Home > Final Expense Insurance Cost > 50,000 Final Expense Insurance

$50,000 Final Expense Insurance: Cost & Options For 2026

$50,000 is the very top of the final expense insurance market — the highest amount most carriers will offer, and an amount many companies won’t sell at all. At this level, prices vary widely by age, health, and carrier, and the underwriting is the strictest in the category. This page gives you an honest look at what a $50,000 policy costs, what it really covers, and whether final expense is even the right product for your goals. For some buyers it is, but for many others a simplified-issue or traditional whole life policy turns out to be the better and more affordable fit.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a $50,000 level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

Who Should Consider a $50,000 Final Expense Plan — And Why Most Buyers at This Level Are in the Wrong Product Category

A $50,000 policy sits at the very top edge of the final expense market. At this amount, the product stops being a simple funeral-cost plan and starts overlapping with life insurance built for much larger goals.

That overlap is the heart of this section. Before you shop for $50,000 of burial insurance, it helps to know whether you are one of the few buyers this product actually fits — or whether your search should point somewhere else.

Why $50,000 Is the Ceiling of the Final Expense Market

$50,000 is the most that any final expense carrier will offer, and only a small number of them go that high. Most final expense companies stop at $25,000 or $30,000.

The carriers that do reach $50,000 also ask the most health questions in the category. They often review medical records, check prescription history, and sometimes set up a short phone interview.

Age limits tighten at this level too. With some carriers, the full $50,000 maximum is only available up to age 55, dropping to $25,000 for applicants in their late 70s and 80s. So the full $50,000 is often only available to younger, healthier applicants.

The takeaway is simple. This is the one coverage level where final expense competes poorly against other whole life products on price and flexibility.

Why Graded Benefit and Guaranteed Acceptance Aren’t Options at $50,000

If your health is a concern, this part matters most. The “easier” versions of final expense are not sold at $50,000.

Graded benefit policies, which pay a partial amount in the first two or three years, typically cap around $25,000. A few carriers reach higher, but $50,000 of graded coverage is not something the market offers.

Guaranteed acceptance policies, which ask no health questions at all, cap even lower. Most companies cap guaranteed-issue burial insurance at $25,000, and some stop at $10,000 or $15,000.

So at $50,000, there is only one path: a level benefit policy through the strictest health screening in the final expense category. If you cannot pass that screening, you cannot get $50,000 through final expense at all. Your realistic choices become stacking smaller policies, accepting less coverage, or moving to simplified-issue or traditional whole life from a non-final-expense carrier.

Who $50,000 of Final Expense Coverage Genuinely Suits

A few buyers do fit this product at this amount. The common thread is that they choose it on purpose, not by default.

- People in good health who need speed. Final expense can approve in 24 to 48 hours, while traditional whole life often takes four to six weeks. A buyer with a time-sensitive reason may value that gap.

- People already declined elsewhere. If several traditional carriers have said no, the handful of final expense carriers offering $50,000 may be the only open door.

- Retirees with real debt and clear legacy intent who want simple beneficiary setup and fast claim payment.

- Buyers who compared the options first. Someone who weighed final expense against simplified-issue and traditional whole life and still chose it for specific features is making an informed call.

Who $50,000 of Coverage Suits in Terms of Financial Need

Product fit is one question. Dollar need is another. The financial profile that genuinely calls for $50,000 usually includes:

- $25,000 to $40,000 in outstanding debt or expected end-of-life obligations.

- Couples who want one policy to cover both eventual funerals plus a meaningful inheritance.

- Buyers with larger final wishes, such as premium services, family travel, or a big family gathering.

- Specific legacy goals like an inheritance for grandchildren, support for a family business, or help paying off the family home.

In short, $50,000 fits people whose main goal is broad family financial protection, not just funeral costs.

When $50,000 Is Still Insufficient

Some buyers reach for $50,000 thinking it covers everything, when their real goal needs far more.

