Home > Final Expense Insurance Cost > 5,000 Final Expense Insurance

$5,000 Final Expense Insurance: Cost & Options For 2026

A $5,000 final expense insurance policy is one of the smallest burial insurance plans you can buy. It is built to help cover end-of-life costs, and it usually has one of the lowest monthly premiums among coverage amounts. It helps to know up front that $5,000 is the entry-level tier. It can fully cover a simple cremation, but it will not pay for a full traditional funeral on its own.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a $5,000 level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

Who Should Consider a $5,000 Final Expense Plan — And Why

A $5,000 plan is the smallest common tier of final expense insurance. It fits some people very well, while leaving others short. This section helps you figure out which group you fall into.

Who $5,000 of Coverage Actually Suits

A $5,000 plan works best when your costs are small or already partly covered. It tends to be a good match for these buyers:

- Seniors on a limited fixed income who want a low, steady monthly premium

- People planning a direct cremation, which costs far less than a full burial

- Anyone using $5,000 as a top-up to savings, a prepaid plan, or another policy

- Older applicants who have been priced out of higher coverage amounts

- People who want to cover one specific bill, like a final medical balance or a small debt

This lines up with who actually buys these plans. Most buyers are between 50 and 85 years old, and many live on fixed incomes.

Who Should Probably Consider More Coverage

A $5,000 plan is not enough for everyone. You may want a higher amount if any of these fit you:

- You want a traditional burial with a viewing, casket, and cemetery plot

- You are younger and in good health, so more coverage still costs little per month

- You carry meaningful debt or expect unpaid medical bills

- Your family would struggle to cover the gap out of pocket

A small premium feels good today. But a plan that leaves a large gap can shift stress onto the people you love, so it is worth being honest with yourself about the full cost.

How Family Situation Affects the $5K Decision

Your family setup changes the math more than any single number. A widowed senior whose adult children plan to pay for the service has very different needs than a single person with no one to lean on.

A few questions help here:

- Would a spouse or partner have to cover costs alone?

- Are adult children willing and able to help, or already stretched thin?

- Do you already have savings, a prepaid funeral plan, or another policy?

If others will share the cost, $5,000 may close the gap nicely. If you are the only source, sizing up is often the safer call.

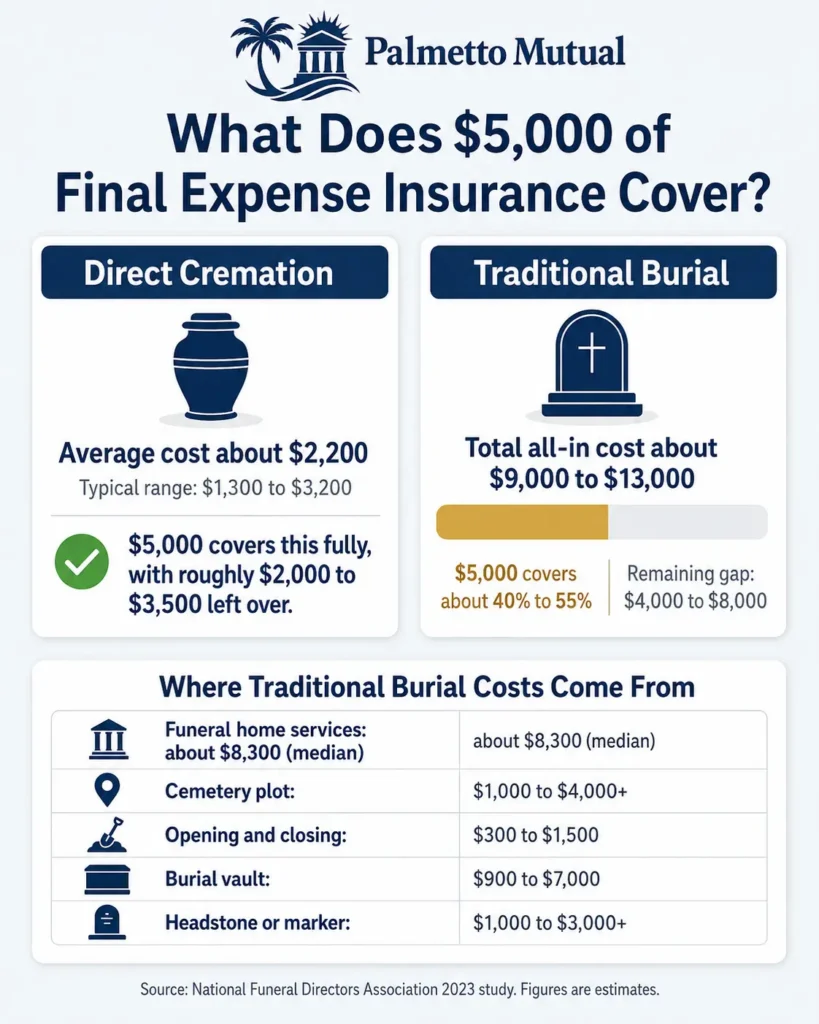

What Can $5,000 Realistically Pay For at Today’s Funeral Prices

Here is the honest reality check. We will look at what a funeral costs today and what $5,000 of burial insurance can and cannot cover.

