Home > Final Expense Insurance Cost > Final Expense Insurance in Your 50s

Final Expense Insurance in Your 50s: Costs, Coverage, and Whether It’s the Right Fit (2026)

If you are in your 50s and looking into final expense insurance, you are shopping at the best possible time. This is the decade when health-based approval is easiest, monthly rates are at their lowest, and you have the longest runway ahead of you to build value in the policy. But buying in your 50s comes with a question that older buyers do not really face: not just “which burial insurance plan fits me?” but “is this even the right kind of life insurance for me right now, or would term life or traditional whole life serve my goals better?” This page walks through both questions honestly — what final expense looks like at this age, and how to tell whether it is the right choice for you.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

What Final Expense Insurance Looks Like in Your 50s — And Why This Decade Matters

If you are in your 50s and looking into burial insurance, you are doing something a little different from older buyers. You are not usually shopping in a rush. You have time, good health on your side, and real choices about what kind of life insurance fits you best. That changes the whole conversation.

Why the 50s Is the Planning-Ahead Decade

Most people who shop for final expense insurance in their 50s are not reacting to a health scare. They are planning. Many are nearing retirement, helping a parent through end-of-life costs, or simply getting their financial house in order.

This decade comes with real advantages. You have the healthiest application profile of any age group, the lowest rates you will ever see, and the most years ahead to let a whole life policy build cash value.

Because of those advantages, the 50s deserves a closer look at the kind of product you buy — not just which final expense plan. Older buyers often have fewer options, so the choice is simpler. In your 50s, you can still qualify for products that may serve you better, which is why this page spends extra time on that question.

Why Premiums Are at Their Lowest in Your 50s

Final expense premiums sit at the bottom of the curve in your 50s. The rate you lock in now is the rate you keep for life, since these are level-premium whole life policies. A 50-year-old man pays about $30.55 per month for $10,000 of coverage through one common carrier at non-tobacco rates, while a 50-year-old woman pays about $24.24 for the same policy.

Waiting costs you. That same $10,000 policy for a man jumps to about $69.78 by age 70 — roughly a 128% increase over 20 years of delay. A $15,000 policy that runs around $40 to $55 a month at 52 commonly costs $60 to $80 at 62, and $100 to $130 at 72.

This is why the 50s is the one decade where larger coverage stays comfortable. Buying $20,000 to $25,000 is realistic on most retirement budgets at this age, which makes it the best time to lock in a bigger face amount without straining your future fixed income.

Who Should Actually Buy Final Expense in Their 50s

Plenty of 50s buyers are a great fit for funeral life insurance. But not everyone should default to it without looking at other options first. The product is built for simplicity and easy approval, and those are real benefits — if you actually need them.

You are likely a good fit if you:

- Have health conditions that would make traditional, fully underwritten life insurance hard or costly to get

- Want fast approval, often within 24 to 72 hours, with no medical exam

- Are nearing retirement and want to lock in a fixed monthly cost that never rises

- Have already looked at term life and traditional whole life and chose final expense on purpose

You may want to pause if you are a healthy 50-something who has not yet shopped traditional life insurance. Simplified issue is a good fit for people in relatively good health who want an affordable option without a medical exam, but premiums may still be higher than standard term or whole life insurance. If you are healthy, you might be paying for easy approval you do not actually need.

When Final Expense Is the Wrong Product in Your 50s

For many healthy 50s buyers, final expense is honestly not the best category. It is worth saying plainly, because no one benefits from buying the wrong product.

Term life gives you far more coverage for far less money during your working years. Term life insurance provides more coverage for a lower price if you are still relatively healthy. If you still carry a mortgage, support a spouse, or want income protection for a defined stretch of time, term often fits better. Term life works best for people in their 50s or 60s who need to protect a spouse’s income, pay off remaining debts, or cover post-retirement expenses for a set period.

Traditional whole life can also serve you better if you qualify. It offers permanent coverage and cash value, often at a lower cost per dollar than final expense, because final expense charges extra for its lenient, no-exam underwriting. Whole life rates are consistently higher than term, but they buy lifelong protection plus guaranteed cash value growth.

