Home > Final Expense Insurance Cost > 20,000 Final Expense Insurance

$20,000 Final Expense Insurance: Cost & Options

A $20,000 final expense insurance policy is a small whole life plan built to cover funeral costs and then some. For most applicants in their 60s and 70s, monthly premiums fall somewhere in the range of roughly $50 to $150, depending on age, gender, health, and tobacco use. This is the “extra cushion” tier of burial insurance: $20,000 fully covers a traditional funeral in any part of the country and still leaves a meaningful buffer for medical bills, debts, family expenses, or even a small inheritance. At this coverage level, the conversation shifts from simply paying for the funeral to protecting the family financially.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a $20,000 level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

Who Should Consider a $20,000 Final Expense Plan — And Why Some Families Choose the Extra Cushion

A $20,000 policy is the point at which final expense insurance starts doing more than just paying for a funeral. At smaller amounts, the money is mostly spoken for before it arrives. At $20,000, there is room left over once the funeral is paid. This section helps you decide whether that extra room is worth the higher premium, and whether you are really shopping for funeral protection or for something broader.

Why $20,000 Appeals to Buyers Who Want Real Financial Protection

A traditional funeral with a viewing and burial runs around $8,300 by the national median, and closer to $10,000 to $12,000 once you add a vault, a cemetery plot, and a headstone. A $20,000 burial insurance policy covers all of that with thousands of dollars to spare.

That leftover money is the whole point of this tier. Even in higher-cost parts of the country, $20,000 covers the funeral in full and still leaves a real cushion behind.

At this level, buyers stop worrying about the funeral being underfunded. The question changes from “will this be enough?” to “what else can this money do for my family?” That shift is why many people decide the extra coverage is worth the added cost.

Who $20,000 of Coverage Suits Best

This amount fits some buyers better than others. The people who get the most value from $20,000 of final expense coverage usually share a few traits.

- Applicants in high-cost regions, where a full traditional funeral can run $13,000 to $16,000 once cemetery costs are included.

- Those carrying $5,000 to $10,000 in outstanding debt or expected medical bills.

- Retirees who want the death benefit to genuinely help their family, not just break even on the funeral.

- Applicants with adult children who would otherwise chip in for funeral costs.

- Buyers in their 60s and 70s who can comfortably afford the premium and want solid protection without stretching to $25,000 or more.

If two or three of these describe you, $20,000 is likely a sensible target.

When $20,000 Still Falls Short

Honesty runs both directions, so here is where this amount may not be enough. Some situations call for more coverage than $20,000 can provide.

- Couples who want a single policy to cover both eventual funerals. Two funerals will outrun $20,000 in most regions.

- Applicants with significant debts, such as a large mortgage balance, a business obligation, or heavy credit card debt.

- Those planning premium services, like mausoleum entombment, a custom casket, or a multi-day service with travel for extended family.

- Buyers who want to leave a meaningful inheritance on top of covering end-of-life costs.

If your goal is broad financial protection rather than just final expenses, a larger policy may serve you better.

When $20,000 Is More Than You Actually Need

The reverse is also true. For some buyers, $20,000 is more coverage than the situation calls for, and the extra premium is money that could stay in their pocket.

- Single applicants planning a direct cremation or a simple traditional service in a lower-cost region.

- Those with savings already set aside for final expenses.

- Applicants whose adult children have said they will handle the costs without insurance.

- Seniors on a fixed income, where the jump in premium from $15,000 to $20,000 creates ongoing budget strain.

The right amount is the one that matches your real costs and your budget, not the largest one you can qualify for.

What Does $20,000 Cover at Today’s Funeral Prices — Burial, Cremation, and Everything In Between

At smaller coverage amounts, the central question is whether the policy will stretch far enough. At $20,000, that worry mostly disappears. The useful question becomes what the leftover money can do once the funeral is paid for. This section walks through the real numbers, region by region and service by service.

