Home > Final Expense Insurance Cost > 15,000 Final Expense Insurance

$15,000 Final Expense Insurance: Cost & Options

Final expense insurance is a small whole life policy built to cover the costs that come at the end of life, and $15,000 is the tier where the coverage starts to feel complete rather than just adequate. For most applicants, a $15,000 burial insurance policy runs somewhere in the range of about $45 to $120 a month, depending mostly on your age, gender, tobacco use, and which carrier you choose. At this amount, the policy can fully pay for a traditional funeral in most parts of the country and still leave a few thousand dollars of buffer for final medical bills, lingering debts, or help for the family. That buffer is what makes $15,000 the level where many buyers stop trading one need against another and simply cover everything they had in mind.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a $15,000 level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

What Can $15,000 Really Pay For at a Funeral — And Will It Be Enough

Once you reach the $15,000 tier, the question changes. With smaller policies, buyers ask what fraction of the bill gets covered. With burial insurance at this level, the better question is whether it covers everything you actually want it to.

The Full Cost Picture for a Traditional Funeral in 2026

A traditional funeral with a viewing and burial is the most common and expensive option. The National Funeral Directors Association puts the national median for a funeral with viewing and burial at roughly $8,300, and closer to $9,400 once a vault is added — and many real-world bills land higher once cemetery and headstone costs are included.

Most full traditional funerals, including the cemetery plot and marker, fall in the $9,000 to $12,000 range nationwide. Cost of living is the biggest reason two families pay very different prices for the same service.

Here is how the major pieces tend to break down, and which ones swing the most by region:

| Cost component | Typical 2026 range | How much it varies by region |

|---|---|---|

| Funeral home services (basic fee) | $2,000 – $3,500 | Moderate |

| Embalming and body prep | $500 – $1,000 | Low |

| Viewing and ceremony | $1,000 – $2,000 | Moderate |

| Casket | $2,000 – $5,000+ | Low (price set by selection, not region) |

| Cemetery plot | $1,000 – $5,000+ | High |

| Vault or grave liner | $1,000 – $2,000 | Moderate |

| Headstone or marker | $1,000 – $3,000 | Moderate |

| Transportation and misc. | $500 – $1,000 | Low |

Region is the swing factor. The cemetery plot is where the gap is widest — a plot in a major Northeast or West Coast metro can cost several times what the same plot costs in a rural Southern or Midwestern county.

As a rough map: the Northeast and West Coast often run $13,000 to $16,000 for a full traditional burial, while much of the South and Midwest lands closer to $8,000 to $10,000. Your zip code can move the total by thousands.