The simple rule: the premium you pay for simplified-issue speed and easy approval is only worth it if you need speed or easy approval. If you are healthy and have time, look at the alternatives first.

Average Final Expense Insurance Costs in Your 50s

Now to the numbers. This section fixes your decade as the constant and shows how rates move by age within the 50s and by how much coverage you buy. Final expense insurance pricing in this decade is the most affordable you will find, so it helps to see exactly where you land.

Final Expense Rates in Your 50s by Age and Coverage Amount

The table below shows estimated monthly premiums for a healthy, non-tobacco applicant at four coverage amounts across the decade. These are blended national estimates drawn from 2026 carrier data; your real rate depends on the carrier, your state, your sex, and your health profile.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 50 | $31 | $45 | $59 |

| 51 | $32 | $46 | $60 |

| 52 | $33 | $47 | $61 |

| 53 | $33 | $48 | $63 |

| 54 | $35 | $50 | $66 |

| 55 | $36 | $53 | $69 |

| 56 | $38 | $55 | $72 |

| 57 | $39 | $57 | $75 |

| 58 | $41 | $59 | $78 |

| 59 | $42 | $62 | $81 |

Sample monthly rates for male applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 50 | $25 | $35 | $46 |

| 51 | $26 | $36 | $47 |

| 52 | $26 | $38 | $49 |

| 53 | $27 | $39 | $50 |

| 54 | $28 | $40 | $51 |

| 55 | $28 | $40 | $53 |

| 56 | $29 | $42 | $54 |

| 57 | $30 | $44 | $57 |

| 58 | $31 | $45 | $59 |

| 59 | $32 | $46 | $61 |

Sample monthly rates for female applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

How Premiums Change Across Your 50s

The premium curve through the 50s is the gentlest of any decade. The yearly steps are small, so the gap between buying early and late in the decade is modest. A $15,000 policy bought at 50 typically costs only about 12% to 18% less than the same policy bought at 58.

That gentleness is the point. The difference between locking in at 52 versus 58 is real money over time, but it is not dramatic, which gives 50s buyers more breathing room on timing than 60s or 70s buyers have.

The contrast with later life is sharp. The steepest jump in the rate data comes between ages 75 and 80, where average monthly rates climb about 44% for women and 45% for men. Nothing in the 50s moves that fast. So the cost of waiting through this decade is genuine, but far less urgent than the cost of waiting through the decades that follow.

How Tobacco Use Changes Costs in Your 50s

Tobacco use raises your rate, and the surcharge is built into the premium from the start. Smokers typically pay 30% to 60% more than nonsmokers for final expense coverage. At common 50s coverage amounts, that often works out to roughly $15 to $45 or more in extra monthly cost.

Here is what makes the 50s special: you have the longest re-rating window of any decade. Carriers generally require you to be tobacco-free for a set period before they will reclassify you. If you quit smoking after buying a policy, you may be able to request a rate review after a tobacco-free period — some insurers require 12 months, others 24, and some longer. Because Palmetto Mutual works exclusively with carriers that use a 12-month tobacco look-back, that window is at the shorter end.

Quitting now and re-rating to non-tobacco pricing in a year or two means decades of savings on a policy you will hold a long time. The financial reward for quitting before you lock in coverage is higher at this age than at any other.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 50 | $41 | $60 | $79 |

| 51 | $43 | $63 | $82 |

| 52 | $45 | $65 | $86 |

| 53 | $47 | $68 | $90 |

| 54 | $49 | $71 | $94 |

| 55 | $51 | $74 | $98 |

| 56 | $52 | $77 | $102 |

| 57 | $54 | $80 | $106 |

| 58 | $57 | $84 | $111 |

| 59 | $59 | $87 | $115 |

Sample monthly rates for male applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 50 | $32 | $46 | $60 |

| 51 | $33 | $48 | $62 |

| 52 | $34 | $50 | $65 |

| 53 | $36 | $52 | $69 |

| 54 | $37 | $54 | $71 |

| 55 | $39 | $57 | $75 |

| 56 | $40 | $59 | $77 |

| 57 | $42 | $61 | $81 |

| 58 | $44 | $64 | $84 |

| 59 | $45 | $66 | $87 |

Sample monthly rates for female applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

How Health Conditions Affect Costs in Your 50s

Most everyday 50s conditions barely move your rate or your plan tier. Controlled high blood pressure, type 2 diabetes managed with oral medication, cholesterol treated with statins, anxiety or depression on stable medication, and mild arthritis typically have little to no effect on qualifying for level benefit coverage at this age.