If the aim is passing down lasting wealth, $50,000 is small. Goals like that are usually served better by $100,000 to $500,000 through traditional whole life or term life. The same is true for couples whose combined debt and inheritance goals run past $50,000, or anyone with a large remaining mortgage, business debt, or long-term dependent care to fund.

The honest read is this. If your goal is multi-decade family protection, $50,000 of final expense is both the wrong product and likely the wrong amount.

When $50,000 Is More Than the Buyer Genuinely Needs

The opposite mistake is just as costly. Plenty of buyers reach for $50,000 when far less would serve them well.

This includes single people without dependents, those whose savings already cover end-of-life needs, and parents whose adult children are financially independent and neither need nor want an inheritance. It also includes anyone on a fixed income where a $50,000 premium strains the monthly budget.

Overbuying here is the most consequential overbuy in the whole final expense market. The premium gap between $25,000 and $50,000 can be the difference between a comfortable retirement and ongoing money stress.

When Final Expense Is Almost Certainly the Wrong Product at $50,000

This is the most important point on the page, so it gets said plainly.

For most healthy buyers in their 50s and 60s shopping at $50,000, simplified-issue or traditional whole life from a non-final-expense carrier offers clearly better pricing for the same coverage and the same person. Simplified-issue policies are priced higher than fully underwritten coverage, and a medical exam lowers premiums for those who can pass one. Final expense sits at the more expensive end of that range because you pay extra for lenient underwriting whether you need it or not.

Across a long policy life, that convenience premium adds up to thousands of dollars. If you can comfortably pass traditional underwriting, you almost always come out ahead going that route.

So here is the direct recommendation. If you are healthy and considering $50,000 of funeral life insurance, pause and shop traditional and simplified-issue whole life first. Come back to final expense only if you have been declined elsewhere or you have a genuine need for fast approval that other products cannot meet.

What Does $50,000 Cover — Comprehensive Funeral, Major Debt Clearance, and Real Family Legacy

At lower coverage levels, the funeral is the main event. At $50,000, the funeral becomes a small slice of what the money actually does. Most of the death benefit goes to debt, family transition, and legacy.

This section walks through the real math, so you can see what $50,000 funds beyond the service itself.

The Cost of a Premium Traditional Funeral in 2026

Buyers shopping at $50,000 rarely plan an average funeral. Still, it helps to start with the national numbers and then build up.

The median funeral with viewing and burial runs around $8,300, and once you add the cemetery plot, vault, headstone, flowers, obituary, and reception, the all-in total usually lands between $11,000 and $13,000.

A premium service runs well above that. Custom casket, mausoleum entombment, extended viewing, full services, family travel, and a large reception can push the total into the $20,000 to $25,000 range. A mausoleum alone can run $4,000 to $10,000, and a private family walk-in mausoleum can cost well over $100,000.

So even a high-end funeral rarely uses more than half of a $50,000 benefit.