The True Cost of a Traditional Funeral in 2026 — Including Premium Options

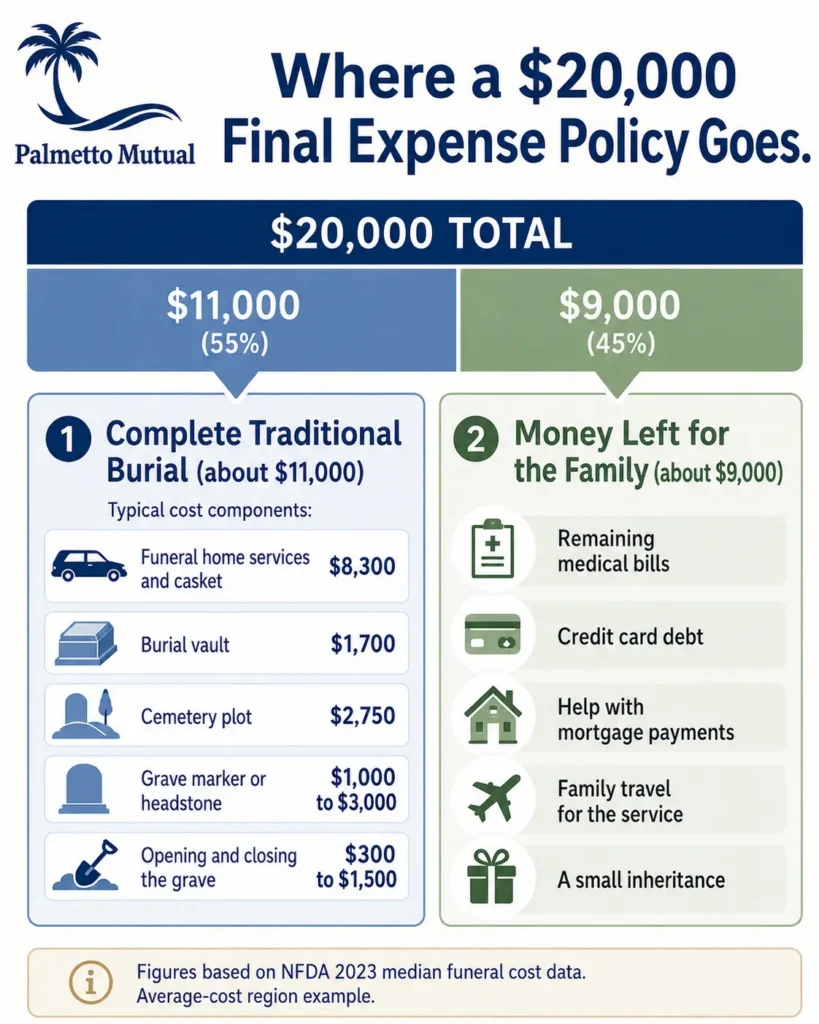

The most recent national figures put a funeral with viewing and burial at a median of $8,300. That figure covers the funeral home’s services and casket, but not the cemetery.

Once you add the items families almost always need, the total climbs. Here is how a complete traditional burial typically adds up.

| Cost component | Typical range |

|---|---|

| Funeral home services and casket (NFDA median) | $8,300 |

| Burial vault | adds about $1,700 (brings total near $9,995) |

| Cemetery plot | $2,750 average |

| Grave marker or headstone | $1,000–$3,000 |

| Opening and closing the grave | $300–$1,500 |

Put together, a complete traditional burial commonly lands in the $10,000 to $14,000 range in average-cost areas. Premium choices push it higher. A custom casket can reach $10,000 on its own, and mausoleum entombment often starts around $4,000 to $5,000 and climbs from there. Buyers who want extended viewings, multiple service locations, or upscale merchandise can reach $14,000 to $18,000 even outside the priciest regions.

How $20,000 Covers a Traditional Funeral With Substantial Buffer

In an average-cost region, $20,000 of funeral life insurance pays for the entire traditional burial and leaves a sizable amount behind. If a complete burial runs $10,000 to $12,000, the buffer is roughly $8,000 to $10,000.

That leftover money is real, and families put it to practical use. Common uses include:

- Clearing the medical bills left over from end-of-life care.

- Paying off a meaningful chunk of credit card debt.

- Helping a surviving spouse cover mortgage payments during the transition.

- Funding family travel and time off work for the funeral.

- Covering small estate-related expenses, like filing fees or account closures.

The death benefit is paid in cash to the beneficiary, so the family decides how to spend it.

$20,000 in High-Cost Regions — Still Comfortable, Still With Buffer

The picture holds up even where funerals are most expensive. In Hawaii, New York, California, Massachusetts, and Connecticut, a complete traditional burial often runs $13,000 to $16,000. Some New York City and San Francisco metros run higher still.