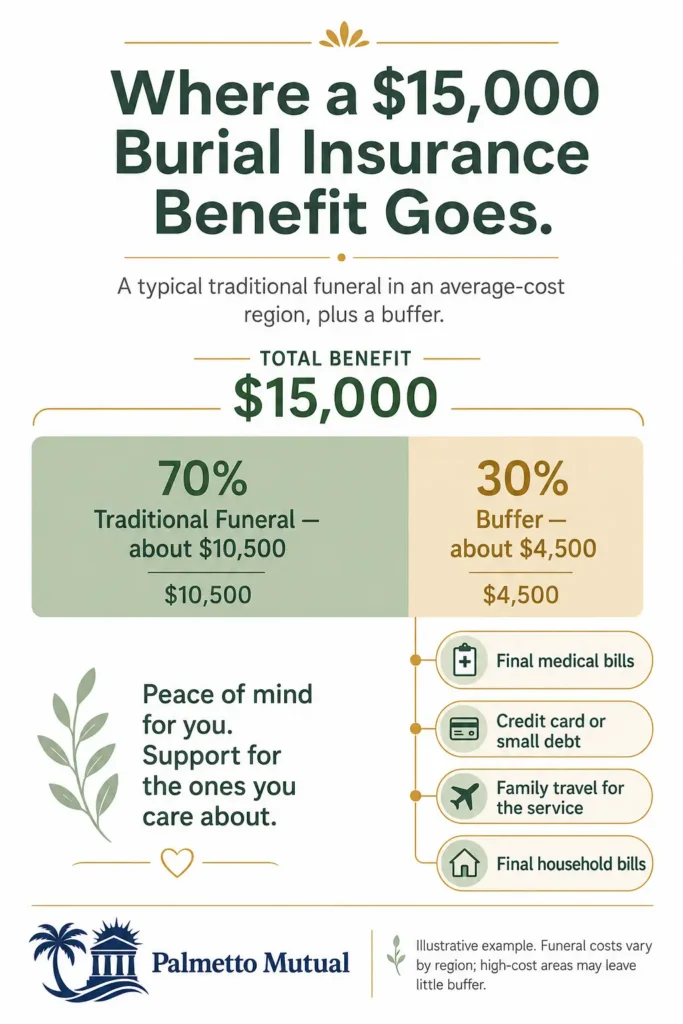

How $15,000 Covers a Traditional Funeral With Buffer

In an average-cost region, $15,000 is the level where the math finally works in your family’s favor. A full traditional funeral runs around $9,000 to $12,000, which leaves roughly $3,000 to $6,000 left over.

That leftover money is the whole point of stepping up to this tier. Because the death benefit is paid in cash, your family decides where it goes.

In practice, that buffer tends to cover things like:

- Outstanding medical bills from end-of-life care, such as hospital copays or hospice costs

- A remaining credit card balance or small loan

- Travel and lodging for family coming in for the service

- Small estate cleanup costs, like clearing a final utility or phone bill

For a family in an average-cost area, this is the tier where one policy genuinely covers the funeral and the loose ends, rather than forcing a choice between them.

Where $15,000 Still Falls Short for Traditional Burial

The honest caveat is that $15,000 is not a comfortable cushion everywhere. In high-cost-of-living regions, it may cover the funeral itself and leave little or nothing behind.

If you live in an expensive metro and want a full traditional burial, the funeral alone can cost $14,000 to $16,000. At that point, your $15,000 policy is doing its whole job just on the service, with no buffer for debts or medical bills.

Specific wishes can push past $15,000 on their own. A few examples that commonly exceed this tier:

- Mausoleum entombment instead of an in-ground plot

- A premium or custom hardwood or metal casket

- Multi-day visitation or a large memorial event

If you are in a high-cost area, or you have any of these specific plans, $20,000 or more is the more honest target. It is better to size the policy to what you actually want than to discover the gap later.

$15,000 for Cremation — Substantial Coverage Plus Significant Buffer

For anyone leaning toward cremation, $15,000 is more than generous. The NFDA median for a funeral with cremation and a viewing is roughly $6,300, and a simple cremation with a small memorial is often well under that.

Even a cremation with full memorial services rarely costs more than $7,000. That leaves $8,000 or more for other final expenses — or as a small, simple inheritance for the family.

If cremation is your plan, it is worth pausing to ask an honest question. You may not need this much coverage at all, and a $10,000 funeral insurance policy could cover everything with room to spare at a lower premium.

Common Uses for a $15,000 Death Benefit Beyond the Funeral

The death benefit is not earmarked for the funeral. It is paid directly to your beneficiary as cash, and they can use it for whatever the moment calls for.

At this coverage level, families most often use the extra toward:

- Clearing final medical bills, which commonly run $5,000 to $15,000 after a serious end-of-life illness

- Paying off credit card debt that would otherwise fall to the family

- Helping a surviving spouse stay current on the mortgage during the transition months

- Covering family travel, lodging, and time off work to attend the service

This flexibility is what separates final expense insurance from a prepaid funeral plan. A prepaid plan is locked to one funeral home and one set of services, while this policy hands your family money and lets them decide.

$15,000 Whole Life Policy Rates by Age (Non-Tobacco Applicants)

This is the most common profile for burial insurance buyers: someone who can answer “no” to the basic health questions and qualifies for a level benefit policy. The rates below show what $15,000 of whole life coverage typically costs month to month.

How $15,000 Whole Life Pricing Works

Carriers set your premium based on four main factors: your age at application, your gender, your tobacco status, and your health tier. Once the policy is issued, the premium is locked in for life and never increases.

Final expense is priced per $1,000 of coverage. The carrier figures your cost per thousand, then multiplies by how many thousands you want — so a $15,000 policy is simply that per-thousand rate times fifteen.

The $15,000 amount sits comfortably within this pricing. It is large enough that simplified underwriting can handle approval cleanly, and small enough to stay within the range where most carriers compete hardest. Many carriers show their most competitive pricing in the $10,000 to $20,000 band.