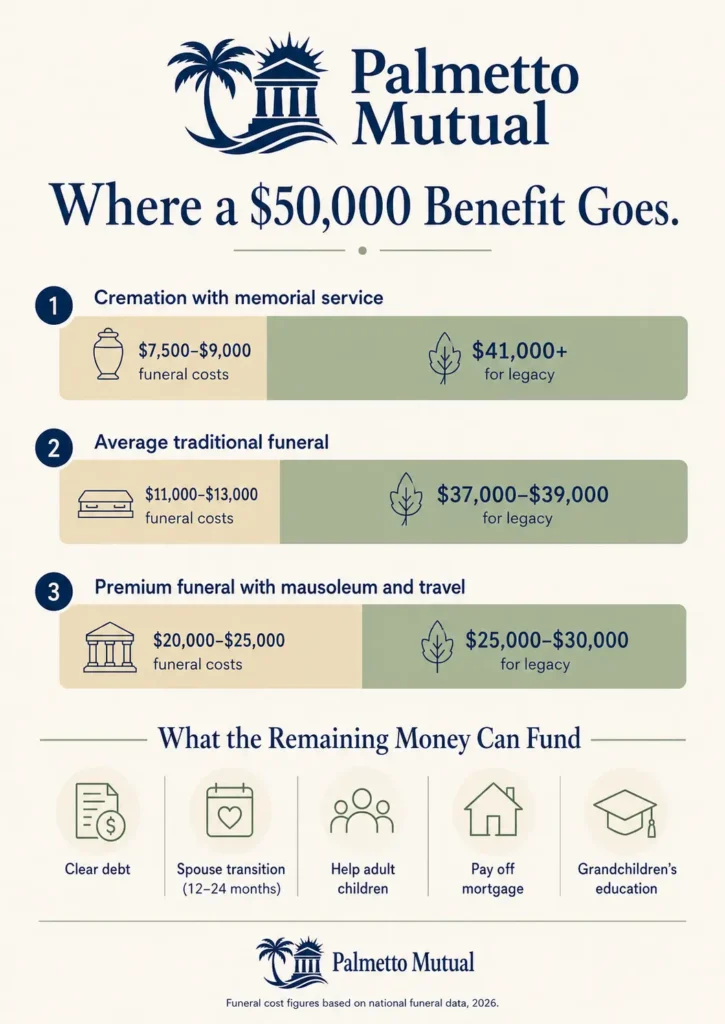

How $50,000 Funds Even the Most Premium Funeral With Major Legacy Remaining

This is the favorable case. Even with top-tier funeral choices and significant travel costs, a premium service of $20,000 to $25,000 still leaves roughly $25,000 to $30,000 for everything else.

Here is what that buffer realistically funds:

- Clearing all medical and credit card debt, with money left over.

- Giving a surviving spouse 12 to 24 months of household expenses during a hard transition.

- Helping adult children with major life events like a home down payment or education.

- Leaving meaningful inheritances split across several beneficiaries.

- Paying down a remaining mortgage on the family home.

- Starting a college fund for grandchildren.

- Providing seed money for a family business or other long-term goal.

At this level, burial insurance stops being about the funeral and starts being a family financial event.

$50,000 for Average Funeral Choices — Major Multi-Purpose Family Benefit

For buyers planning an average or modest traditional service, the gap is even wider. With an all-in funeral cost near $11,000 to $13,000, a $50,000 policy leaves roughly $37,000 to $39,000 for other purposes.

At that point, the death benefit is overwhelmingly a multi-purpose family resource. That makes beneficiary planning a real decision, not an afterthought.

Buyers here should think carefully about structure: a single beneficiary, multiple beneficiaries with set percentages, contingent beneficiaries, and whether a trust serves the goal better than a direct designation. With this much money flowing to family, getting the structure right ensures it reaches the right people in the right shares.

$50,000 for Cremation Buyers — Coverage Is Pure Legacy Planning

For cremation-focused buyers, the gap is dramatic. A cremation with a memorial service typically totals between $7,500 and $9,000 once you include an urn, stationery, and a celebration of life.

That leaves more than $40,000 of a $50,000 policy untouched by end-of-life costs. At this point, the purchase is not really about final expenses at all. It is a pure legacy decision.

And this needs to be said plainly. A cremation-focused buyer shopping at $50,000 is usually better served evaluating traditional whole life, simplified-issue whole life, or even term life built for legacy goals — not final expense. Final expense is rarely the right structure when almost none of the benefit goes toward the funeral.

How Families Actually Use $50,000 Death Benefits

The death benefit is paid in cash, with no strings attached, and the family uses it however they need. At $50,000, the real-world pattern is heavily legacy-focused.

Families most often use the money to:

- Clear all remaining family debt at once.

- Carry a surviving spouse through one to two years of household expenses.

- Support adult children through major milestones and expenses.

- Leave inheritances across several beneficiaries.

- Fund grandchildren’s education.

- Pay off the remaining balance on the family home.

- Provide seed capital for a family business.

- Finish a financial goal the deceased had been working toward for years.

