifetime premium difference for the exact same coverage.

This is exactly where an independent broker helps. Because Palmetto Mutual isn’t tied to one carrier, the same application can be shopped across the companies that actually offer $30,000, rather than accepting the first quote a single carrier returns.

Why Locking In $30,000 in Your 50s or 60s Is the Strategic Decision

Because the premium is fixed for life, the age you buy at is the age you pay at forever. Waiting is expensive in two separate ways.

First, the rate itself climbs steeply. Final expense premiums roughly double between age 50 and age 70 for the same face amount, with the steepest single jump — about 44–45% — happening between ages 75 and 80. A 60-year-old who locks in $30,000 in good health keeps that lower premium for the rest of the policy’s life.

Second, and unique to this tier, waiting risks your eligibility. At $30,000 carriers apply stricter health standards, so a change in health before you apply can mean a reduced offer or an outright decline. Waiting from 60 to 70 to buy $30,000 often means a premium 80–110% higher and real underwriting risk, with a lifetime cost of waiting that can total $25,000–$45,000 or more depending on age and life expectancy.

The takeaway is straightforward: if $30,000 is the goal, buying earlier is dramatically more favorable, both on price and on the odds of qualifying at all.

Whether $30,000 Final Expense Beats Traditional Whole Life at Your Profile

For a healthy applicant in their 50s or early 60s, this is the most important question on the page — and the answer is often no.

Final expense pricing carries a premium for lenient, no-exam underwriting. You pay for that convenience whether or not your health requires it. Traditional policies usually require a medical exam but are generally less expensive because the insurer can see your full health history. For a healthy buyer who can pass an exam, traditional or simplified-issue whole life at $30,000 can price materially lower per month than a final expense product.

At this coverage amount, that gap can mean $15–$40 or more in monthly difference for the same person, which compounds to roughly $4,000–$12,000 over the life of the policy. For applicants who can comfortably qualify for traditional underwriting, that’s often too large to ignore.

None of this means final expense is wrong for you. For applicants who can’t pass full underwriting, or who value speed and simplicity, it’s a good fit. But at $30,000, a healthy buyer owes it to themselves to compare the broader life insurance market before assuming final expense is the right category.

$30,000 Whole Life Rates by Age (Tobacco Users)

Tobacco use changes the math significantly at this coverage level. This section mirrors the non-tobacco rates above, with the surcharge built in.

What Tobacco Use Adds to a $30,000 Premium

Tobacco status is one of the biggest single price factors in burial insurance. Smokers and regular nicotine users almost always pay more, with rates commonly running 30–60% higher than non-smokers of the same age. At $30,000 of coverage, that percentage turns into real dollars — often $60–$140 or more per month at the older ages, compounding heavily over the life of the policy.

What counts as “tobacco use” isn’t uniform across carriers, and the differences matter:

- Cigarettes always count as tobacco use at every carrier.

- Cigars, pipe, and smokeless tobacco are treated inconsistently — some carriers count only cigarettes, so a cigar or chew user can sometimes qualify for non-tobacco rates.

- Vaping and nicotine pouches are treated as tobacco by some carriers and not others.

- Smokeless tobacco is most often treated the same as smoking.

Look-back periods vary too. Most final expense carriers ask whether you’ve used tobacco in the past 12 months, though some look back two to three years depending on the product. At $30,000, matching to the right carrier’s definition and look-back is one of the most financially consequential decisions in the purchase.

$30,000 Whole Life Tobacco Rates by Age

The table below mirrors the non-tobacco table above, with the tobacco surcharge applied. These are illustrative monthly ranges for a $30,000 level benefit policy, tobacco rates, average health — representative figures scaled from 2026 rate studies, not quotes from a specific carrier.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $109 | $88 |

| 55 | $137 | $109 |

| 60 | $173 | $129 |

| 65 | $233 | $164 |

| 70 | $316 | $217 |

| 75 | $429 | $293 |

| 80 | $613 | $399 |

Sample monthly rates for level benefit at $30,000 of coverage, tobacco. Rates require answering health questions, and approval is not guaranteed.

Re-Rating to Non-Tobacco After Quitting — Major Long-Term Savings at $30,000

This is real money most TV-advertised products never mention. Many insurers allow a policyholder who quits to request a rate reclassification after a tobacco-free period, typically 12 to 24 months depending on the carrier. After that period, you can be reclassified as a non-smoker and pay what you would have if you’d never smoked.

At $30,000, the savings from re-rating can total roughly $9,000–$22,000 or more over the life of the policy, depending on the age you quit and your life expectancy.

That changes the decision for a tobacco-using applicant. The financial incentive to quit and re-rate is large enough to fundamentally reshape the policy’s long-term cost. It also raises a real strategic question: lock in coverage now at tobacco rates and re-rate later, or, if quitting is already underway, wait until you’ve been tobacco-free long enough to secure non-tobacco pricing from day one. There’s a tradeoff either way — applying now means coverage is in force immediately rather than leaving your family exposed while you wait.