$15,000 Whole Life Monthly Rates by Age

The table below shows representative monthly premiums for a $15,000 level benefit whole life policy at non-tobacco rates. Figures at ages 50, 60, and 70 reflect TransAmerica’s published 2026 simplified issue schedule; the remaining ages are built from the same per-$1,000 pricing model at current 2026 market rates.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $44 | $35 |

| 55 | $52 | $40 |

| 60 | $64 | $48 |

| 65 | $83 | $60 |

| 70 | $110 | $78 |

| 75 | $148 | $107 |

| 80 | $208 | $146 |

Sample monthly rates for level benefit, non-tobacco applicants at $15,000 of coverage. Applying does not guarantee approval.

How $15,000 Rates Compare Across Carriers

Here is where shopping carriers stops being abstract. Two applicants with identical age, gender, and health can be quoted $15,000 rates that differ by 25 to 45 percent depending on which carrier they apply to.

At this coverage amount, those percentages turn into real dollars. The gap between the most and least competitive carrier for the same profile often runs $200 to $500 per year — and since the rate is locked for life, that difference repeats every year you hold the policy.

That is the entire case for comparing the market rather than taking the first quote. A 40 percent spread on a single carrier’s word can quietly cost a family thousands over the life of the policy. Because Palmetto Mutual is an independent broker rather than a single-carrier agent, the same profile can be run across multiple carriers to find the one that prices it lowest.

Why Locking In $15,000 in Your 60s Often Beats Waiting for Higher Coverage Later

There is a common instinct to wait, save up, and buy more coverage later. With this product, the math usually rewards the opposite move.

A 60-year-old who locks in $15,000 today pays a fixed premium for the rest of their life. Waiting until 70 to buy that same $15,000 means a much higher monthly rate.

Waiting also carries an underwriting risk unrelated to price. A health change in your 60s could push you out of level benefit and into a graded or guaranteed acceptance plan, which costs more and may add a waiting period. For many buyers, $15,000 secured at 60 to 65 is a better lifetime value than reaching for $20,000 or $25,000 at 70-plus and paying steep rates on a possibly downgraded health tier.

$15,000 Whole Life Policy Rates by Age (Tobacco Users)

This section mirrors the one above, but for applicants who use tobacco. Tobacco status is one of the largest single factors in a funeral insurance premium, so these rates run meaningfully higher than the non-tobacco table.

$15,000 Whole Life Tobacco Rates by Age

The table below shows representative monthly premiums for a $15,000 level benefit policy at tobacco rates, built by applying the current market surcharge to the non-tobacco baseline in the prior section. It uses the same age rows and gender columns for direct comparison.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $60 | $46 |

| 55 | $74 | $57 |

| 60 | $90 | $67 |

| 65 | $113 | $85 |

| 70 | $146 | $107 |

| 75 | $197 | $140 |

| 80 | $271 | $201 |

Sample monthly rates for level benefit, tobacco-use applicants at $15,000 of coverage. Applying does not guarantee approval.

Re-Rating to Non-Tobacco Status After Quitting

Here is something most TV-advertised products and generalist sites never mention: many carriers will re-rate a policy to non-tobacco pricing once you have been tobacco-free long enough, typically 12 to 24 months.

On a $15,000 policy, that re-rating is real money. Depending on your age when you quit and how long you live, the savings can add up to roughly $3,000 to $8,000 or more over the life of the policy.

The look-back length is exactly why the choice of carrier matters for someone who has recently quit. A person who stopped 14 months ago is treated very differently by a 12-month carrier than by a 24-month carrier.

Carrier Variation in Tobacco Underwriting

Tobacco underwriting is not uniform across the market, and the differences are bigger than most buyers realize. The look-back period is the clearest example — some carriers look back 12 months, others 24, and for someone who quit 18 months ago, that single difference decides tobacco versus non-tobacco pricing outright.

The definition of “tobacco user” also varies. Cigarettes always count, but treatment of other products differs:

- Occasional cigar users sometimes qualify for non-tobacco rates with specific carriers, while others rate all cigar use as tobacco.

- Vaping and nicotine products are increasingly treated as tobacco industry-wide, though a few carriers still differentiate.