The funeral is part of the picture, but at this coverage level it is rarely the largest part.

$50,000 Whole Life Rates by Age (Non-Tobacco Applicants in Good Health)

These are the rates that matter most to a healthy buyer shopping at the top of the final expense market. Because graded and guaranteed-issue products are not sold at $50,000, this is one of only two rate tables on the page.

The numbers below are for non-tobacco applicants in good health. Tobacco rates appear in the next section.

How $50,000 Whole Life Pricing Works at the Absolute Ceiling of the Final Expense Market

Carriers set your premium using four things: your age when you apply, your gender, your tobacco status, and your health tier. Once set, the premium is locked. These are whole life policies with locked-in rates, so what you pay at 65 is what you pay at 85, and the monthly cost never increases.

$50,000 is the maximum face amount in the category, and only a limited number of carriers compete there. They also apply the strictest health screening in final expense, often reviewing medical records and prescription history.

Age limits are a real factor at this amount. With some carriers, the $50,000 maximum is only available up to age 55 and drops to $25,000 by the late 70s and 80s. An applicant who qualifies easily at $25,000 may be offered less, or declined, when asking for $50,000.

$50,000 Whole Life Monthly Rates by Age

The table below shows estimated monthly premiums for $50,000 of level benefit whole life, non-tobacco, in good health.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $141 | $109 |

| 55 | $167 | $126 |

| 60 | $206 | $152 |

| 65 | $270 | $193 |

| 70 | $361 | $254 |

| 75 | $488 | $350 |

| 80 | $686 | $480 |

Sample monthly rates for level benefit at $50,000 of coverage, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

The gender gap is wider at this coverage level than at any other. Women pay less than men because longer average life expectancy means lower risk to the insurer. At $50,000, that difference can mean a meaningful monthly gap, especially at older ages.

Why $50,000 Rate Variation Across Carriers Is Extreme

This is where shopping pays off the most in the entire final expense market. With only a few carriers competing at $50,000, the spread between the cheapest and most expensive can be large.

Two people with identical profiles can see very different monthly rates depending on which carrier they land with. An independent agency with access to many carriers can match a client to the company most likely to approve them at the best price, which captive agents representing a single company cannot do.

Because the dollar amounts are large at $50,000, a single percentage difference in rate translates into hundreds of dollars a year, and thousands over the life of the policy. At this level, carrier shopping is the highest-leverage decision in the whole purchase.

Why Locking In $50,000 in Your 50s Is the Strategic Decision

Premiums rise with every year you wait, and the increase is steep at older ages. The sharpest jump tends to happen between ages 75 and 80, where average rates climb more than 40 percent in a single five-year span.

Buying in your 50s locks in a lower rate for life. As a general rule, premiums rise roughly 8 to 10 percent for every year you wait, so buying earlier almost always wins.

There is a second risk to waiting at $50,000. Because these carriers screen health tightly, a change in health can move you from “approved” to “declined” at this amount. Waiting risks not just a higher price, but losing access to $50,000 of coverage entirely.

Why $50,000 Final Expense Almost Always Loses to Traditional Whole Life

This bears repeating at the rate table, because this is where the cost gap becomes concrete. For nearly all healthy buyers in their 50s and 60s, traditional or simplified-issue whole life from a non-final-expense carrier prices better at $50,000.

The reason is structural. Final expense charges extra for lenient, no-exam underwriting. Premiums are lower when you take a medical exam, and simplified-issue policies cost more precisely because the insurer knows less about your health.

A concrete example shows the gap. One carrier quoted a healthy 60-year-old man about $55 a month for up to $10,000 of its final expense product, versus about $34 a month for up to $50,000 of its traditional life product. The same person paid less for five times the coverage by going the traditional route.

So the recommendation here is direct. If you are healthy and looking at a $50,000 final expense rate, pause and shop traditional and simplified-issue whole life first. Return to final expense only if you have been declined elsewhere, or you have a genuine need for fast approval that traditional products cannot meet.