The Current Cost of a Traditional Funeral in 2026

The clearest national number comes from the National Funeral Directors Association. The median cost of a funeral with viewing and burial was $8,300 in its most recent study

One detail matters a lot here. That $8,300 covers funeral home services only. It does not include the cemetery plot, the grave marker, or extras like flowers and an obituary

Once you add those cemetery costs, the bill climbs. Here is how the pieces stack up:

| Cost piece | What it covers | Typical figure |

|---|---|---|

| Funeral home services | Basic fee, transfer, embalming, casket, viewing, ceremony, hearse | ~$8,300 median (NFDA) |

| Cemetery plot | The grave space itself | $1,000–$4,000+ |

| Opening and closing (interment) | Digging and filling the grave | $300–$1,500 |

| Outer burial container / vault | Liner many cemeteries require | $900–$7,000 |

| Headstone or marker | The marker and its installation | $1,000–$3,000+ |

Add it up and a full traditional burial commonly lands between about $9,000 and $13,000. Adding just a vault to the NFDA figure already pushes it near $9,995, and costs run higher in pricier regions — the Northeast averages around $8,985, up to 34% more than Southern states.

What $5,000 Covers If You Choose Direct Cremation

This is where a $5,000 plan shines. Direct cremation skips the viewing and ceremony. The body is cremated soon after death, and the remains are returned to the family.

The national average for direct cremation in 2026 is about $2,200, with most families paying between $1,300 and $3,200, depending on the state.

So at this coverage level, a direct cremation leaves real money left over — often $2,000 to $3,500 — for other end-of-life costs. This is the best-case scenario for a $5,000 plan.

The Gap $5,000 Leaves for Traditional Burial

If your family wants a traditional burial, $5,000 will not cover the whole bill. Against an all-in traditional burial of roughly $9,000 to $13,000, a $5,000 payout covers about 40% to 55% of the total.

Here is that gap in plain numbers:

| All-in traditional burial | $5,000 covers | Remaining gap |

|---|---|---|

| $9,000 | ~55% | ~$4,000 |

| $11,000 | ~45% | ~$6,000 |

| $13,000 | ~38% | ~$8,000 |

That is an honest gap, not a reason to worry. Some readers will accept it deliberately because their budget only allows a small premium, and that is a fair choice when made with clear eyes. If you expect a traditional burial and want to close the gap, it is worth pricing a higher tier before you decide.

Other Things Beneficiaries Use $5K Final Expense Payouts For

The death benefit is paid in cash, straight to your beneficiary. They are not required to spend it on a funeral. They can put it toward whatever is most pressing.

Common uses include:

- Unpaid medical or hospital bills

- Credit card or other consumer debt

- A mortgage or rent payment to steady the household

- Travel for the family coming to the service

- Every day bills during a hard stretch

So even when $5,000 does not cover a full funeral, it still gives your family real flexibility during a hard time. That flexibility is a big part of why funeral life insurance appeals to people who want to leave behind something simple and useful.