- Smokeless and pipe tobacco are handled inconsistently from carrier to carrier.

This is the kind of granular, carrier-by-carrier knowledge that makes a multi-carrier consultation worth it. Because Palmetto Mutual works only with carriers that use a 12-month tobacco look-back, an applicant who quit more than a year ago is matched to a carrier that can price them at non-tobacco rates rather than being stuck on a longer clock.

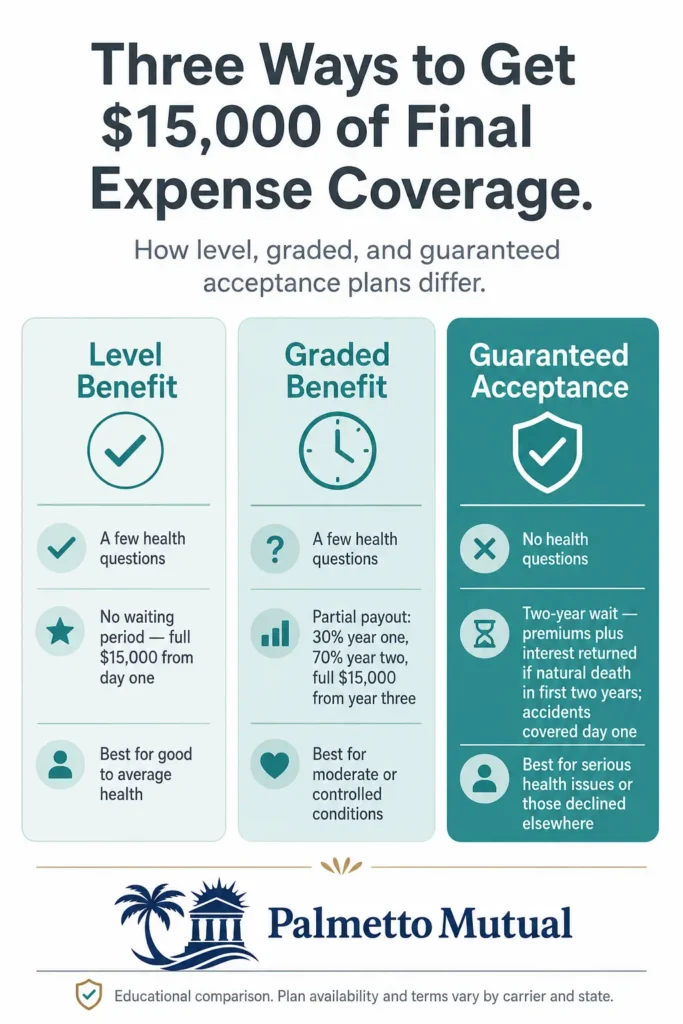

$15,000 Graded Benefit Policy Rates by Age (Health-Based Approval)

Graded benefit sits in the middle of the burial insurance lineup. It is built for applicants whose health keeps them out of level benefit pricing but who still want real coverage without dropping all the way to a no-questions plan.

How Graded Benefit Works on a $15,000 Policy

A graded benefit policy pays only a portion of the death benefit if you pass away from natural causes in the first couple of years, then pays in full after that. The most common structure pays 30 percent in year one, 70 percent in year two, and the full amount from year three onward.

On a $15,000 policy, that schedule looks like this:

| If natural-cause death occurs in | Amount paid on a $15,000 policy |

|---|---|

| Year 1 | $4,500 (30%) |

| Year 2 | $10,500 (70%) |

| Year 3 and beyond | $15,000 (100%) |

Accidental death is typically paid in full from day one, even during the graded period.

Some carriers use a slightly different version that returns your premiums plus interest in the first year or two, rather than a flat percentage. Either way, the key point is that graded benefit provides real first-day protection — meaningfully better than the zero-benefit start of a guaranteed acceptance plan — and, at $15,000, the partial payouts are still substantial.

$15,000 Graded Benefit Monthly Rates by Age

The table below shows representative monthly premiums for a $15,000 graded benefit policy at non-tobacco rates. Graded pricing typically runs about 15 to 30 percent higher than level benefit rates for the same applicant, so these figures are built by applying that premium step to the level benefit baseline from the earlier section.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $56 | $44 |

| 55 | $72 | $56 |

| 60 | $87 | $68 |

| 65 | $113 | $87 |

| 70 | $156 | $117 |

| 75 | $222 | $162 |

| 80 | $338 | $243 |

Sample monthly rates for graded benefit applicants at $15,000 of coverage. Applying does not guarantee approval.