Carrier-Specific Tobacco Underwriting Becomes Critical at $30,000

The fine print on tobacco varies enough between carriers that, at $30,000, it can swing thousands of dollars. Getting matched to the right carrier for your specific tobacco history is one of the highest-leverage moves in the whole process.

A few examples of where the dollars are:

- Look-back length. The difference between a 12-month and a 24-month look-back at one carrier versus another can decide whether you’re classified as tobacco or non-tobacco at all. At $30,000, that classification swing can mean $4,000–$10,000 or more in lifetime premium difference.

- Cigar users. Some carriers count only cigarettes as tobacco, so an occasional cigar user can qualify for non-tobacco rates with the right company. At $30,000, that match can save $1,500–$4,000 or more a year.

- Vapers. Treatment is inconsistent industry-wide, so the right carrier match matters.

- Smokeless tobacco. Most carriers treat it as tobacco use, though a small number ask only about cigarettes.

Because no single carrier’s tobacco rules fit every applicant, this is another place where shopping multiple carriers through an independent broker directly changes what you pay. Quitting for an extended period can lower rates, but the specifics are at each insurer’s discretion, which is exactly why matching the applicant to the right carrier matters so much at this amount.

What Health-Compromised Applicants Should Do When $30,000 Isn’t Available Through Standard Underwriting

If your health doesn’t qualify you for $30,000 of level benefit coverage on a single policy, you still have options — they just take a little more planning. This section walks through what to actually do, in order of what usually works best.

Why Some Applicants Will Be Declined or Reduced at $30,000

It helps to understand why this happens. Carriers raise their health standards as the face amount goes up, because their risk goes up right along with it.

Most applicants qualify for simplified issue — including those with common conditions like controlled diabetes, high blood pressure, or mild heart conditions — and get full coverage from day one. But that’s typically true at smaller amounts. The same conditions that pass cleanly at $10,000 or $15,000 can trigger a closer look at $30,000.

So an applicant with a controlled chronic condition, a recent diagnosis, a certain medication profile, a moderate heart condition, COPD, or insulin-dependent diabetes might qualify for level benefit at $10,000–$20,000 yet be declined, reduced to a lower amount, or steered toward a graded plan at $30,000. Level-benefit plans generally carry tighter underwriting than graded or guaranteed issue plans. The higher you reach, the stricter those questions get.

This isn’t a dead end. It just means the path to $30,000 may look different than a single policy.

How to Combine Multiple Policies to Reach $30,000 of Coverage

If you can’t get $30,000 on one policy, you can often reach the same total by combining two. This is a standard, legitimate approach for burial insurance.

A couple of common structures:

- A $20,000 level benefit policy from one carrier plus a $10,000 graded benefit policy from another.

- A $15,000 level plus a $15,000 graded, split across two carriers.

The idea is to take as much level benefit coverage as your health allows, then fill the gap with a graded policy that has more lenient health questions. Graded benefit plans ask some health questions but are more lenient than simplified issue, paying a reduced amount in the early years and the full benefit after two to three years.

There are real tradeoffs to know going in:

- The combined premium will be higher than a single $30,000 level policy would have cost, because part of your coverage is priced as graded.

- You qualify twice, meaning two applications and two sets of health questions.

- The policies pay out independently, each on its own terms, including any waiting period on the graded portion.

For an applicant whose health rules out a single $30,000 level policy, this approach can still get the full face amount in place through realistic underwriting. An independent broker matters here, because the two policies usually come from two different carriers. A broker with relationships across many carriers can often find a level benefit match where a single-carrier search only produced a graded or guaranteed issue result.

When Stepping Down to $25,000 or $20,000 Is the Smarter Decision

Sometimes the better move isn’t to chase $30,000 at all. For some applicants, taking a smaller single policy beats forcing the higher amount through workarounds.

$25,000 of single-policy level benefit is widely available — a $25,000 cap is common across final expense products. At that amount you stay inside one carrier’s standard range, which usually prices more efficiently and skips the complexity of managing two separate policies.

So if you’d need a graded second policy to reach $30,000, it’s worth comparing that against a clean $25,000 or $20,000 single policy. Stepping down by $5,000–$10,000 to qualify cleanly often produces a better long-term outcome than stacking policies to hit a round number. The goal is right-sizing the coverage to what you can qualify for smoothly, not hitting $30,000 for its own sake.

When to Consider a Different Product Category Entirely

There’s one more honest option, and for some applicants it’s the best one. If your real goal is leaving an inheritance or providing broad family financial protection at $30,000 — not just covering a funeral — and final expense underwriting won’t get you there, a different product may serve you better.

Simplified issue whole life policies commonly offer maximum death benefits between $25,000 and $50,000, and some of these products from non-final-expense carriers underwrite more leniently at higher face amounts than final expense does. That’s especially worth checking for applicants in their 50s and 60s with a controlled chronic condition, who may find a smoother path to $30,000 outside the final expense category altogether.

The point is to start from your goal and work backward to the right product, rather than assuming the answer has to be a multi-policy final expense workaround. A broker who can shop both burial insurance and broader simplified-issue products is in the best position to tell you which path actually fits. That’s the value of working with someone independent: the recommendation follows your situation, not a single carrier’s shelf.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.