Even at the top of that range, $20,000 covers the funeral and leaves roughly $4,000 to $7,000.

| Region type | Complete traditional burial | Buffer left from $20,000 |

|---|---|---|

| Lower-cost (South, Midwest) | $7,000–$9,000 | $11,000–$13,000 |

| Average-cost | $10,000–$12,000 | $8,000–$10,000 |

| High-cost (Northeast, West Coast) | $13,000–$16,000 | $4,000–$7,000 |

This is the coverage level where region stops being the deciding factor. No matter where you live, $20,000 gives you full funeral coverage with cushion to spare.

$20,000 for Cremation Buyers — Coverage Plus Family Inheritance

For cremation buyers, $20,000 is far more than the end-of-life costs alone require. A cremation with a full memorial service has a national median of about $6,280, and even an upscale cremation with viewing and service rarely tops $7,000 to $9,000.

That leaves $13,000 or more available for other purposes.

At this point, a cremation buyer should make a conscious choice. You are either buying funeral coverage with a large amount of overhead built in, or you have shifted into modest legacy planning, where the policy is partly meant to leave money behind. Both are perfectly valid. The key is to decide on purpose rather than by accident, so the coverage amount matches your actual intent.

Common Uses for the $20,000 Death Benefit Beyond Funeral Costs

Because the death benefit arrives as cash, the family is free to use it however the moment requires. At the $20,000 tier, that use commonly reaches well past the funeral itself.

- Clearing all remaining final medical bills.

- Paying off credit card balances in full.

- Giving a surviving spouse several months of household expenses during the transition.

- Supporting adult children with travel and time off for the service.

- Leaving a small but meaningful inheritance for grandchildren.

This flexibility is a big part of why families choose $20,000 of burial insurance over smaller amounts. The funeral is handled, and there is still something left for the people who remain.

$20,000 Whole Life Rates by Age (Non-Tobacco Applicants in Good Health)

This section covers the most common buyer: a non-tobacco applicant in reasonably good health applying for level benefit coverage. These are the lowest rates available in the final expense market, and they are locked for life once the policy is issued.

How $20,000 Whole Life Pricing Is Structured

Carriers set your premium using four inputs: your age when you apply, your gender, your tobacco status, and your health tier. Once the policy is issued, that premium never changes for the rest of your life.

A $20,000 policy sits near the top of the simplified-issue sweet spot. It still prices competitively, but some carriers ask a few extra health questions at this amount, and a small number may request medical records for borderline applicants.

The takeaway is simple. At $20,000, you are still in straightforward, simplified-issue territory for most carriers, but the health questions can be slightly stricter than at $10,000.

$20,000 Whole Life Monthly Rates by Age

The table below shows illustrative monthly premiums for a $20,000 level benefit whole life policy at non-tobacco rates. Figures are scaled and rounded from current Mutual of Omaha Living Promise Level rates and cross-checked against market data.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $59 | $46 |

| 55 | $69 | $53 |

| 60 | $85 | $63 |

| 65 | $110 | $79 |

| 70 | $147 | $104 |

| 75 | $197 | $142 |

| 80 | $277 | $194 |

Sample monthly rates for level benefit at $20,000 of coverage, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

One pattern stands out at this coverage amount. The gap between male and female rates is real and widens in dollar terms as you age. Women typically pay 15% to 20% less than men for the same coverage. At $20,000, that percentage turns into a meaningful monthly difference. A 75-year-old man pays roughly $40 more per month than a woman of the same age, which adds up over the life of the policy.

How $20,000 Rates Vary Significantly Across Carriers

Carrier shopping matters more at this amount than most buyers realize. Two applicants with identical profiles can see $20,000 rates that differ by 25% to 50% from one carrier to the next.

At this coverage level, those percentages turn into serious money. The spread between the most and least competitive carrier commonly runs $300 to $700 or more in annual premium for the same coverage.

That difference is not a one-time gap. You pay it every year for the life of the policy. This is why working with an independent agency that compares multiple carriers, rather than buying from a single brand seen on TV, is the difference between an affordable policy and years of overpaying.

Why Locking In $20,000 Earlier Pays Off Substantially

Because rates are based on your age when you apply, every year you wait raises the price of the same coverage. The premium you lock in today is the premium you keep for life.

The jump from your 60s to your 70s is steep. Final expense rates roughly double between age 50 and 70, and the 60-to-70 step alone commonly runs from about 60% to well over 100% higher, depending on carrier and gender. Waiting also risks a health change that pushes you out of level benefit and into a higher-priced tier.