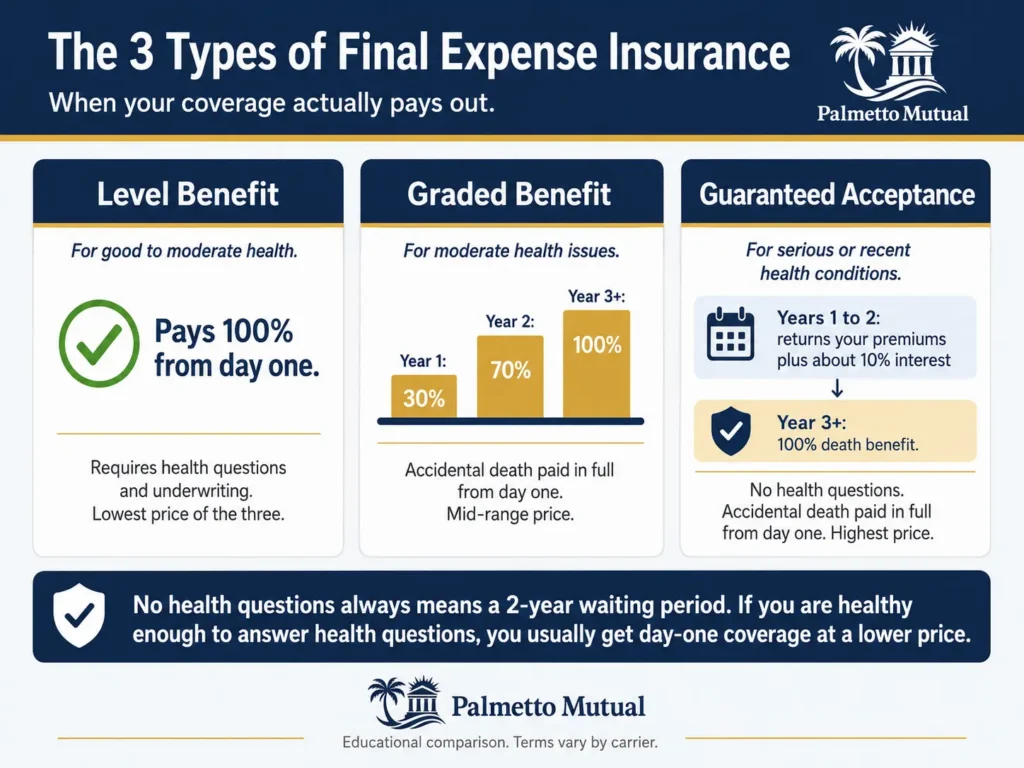

$5,000 Whole Life Policy Rates by Age (Non-Tobacco Applicants)

This is the most common applicant profile: a non-tobacco user buying a level benefit whole life plan. The rates below show what $5,000 of burial insurance typically costs each month at different ages.

How Level Benefit Whole Life Pricing Works

Level benefit is the strongest type of final expense plan. It pays the full death benefit from day one, with no waiting period.

A few things define how it is priced:

- The premium is fixed. It never goes up, no matter how old you get or how your health changes.

- The plan builds a small amount of cash value over time.

- You answer health questions and qualify through underwriting to get it.

The key point for seniors on a budget: the rate you lock in today is your rate for life.

$5,000 Whole Life Monthly Rates by Age

The table below shows representative monthly premiums for a $5,000 level benefit policy, non-tobacco, by age and sex. Women pay less than men at every age because they tend to live longer.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $17 | $14 |

| 55 | $20 | $15 |

| 60 | $23 | $18 |

| 65 | $30 | $22 |

| 70 | $39 | $28 |

| 75 | $52 | $38 |

| 80 | $71 | $51 |

| 85 | $98 | $70 |

Sample monthly rates for non-tobacco applicants at $5,000 of coverage. Applying does not guarantee approval.

Why $5,000 Whole Life Rates Vary Between Carriers

The rates above are representative, not universal. The same applicant can get very different prices from different carriers.

This happens because each carrier has its own underwriting niches and pricing strategy:

- One carrier may be easy on diabetes but strict on heart conditions, while another does the opposite.

- A carrier that wants more older applicants may price age 75 more kindly than its competitors.

- Some carriers simply run leaner and pass the savings on.

This is why comparing several carriers matters. For the same health profile, the spread between the cheapest and most expensive option can be meaningful. An independent broker shops across many carriers to find the one that views your situation most favorably.

$5,000 Whole Life Policy Rates by Age (Tobacco Users)

Tobacco use raises the price of burial life insurance. This section mirrors the one above, but for applicants the carrier classifies as tobacco users.

How Tobacco Use Affects Final Expense Pricing

Most carriers charge tobacco users meaningfully more than non-tobacco applicants — commonly 30% to 60% more for the same coverage.

Two details matter more than people expect:

- What counts as “tobacco” varies. Some carriers flag cigars, pipes, chewing tobacco, and vaping. Others only count cigarettes.

- Look-back periods vary. Some carriers ask about the last 12 months, others the last 24 months.

These differences are why the right carrier matters so much. The same person can be a “tobacco” rate at one carrier and a better rate at another, depending on how each one defines and looks back on use.

$5,000 Whole Life Tobacco Rates by Age

The table below mirrors the non-tobacco table, using the same ages and male and female columns, but with tobacco rates.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $22 | $17 |

| 55 | $27 | $21 |

| 60 | $32 | $24 |

| 65 | $40 | $31 |

| 70 | $51 | $38 |

| 75 | $68 | $49 |

| 80 | $92 | $69 |

| 85 | $130 | $107 |

Sample monthly rates for tobacco applicants at $5,000 of coverage. Applying does not guarantee approval.

Quitting Tobacco and Re-Rating

Here is something most generalist sites skip. If you quit tobacco, many carriers will move you to non-tobacco rates after you have been tobacco-free for 12 to 24 months.

This is rarely advertised, but it can mean real savings over the life of the policy:

- You usually have to apply for the new rate or a new policy, not just call and ask.