Even heavier conditions often still allow level qualification in your 50s because carriers apply easier standards to younger applicants. A recent cardiac event, insulin-dependent diabetes, or COPD may nudge your rate up but frequently still permits a level benefit plan at 50s ages. Conditions like well-controlled diabetes or past heart issues sometimes push an applicant toward a graded benefit policy, which costs more and carries a waiting period. Whether that happens depends heavily on the carrier.

That carrier-by-carrier difference is the key takeaway. Different companies have genuinely different appetites for risk — a carrier that is cautious about diabetes might be aggressive on heart conditions, and the reverse. Matching your specific condition to the right carrier is exactly where shopping multiple companies pays off.

How Final Expense Underwriting Works in Your 50s

Underwriting is simply how a carrier decides whether to approve you and at what price. For final expense insurance, that process is far lighter than for traditional life insurance — and it is lightest of all in your 50s. Here is what carriers actually look at and why qualifying is easier at this age than any other.

What Carriers Actually Evaluate for 50s Applicants

There is no medical exam for final expense. Instead, carriers rely on a short health questionnaire plus a few automated database checks. Simplified issue final expense requires a brief health questionnaire but no medical exam, and the process is faster than traditional life insurance.

Behind the scenes, the carrier usually pulls two records. One is your MIB file, a shared industry database. Underwriters see coded health conditions and risk factors from your prior applications with other carriers, but not the decisions those carriers made. The other is a prescription history check. The MIB request is typically part of an automated batch that also includes prescription database checks.

Most 50s applications move quickly through this. Decisions often come within 24 to 72 hours, and some carriers approve in minutes. Some carriers use instant-decision underwriting that can approve applicants in under 10 minutes. Because the actuarial risk at this age is lower, 50s applications face the lightest scrutiny of any age group.

Why Most 50s Applicants Qualify for Level Benefit

Level benefit is the plan you want: full coverage from day one, lowest price, no waiting period. Carriers hand it out most freely to 50s applicants because their life expectancy is long enough to make the math comfortable. Even with chronic conditions like diabetes or high blood pressure, you can usually still qualify for level coverage, with the full death benefit available from day one.

The contrast with older applicants is real. Conditions that might push a 65- or 70-year-old toward a graded benefit plan — a recent cardiac event, insulin-dependent diabetes, advancing COPD — often still allow level qualification in your 50s. Graded benefit policies, which cost more and carry a one-to-three-year waiting period, are aimed at people with managed conditions who do not qualify for level benefit.

The honest framing: buy burial insurance in your 50s and you typically lock in level benefit even with conditions that would force a higher-priced graded plan if you waited until your 60s or 70s.

Why Locking In Underwriting Now Matters for Future-You

Here is the part that gets overlooked: your plan tier is permanent. The level, graded, or guaranteed-issue classification you qualify for at the time you apply is the one you keep for life, no matter how your health changes later.

That makes a 50s purchase about more than just a low rate. A 52-year-old who locks in level benefit today still has level benefit at 75 — even if conditions develop in their 60s that would push a brand-new applicant into a graded plan. The rate is frozen too, since these are level-premium whole life policies that never increase.

So the strongest argument for buying in your 50s is not only the price. It is locking in the best possible plan tier while the underwriting door is widest open.

When to Apply With a Multi-Carrier Agent vs. Direct

Going straight to a single carrier can work fine if you are a very healthy 50-something with no conditions and no complications. The application is simple, and you will likely qualify cleanly anywhere.