Who Lands in the Graded Tier at $15,000

Graded benefit is for applicants who do not quite clear level benefit underwriting but are not high-risk enough to need guaranteed acceptance. Common profiles include:

- A health diagnosis one to two years in the past, still inside a carrier’s level benefit look-back

- A controlled chronic condition that exceeds the level benefit threshold

- Certain medications flagged in the prescription check

- Heavy heart conditions, or COPD with oxygen use

- Insulin-dependent with complicated diabetes

At $15,000 of coverage, graded benefit matters because it preserves access to a meaningful amount. Without it, an applicant in this group might have to cut down to $10,000 or fall back to a guaranteed acceptance plan with a full waiting period. Because conditions are weighed differently by carriers, an independent broker like Palmetto Mutual can sometimes find a carrier that places the same applicant in graded rather than guaranteed acceptance.

$15,000 Guaranteed Acceptance Policy Rates by Age (No Health Questions)

Guaranteed acceptance is the last tier, for applicants who cannot qualify for level or graded coverage. It trades the highest per-dollar cost and a waiting period for one thing no other plan offers: approval that cannot be turned down.

How Guaranteed Acceptance Works at $15,000 of Coverage

A guaranteed acceptance policy asks no health questions, requires no medical exam, and runs no prescription or MIB history check. As long as you fall within the carrier’s age range — commonly 45 to 85 — your approval is guaranteed.

The tradeoff is a two-year waiting period. If you pass away from natural causes in year one or two, the policy returns your premiums paid plus interest — typically 10 percent — rather than the full $15,000.

Accidental death is covered in full from day one. After the two-year mark, the full death benefit is paid for any cause. Per dollar of coverage, this is the most expensive plan tier, which is the price of skipping underwriting entirely.

$15,000 Guaranteed Acceptance Monthly Rates by Age

The table below shows representative monthly premiums for $15,000 of guaranteed acceptance coverage at non-tobacco rates. Guaranteed acceptance typically runs 40 to 80 percent higher than level benefit pricing, so these figures apply that step to the level benefit baseline. Carrier age limits vary, and some carriers issue guaranteed acceptance starting at age 45.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $90 | $62 |

| 55 | $99 | $75 |

| 60 | $110 | $87 |

| 65 | $147 | $107 |

| 70 | $172 | $130 |

| 75 | $243 | $188 |

| 80 | $336 | $309 |

Sample monthly rates for guaranteed acceptance applicants at $15,000 of coverage. Applying does not guarantee approval.

The Long-Term Math on $15,000 Guaranteed Acceptance

Because guaranteed acceptance is the most expensive tier, it is worth doing the math before committing. At older ages, the total premiums paid over many years can approach or even exceed the $15,000 death benefit if the insured lives long.

Take a 75-year-old paying roughly $231 a month for $15,000 of coverage. That is about $2,772 a year, so total premiums would pass the $15,000 death benefit in a little under six years and keep climbing after that.

This does not automatically make guaranteed acceptance a bad choice. For someone who genuinely cannot qualify for level or graded coverage, it may be the only option that exists, and the immediate certainty of coverage still has real value. The point is simply that the buyer should make that decision with the full cumulative cost in view, not just the monthly figure.

When $15,000 Guaranteed Acceptance Is the Right Choice — And When It Isn’t

Guaranteed acceptance is the right call for applicants who truly do not qualify for level or graded coverage — recent serious health events, a terminal diagnosis, or specific disqualifying conditions — and who genuinely need $15,000 of immediate-path coverage rather than a smaller amount.

It is the wrong call for someone who would actually qualify for level or graded benefit but gets steered into guaranteed acceptance through rushed underwriting or high-pressure sales tactics. That happens, and it costs the buyer money for life.

Here is a plain warning worth keeping: if you are being pushed toward a $15,000 guaranteed acceptance policy and no one has asked you a single health question, get a second opinion. There is a good chance you qualify for level or graded benefit at this coverage amount, and the difference in both price and waiting period is significant.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.