$50,000 Whole Life Rates by Age (Tobacco Users)

Tobacco use raises the cost of burial insurance at every age, and the dollar impact is largest at $50,000. This section mirrors the non-tobacco table so you can compare side by side.

What Tobacco Use Adds to a $50,000 Premium

The tobacco surcharge in final expense is fairly consistent across the market. The smoker surcharge runs roughly 30 to 50 percent over the non-tobacco baseline, and about 95 percent of carriers apply it to any tobacco or nicotine use within the past 12 months.

At $50,000, that percentage becomes real money. A 30 to 50 percent surcharge on a large premium can add well over $100 a month at older ages, compounding across the life of the policy.

Carriers also define “tobacco” differently. Most carriers price cigarettes, cigars, pipe, smokeless, and vaping the same way. But some treat occasional cigar or pipe use more leniently. A few top-rated insurers will classify occasional cigar use — fewer than about 12 per year — as non-smoker, which can save 40 to 60 percent compared to smoker rates.

Look-back periods vary too. Most final expense insurers ask about tobacco use in the past 12 months, though some look back two to three years. With only a few carriers offering $50,000, that variation can decide whether you qualify as a non-smoker at all.

$50,000 Whole Life Tobacco Rates by Age

Estimated monthly premiums for $50,000 of level benefit whole life, tobacco rates.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $179 | $145 |

| 55 | $227 | $181 |

| 60 | $286 | $214 |

| 65 | $387 | $271 |

| 70 | $524 | $360 |

| 75 | $712 | $487 |

| 80 | $1019 | $663 |

Sample monthly rates for level benefit at $50,000 of coverage, tobacco. Rates require answering health questions, and approval is not guaranteed.

Re-Rating to Non-Tobacco After Quitting — Major Long-Term Savings at $50,000

There is real money to be saved by quitting, but it helps to understand exactly how that saving works, because it is easy to get wrong.

A final expense policy is locked at issue. Insurers do not re-check your tobacco status during the life of the policy, and they do not lower your rate for lifestyle changes after the policy is issued — the premium stays locked. So quitting does not automatically convert an existing tobacco policy to non-tobacco pricing.

The savings come a different way: by re-applying. After 12 months tobacco-free, you can qualify for non-smoker rates, which may save thousands of dollars over the life of the policy. In practice, that means shopping a new non-tobacco policy once you pass the 12-month mark and replacing the old one if the new rate is lower.

At $50,000, the gap between tobacco and non-tobacco pricing is wide enough that this is worth doing the math on. This is genuine money most TV-advertised products never mention. The catch is timing: you need to be tobacco-free for at least 12 months to qualify for non-smoking rates. An independent broker can compare your locked-in tobacco premium against a fresh non-tobacco quote and tell you whether switching saves money.

Carrier-Specific Tobacco Underwriting at $50,000

This is the most granular underwriting detail on the page, and at $50,000 it carries the highest dollar stakes. The difference between a 12-month and a 24-month look-back at one carrier versus another can decide whether you are rated tobacco or non-tobacco.

A few patterns hold across the market:

- Cigarettes always count. Even a single cigarette in the past year means smoker rates, regardless of how much you smoke.

- Occasional cigar or pipe use is the main exception. A small number of carriers will rate light cigar use as non-tobacco, which is a large saving at this coverage level.

- Vaping is treated inconsistently from carrier to carrier.

- Smokeless tobacco is almost always rated as tobacco. Most carriers price smokeless the same as cigarettes.

Because only a few carriers compete at $50,000, the room to shop your specific tobacco history is narrower than at lower coverage amounts. That makes matching with the right carrier — ideally through an independent broker who knows each company’s tobacco rules — one of the highest-value steps in the whole process.

What Health-Compromised Applicants Should Do When $50,000 Isn’t Available Through Standard Underwriting

If your health keeps you from qualifying for $50,000 of level benefit coverage, you are not out of options — but the right move is usually not to force final expense to do something it isn’t built for. This section walks through what actually works.