A multi-carrier agent earns their keep when there is any complexity — a health condition, tobacco use, a past denial, or a desire to find the carrier that prices your exact profile best. Each carrier has its own underwriting guidelines, which means the same person can be declined by one company and approved at preferred rates by another. An agent who can review your MIB history and match you to a carrier whose rules fit your profile changes the outcome.

The 50s are the decade where going direct is most viable, but shopping multiple carriers still tends to produce better rates for most people, meaningfully. Applying to several companies at once on your own can actually work against you, since multiple applications in a short window can hurt your underwriting outcome. A multi-carrier agent shops on your behalf without that risk.

How Much Coverage Most People in Their 50s Actually Buy

Choosing a coverage amount is really a question about what you want the policy to pay for. Final expense insurance is built to cover end-of-life costs, so the right number depends on whether you are planning for just a funeral or for a funeral plus debts and a cushion for family. Here is what 50s buyers tend to choose and how to think it through.

The Most Common Coverage Amounts for 50s Buyers

Buyers in their 50s usually fall into one of two camps. The first buys smaller policies, around $10,000 to $15,000, aimed squarely at funeral costs. They are locking in low rates now while their need is clearly defined.

The second buys larger policies, around $20,000 to $25,000, for broader end-of-life planning — funeral costs plus debt payoff and a financial buffer for loved ones. Both approaches are valid; the right one depends on your goals.

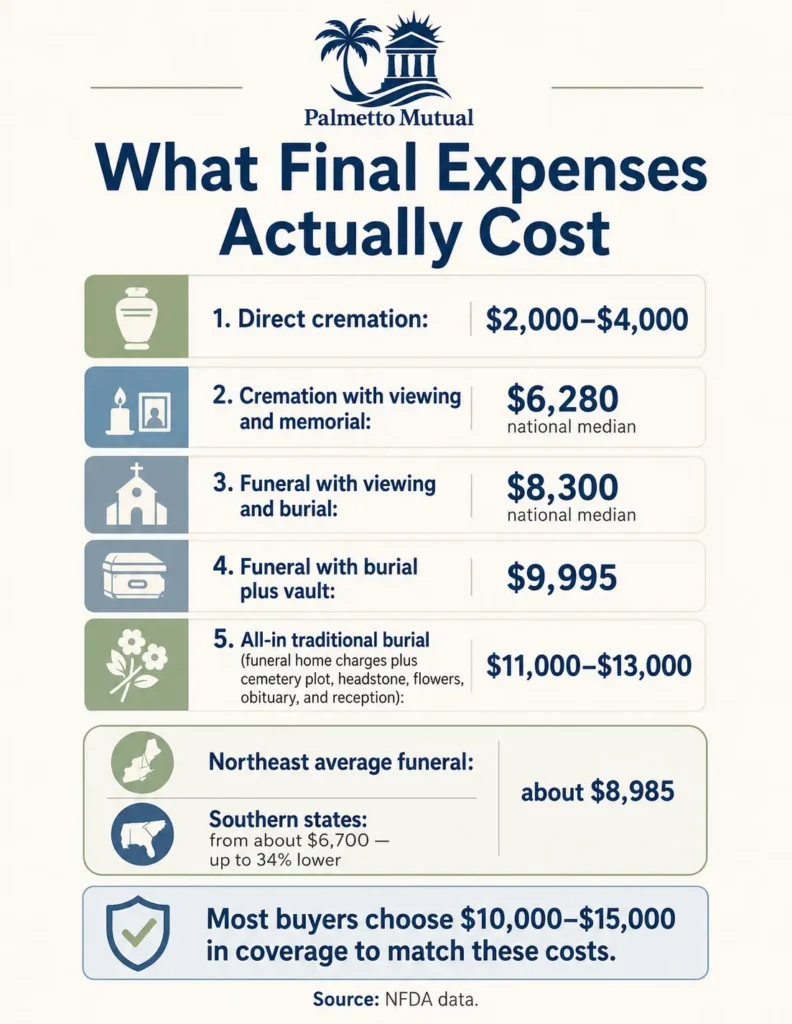

The smaller range maps closely to today’s typical funeral. The national median cost of a funeral with viewing and burial is about $8,300, rising to roughly $9,995 once a burial vault is added. That is why most seniors pick $10,000 to $15,000, since it lines up with the current cost of a funeral and final expenses.