Here is what the cost of waiting looks like at this coverage amount.

| Buy $20,000 at | Female (monthly) | Male (monthly) |

|---|---|---|

| Age 60 | $63 | $85 |

| Age 70 | $104 | $147 |

Over a typical retirement, the extra premium from waiting can total many thousands of dollars, before even accounting for the risk of a health downgrade. At $20,000 of burial insurance, the math clearly rewards buying earlier rather than later.

$20,000 Whole Life Rates by Age (Tobacco Users)

Tobacco use raises the cost of final expense insurance, and at $20,000 the dollar difference is large. This section covers what tobacco adds, what the rates look like, and how quitting can lower your premium down the road.

What Tobacco Use Adds to a $20,000 Premium

Tobacco users pay a surcharge that typically runs 30% to 60% above non-tobacco rates for the same coverage. At $20,000, that surcharge is no small thing.

At older ages, the gap reaches $40 to $80 or more per month. Over the life of the policy, that compounds into thousands of dollars.

Carriers also define “tobacco user” differently, which matters more than most buyers expect.

- Cigarettes always count as tobacco use, at every carrier.

- Cigars, pipes, vaping, and smokeless tobacco are treated inconsistently. Some carriers count them, some do not.

- Look-back periods vary, usually from 12 to 24 months tobacco-free to qualify for non-tobacco rates.

Because of these differences, matching your specific tobacco history to the right carrier can save real money at this coverage amount.

$20,000 Whole Life Tobacco Rates by Age

The table below mirrors the non-tobacco table, at tobacco rates. Same ages, same male and female columns.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $74 | $60 |

| 55 | $93 | $74 |

| 60 | $117 | $88 |

| 65 | $157 | $111 |

| 70 | $212 | $146 |

| 75 | $287 | $197 |

| 80 | $410 | $268 |

Sample monthly rates for level benefit at $20,000 of coverage, tobacco. Rates require answering health questions, and approval is not guaranteed.

Compared with the non-tobacco table, these rates run roughly 40% to 50% higher at most ages, which is consistent with the surcharge range carriers apply.

Re-Rating to Non-Tobacco After Quitting — Substantial Savings at This Tier

Here is something most TV-advertised products never mention. Many carriers will re-rate you to non-tobacco rates once you have been tobacco-free for the required period, usually 12 to 24 months.

At $20,000 of coverage, that re-rate is worth a lot. Depending on your age when you quit and how long you live, the savings can total many thousands of dollars over the life of the policy.

That is genuine money on the table. The financial reward for quitting is large enough at this coverage amount that it can change the decision for a tobacco-using buyer who is weighing whether to lock in a policy now or wait until they have quit. In most cases, securing coverage now and re-rating later is the safer path, because waiting risks a health change that could raise the price more than tobacco ever did.

Carrier-Specific Tobacco Rules That Matter at $20,000

The fine print on tobacco varies carrier to carrier, and at this coverage amount the differences carry real dollar weight.

- Look-back periods differ. Some carriers use a 12-month window, others 24 months. For someone who quit 18 months ago, that single difference decides whether they get non-tobacco rates now, which can mean $40 or more per month saved over the life of a $20,000 policy.

- Cigar users sometimes catch a break. Occasional cigar smokers, not daily users, can qualify for non-tobacco rates with certain carriers.

- Vapers are increasingly treated as tobacco users. The industry has moved toward classifying vaping as tobacco use across the board.

- Smokeless tobacco is treated as tobacco use almost everywhere.

At $20,000, getting matched to the right carrier for your specific tobacco history is worth thousands of dollars over the life of the policy. This is exactly the kind of detail an independent agency is positioned to navigate, because it can shop your situation across carriers with different rules.