The honest summary up front: at $50,000, applicants with health concerns are often better served by a different product entirely.

Why Most Health-Compromised Applicants Will Be Declined at $50,000

The carriers that offer $50,000 of funeral life insurance apply the strictest screening in the category. That is by design. Their risk sits in a small number of large policies, so they underwrite those policies tightly.

The result is that conditions which are easily approved at lower amounts can lead to a decline at $50,000. Higher-risk conditions such as congestive heart failure or COPD are especially hard to place at this amount. The same applicant who clears underwriting at $15,000 or $25,000 may be turned down at $50,000.

There is good news inside this, though. Final expense underwriting is not uniform — some carriers are more lenient with conditions like diabetes and COPD, and being declined or rated by one company does not mean every company will say no. A decline at one carrier is a reason to shop, not to give up.

How to Combine Multiple Policies to Reach $50,000 of Coverage

One workaround is stacking smaller policies from different carriers to reach $50,000 in total. It can work, but you should understand the tradeoffs before going this route.

The typical approaches look like this:

- A $25,000 level benefit policy from one carrier plus a $25,000 graded policy from another.

- A $30,000 level plus a $20,000 graded across two carriers.

- Three smaller policies if your health requires it.

The catch is cost and complexity. Combined premiums usually run meaningfully higher than a single $50,000 level policy would, you go through qualification more than once, and each policy pays out on its own terms. Some graded products also limit the first-two-year payout to around 110 percent of premiums paid before the full benefit becomes available.

For most people, stacking is the most expensive path to $50,000 — and usually a sign that a different product fits better.

When Stepping Down to $25,000 or $30,000 Is Almost Always the Smarter Decision

Before chasing $50,000 through workarounds, it is worth asking whether you truly need the full amount on a single policy. For most applicants, a smaller single policy is the smarter call.

$25,000 of level benefit burial insurance is widely available and prices efficiently. Moving from $25,000 to $30,000 of coverage often adds only a few dollars a month. Clean single-policy coverage at $25,000 to $30,000 avoids the cost and hassle of juggling multiple policies.

Stepping down through one straightforward policy almost always produces a better long-term outcome than forcing $50,000 through combinations. If you genuinely need the full $50,000 and can’t qualify, that is the signal to look at non-final-expense products instead.

Why Simplified-Issue Whole Life Is Usually the Right Path Instead

This is the honest recommendation for most health-compromised buyers at this level. If your real goal is leaving an inheritance or providing broad family protection at $50,000, and you can’t qualify for level benefit final expense, a no-exam whole life policy from a non-final-expense carrier is usually the better path.

These products often underwrite more flexibly at higher face amounts. Simplified policies do accept people with pre-existing conditions, including moderate-to-high-risk ones, though the most severe conditions remain hard to place. They also reach well past final expense limits, with many policies offering death benefits between $25,000 and $50,000, and some carriers going higher.

Some carriers will issue $50,000 of this coverage to an applicant who would be declined for $50,000 of dedicated final expense, often at competitive rates. For most health-compromised buyers at $50,000, this is the dominant correct answer, and final expense workarounds should be the last resort.

When Traditional Whole Life or Term Life Is the Right Product Category

The deepest version of this honesty applies when the goal isn’t really final expense at all. If you are trying to transfer wealth across generations, protect a business, or provide multi-decade family support, the right answer is almost certainly a product built for that purpose.

At $50,000, many buyers are not shopping for funeral coverage in the traditional sense — they are shopping for life insurance to meet a broader family goal. The same products that handle final expenses can also serve income replacement or legacy goals, and the right fit depends on age, health, budget, and goals.

Clarifying the underlying goal usually reveals the product. Term life provides more coverage for a lower price for those still relatively healthy, while final expense is permanent and easier to qualify for but offers lower coverage. If your goal is large and long-term, a properly structured traditional whole life or term approach will serve you far better than final expense ever could.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.