- The exact tobacco-free window depends on the carrier’s rules.

- Because the savings stretch across many years, even a modest monthly drop adds up.

If you quit after buying a policy, it is worth revisiting your coverage rather than assuming the tobacco rate is permanent. An independent broker can check whether re-rating or reshopping would lower your premium.

$5,000 Graded Benefit Policy Rates by Age

Graded benefit is the middle tier of final expense insurance. It is for people who do not qualify for level benefit but are still healthy enough to avoid the most basic plan. You get real first-day protection, just at a reduced payout in the early years.

How Graded Benefit Final Expense Works

A graded benefit plan pays out in steps during the first two years. Most carriers use a 30/70/100 schedule for natural-cause death.

Here is how that schedule works:

| Year of death (natural causes) | Amount your beneficiary receives |

|---|---|

| Year 1 | 30% of the death benefit |

| Year 2 | 70% of the death benefit |

| Year 3 and later | 100% of the death benefit |

Some carriers instead structure the early years as a return of your premiums plus interest, often around 10%. Carrier schedules vary, so the exact terms should always be checked.

Two points make graded a fair deal for the right person. Accidental death is usually paid in full from day one. And graded gives you partial coverage in year one, which is better than the two-year zero-benefit window on a guaranteed acceptance plan.

$5,000 Graded Benefit Monthly Rates by Age

The table below shows representative monthly premiums for a $5,000 graded benefit policy, by age and sex. Graded rates typically run about 15% to 30% higher than level benefit rates for the same coverage.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $20 | $17 |

| 55 | $26 | $20 |

| 60 | $31 | $24 |

| 65 | $39 | $31 |

| 70 | $54 | $41 |

| 75 | $76 | $56 |

| 80 | $114 | $83 |

Sample monthly rates for graded benefit applicants at $5,000 of coverage. Applying does not guarantee approval.

Who Typically Qualifies for Graded Instead of Level

Graded is where carriers place applicants with moderate health issues — not healthy enough for level, but not in the highest-risk group either. The exact line depends on each carrier’s rules.

Common reasons an applicant lands in graded rather than level include:

- A health diagnosis in the recent past, often within the last one to two years

- A controlled chronic condition that sits just past a carrier’s level threshold

- Certain medications that get flagged in the prescription database check

- Some heart conditions, certain COPD severity levels, or diabetes with complications

Because every carrier draws these lines differently, the same health profile can be graded at one carrier and level benefit and at another as a higher benefit. This is exactly where comparing carriers pays off.

$5,000 Guaranteed Acceptance Policy Rates by Age

Guaranteed acceptance is the final tier of burial insurance. It exists for people who cannot qualify for level or graded coverage. It is honest, real coverage, but it comes with the strictest trade-offs and the highest price per dollar.

How Guaranteed Acceptance Final Expense Works

Guaranteed acceptance asks no health questions and requires no medical exam. The carrier does not check the prescription database or the Medical Information Bureau. Approval is truly guaranteed, as long as you fall within the carrier’s age range, usually 50 to 80 or 50 to 85.

The tradeoff is a two-year waiting period:

- If you die from natural causes in the first two years, the carrier returns your premiums plus interest, often about 10%, rather than the full death benefit.

- If you die from an accident, the full death benefit is paid from day one.

- After two years, the full death benefit is payable for any cause.

This is the most expensive plan tier per dollar of coverage because the carrier accepts everyone without screening.

$5,000 Guaranteed Acceptance Monthly Rates by Age

The table below shows representative monthly premiums for a $5,000 guaranteed acceptance policy. Carrier age limits vary, so the oldest rows may not be offered everywhere. Guaranteed acceptance rates typically run about 40% to 80% higher than level benefit rates.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $31 | $22 |

| 55 | $34 | $26 |

| 60 | $38 | $30 |

| 65 | $50 | $37 |

| 70 | $59 | $45 |

| 75 | $82 | $64 |

| 80 | $113 | $104 |

Sample monthly rates for guaranteed acceptance applicants at $5,000 of coverage. Applying does not guarantee approval.

When Guaranteed Acceptance Is the Right Choice — And When It Isn’t

Guaranteed acceptance is the right choice when you genuinely cannot qualify for anything better. That includes recent serious health events, a terminal diagnosis, dialysis, or specific conditions that level and graded plans will not accept.

It is the wrong choice when you would actually qualify for a level benefit or a graded benefit, yet you are sold guaranteed acceptance. This happens through lazy underwriting, high-pressure sales, or TV-advertised products that never ask a single health question.

Here is the plain warning. If you are being told guaranteed acceptance is your only option, and no one has asked you any health questions, get a second opinion before you sign. You may qualify for a better plan at a lower price, and a broker who shops multiple carriers can tell you quickly.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.