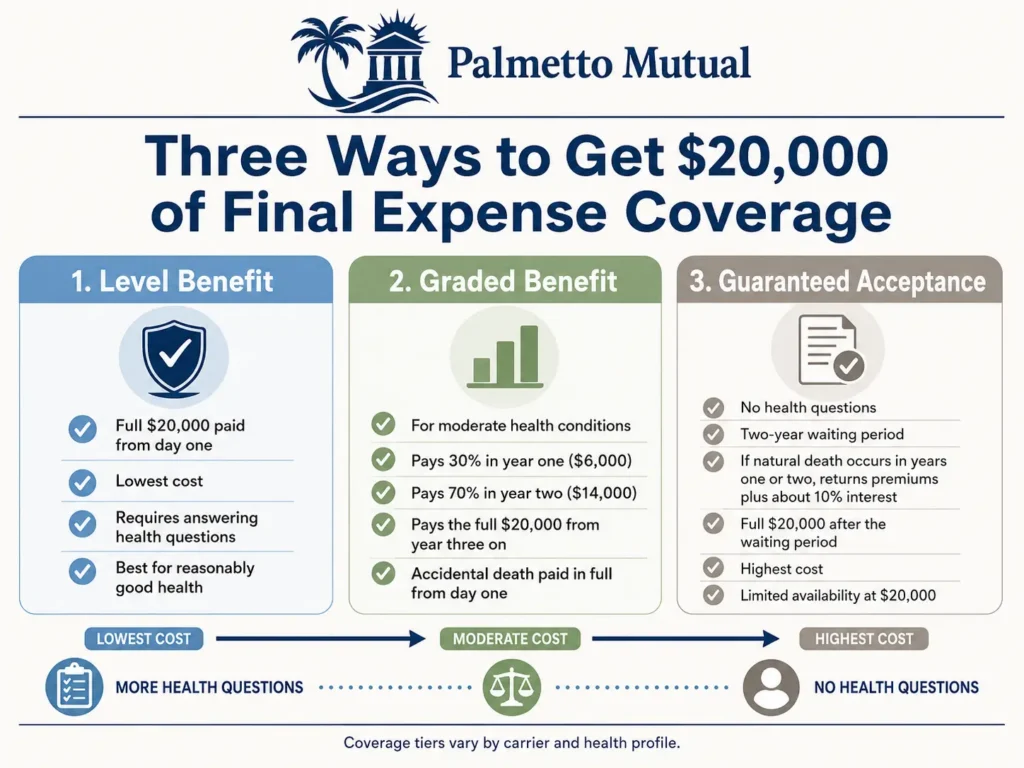

$20,000 Graded Benefit Policy Rates by Age (For Some Health Conditions)

Graded benefit is the middle tier of final expense insurance. It is built for applicants whose health is too complicated for level benefit but who can still answer some health questions. At $20,000 of coverage, this tier plays a bigger role than most buyers expect.

How Graded Benefit Works on a $20,000 Policy

A graded benefit policy pays only part of the death benefit if you die from natural causes in the first couple of years. The most common structure pays 30% in year one, 70% in year two, and the full amount from year three onward.

On a $20,000 policy, that schedule looks like this.

| Year of policy | Natural-cause payout |

|---|---|

| Year 1 | $6,000 (30%) |

| Year 2 | $14,000 (70%) |

| Year 3 and beyond | $20,000 (100%) |

Some carriers structure the early years differently, returning your premiums plus interest instead of a percentage of the benefit. Accidental death is usually paid in full from day one, even during the graded period.

At $20,000, those partial payouts are substantial. A $14,000 payout in year two is more coverage than many applicants could get any other way, since guaranteed acceptance products often cap well below that.

$20,000 Graded Benefit Monthly Rates by Age

The table below shows illustrative monthly premiums for a $20,000 graded benefit policy. Graded rates typically run 15% to 30% higher than level benefit rates for the same coverage.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $74 | $59 |

| 55 | $95 | $74 |

| 60 | $116 | $90 |

| 65 | $150 | $116 |

| 70 | $207 | $155 |

| 75 | $295 | $216 |

| 80 | $451 | $324 |

Sample monthly rates for graded benefit coverage at $20,000. Graded benefit pays a partial death benefit during the first two policy years before full coverage begins. Rates require answering health questions, and approval is not guaranteed. Current as of June 2026.

Why Graded Benefit Becomes Especially Important at $20,000

Here is the strategic point most generalist sites miss. Many guaranteed acceptance products cap their face amount at $10,000, $12,000, or $15,000.

That cap changes everything at this coverage amount. An applicant who does not qualify for level benefit but wants the full $20,000 often has only one path to it: graded benefit.

For someone with moderate health conditions, graded is not just the middle option. It is frequently the only way to reach $20,000 of immediate, partial-then-full coverage. That makes the level-versus-graded qualification process unusually important at this tier, and it is worth shopping carefully to land in the best tier you qualify for.

Who Lands in Graded Benefit at $20,000 Coverage

Certain health profiles commonly qualify for graded benefit but not level. These are buyers with manageable conditions that still make carriers cautious.

- Recent health diagnoses, typically one to two years out.

- Controlled chronic conditions that exceed level benefit thresholds.

- Certain medication profiles flagged in a prescription history check.

- severe heart conditions.

- COPD with oxygen use.

- Major complication diabetes.

One detail matters at this amount. Carriers often apply stricter level-benefit standards as the face amount rises, so some applicants who would qualify for level at $10,000 land in graded at $20,000. An independent agency can compare where your specific health profile qualifies across carriers, since the thresholds are not the same everywhere.

$20,000 Guaranteed Acceptance Rates by Age (No Medical Questions Required)

Guaranteed acceptance is the final tier, for applicants who cannot qualify for level or graded benefit. There are no health questions at all. The trade-off is a waiting period and the highest cost per dollar of coverage, and at $20,000 this tier comes with a real availability problem.

How Guaranteed Acceptance Works at $20,000 of Coverage

Guaranteed acceptance, also called guaranteed issue, asks no health questions, requires no medical exam, and runs no prescription or MIB check. Approval is guaranteed as long as you fall within the carrier’s age range, usually 50 to 80 or 50 to 85.

The catch is the waiting period. If you die from natural causes in the first two years, the policy returns your premiums plus interest, usually around 10%, rather than the full $20,000.

Accidental death is covered in full from day one. After the two-year period, natural-cause death is covered in full as well. This is the most expensive tier per dollar of coverage, which is the price of skipping health questions entirely.

$20,000 Guaranteed Acceptance Availability Is Genuinely Limited

This is the part competitor pages routinely miss, because they treat guaranteed acceptance as one uniform product. It is not.

Most guaranteed acceptance products cap their face amount at $10,000, $12,000, or $15,000, and many top out at $25,000 only for their best cases. Finding a single $20,000 guaranteed acceptance policy is far from guaranteed.

Applicants who genuinely need guaranteed issue at this level sometimes have to combine policies, for example a $15,000 plan from one carrier plus a $5,000 plan from another. Others accept a lower total amount. Knowing which carriers actually offer $20,000 guaranteed issue, and where the caps fall, is exactly the kind of market knowledge an independent agency brings.

$20,000 Guaranteed Acceptance Monthly Rates by Age

The table below shows illustrative rates where $20,000 guaranteed acceptance coverage is available. Because availability is limited, these reflect the carriers that do offer it. Guaranteed acceptance rates typically run 25% to 50% higher than level benefit, and more at older ages.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $111 | $69 |

| 55 | $113 | $88 |

| 60 | $127 | $102 |

| 65 | $170 | $125 |

| 70 | $198 | $151 |

| 75 | $279 | $216 |

| 80 | $453 | $352 |

Sample monthly rates for guaranteed issue coverage at $20,000. Guaranteed issue requires no health questions, and includes a two-year waiting period during which natural-cause death returns premiums paid plus interest rather than the full benefit. Current as of June 2026.

The Cumulative Premium Reality on $20,000 Guaranteed Acceptance

This is the math every buyer at this tier needs to see. Because guaranteed acceptance is priced highest, the premiums you pay over time can approach, or exceed, the death benefit itself.

Consider a $20,000 guaranteed acceptance policy bought at age 75 at roughly $230 a month. Over a 15-year life expectancy, that totals about $41,000 in premiums paid, well above the $20,000 the policy pays out.

| Purchase age | Sample monthly premium | Premiums over 15 years |

|---|---|---|

| 75 | ~$230 | ~$41,000 |

| 80 | ~$330 | ~$59,000 |

For some buyers, guaranteed acceptance is still the right call, because no other option exists for them. But that decision should be made with full knowledge of what you will pay over time versus what the policy pays out.

When $20,000 Guaranteed Acceptance Is the Right Choice — And When It Isn’t

This is the honest moment that separates a good agency from a lazy one.

Guaranteed acceptance at $20,000 is the right choice when all three of these are true:

- You genuinely do not qualify for level or graded benefit.

- You genuinely need $20,000 of immediate coverage.

- You understand the cumulative premium math and accept it.

It is the wrong choice in these situations:

- You would qualify for graded benefit at $20,000 but get sold guaranteed issue through lazy underwriting.

- You are in your late 70s or 80s, where the cumulative premium math means a smaller policy at a more affordable premium would serve you better.

One direct warning. If you are being pushed toward $20,000 guaranteed acceptance and no one has asked you a single health question, get a second opinion. Graded benefit at $20,000 is often achievable for buyers who are told otherwise, and the difference in both price and day-one coverage is significant. An independent broker who shops multiple carriers can confirm which tier you actually qualify for.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.