Why 50s Buyers Often Buy More Coverage Than Older Buyers

The reason 50s buyers can reach for larger amounts is simple: premiums are at their lowest, so more coverage stays affordable. A 52-year-old can often lock in $25,000 for roughly what $15,000 costs a 65-year-old.

That pricing reality changes the math. Because the rate never rises once you lock it in, the cost advantage of buying young lasts the entire life of the policy. The same $10,000 policy that costs a man about $30.55 a month at 50 climbs to about $69.78 at 70 — roughly a 128% increase over 20 years of delay.

So if you anticipate eventually wanting $20,000 or more, you are usually better off locking in that amount now than buying $10,000 to $15,000 today and trying to add coverage later at higher rates.

When 50s Buyers Should Consider More Coverage

Larger coverage makes sense for some 50s buyers more than others. You may want to size up if you:

- Are approaching retirement with significant debt or obligations you want cleared

- Want one policy to eventually cover both spouses’ funerals plus a small inheritance

- Live in a higher-cost region where the all-in cost of a traditional burial — funeral home charges plus cemetery plot, headstone, flowers, obituary, and a reception — can reach the low-to-mid teens

- Have adult children whose finances make a little inheritance support meaningful

That regional point is worth a number. The funeral-home charge alone runs higher in pricier areas — Northeast funeral costs average around $8,985, up to about 34% more than Southern states that start near $6,700. Once you add cemetery and extras on top, a traditional burial commonly totals $11,000 to $13,000 all in, and the highest-cost metros push past that. Over a policy you might hold 30-plus years, inflation will likely lift those figures further.

When 50s Buyers Should Consider Less Coverage

Plenty of 50s buyers need less than they think. Smaller coverage may be the smarter choice if you:

- Plan a direct cremation rather than a traditional burial

- Already have savings or paid-off property that covers end-of-life costs

- Are single with no dependents who would need a financial buffer

- Would rather put the premium difference toward other goals like retirement savings or paying down a mortgage

Cremation is the clearest case. A direct cremation can cost as little as $2,000 to $4,000, which means a modest burial insurance policy may be all you need. Buying more coverage than your actual plan requires just raises your premium without adding value.

When 50s Buyers Should Skip Final Expense Entirely

Some 50s buyers should not buy final expense at all — at least not yet. This is the honest part, and it matters most at this age because you still have options older buyers do not.

If you have dependents who would benefit from coverage during your working years, look at term life first. Term life provides more coverage for a lower price if you are still relatively healthy. If you have steady income and good health, you may come out ahead with traditional whole life at a higher face amount, since funeral life insurance charges a premium for its easy, no-exam approval. Whole life rates are consistently higher than term because they include lifelong protection plus guaranteed cash value growth, but traditional whole life often costs less per dollar than final expense for someone who can qualify.

And if you are in your early 50s with strong family longevity, it can be reasonable to revisit the decision in your 60s, when the timing math gets more pressing. The point is to choose final expense on purpose, not by default.

Should You Lock In Final Expense in Your 50s — Or Wait?

This is the real decision for 50s buyers, and the honest answer is more nuanced than at older ages. Waiting costs you something with any final expense policy, but in your 50s that cost is gentler — which means “wait” is sometimes the right call. Here is how to think it through.

The Real Cost of Waiting From Your 50s Into Your 60s

Premiums do rise between your 50s and 60s, but the jump is more moderate than at later decades. A $15,000 level benefit policy that costs roughly $45 to $55 a month at 52 commonly runs $60 to $80 by 62.

Because the rate locks in for life, that monthly difference repeats every month for as long as you hold the policy. Over a 25-year policy life, the gap between buying at 52 and buying at 62 can add up to somewhere around $4,500 to $8,000 or more in extra lifetime premiums.

The takeaway: the math favors locking in earlier, but the urgency is lower in the 50s. Age is the biggest factor, and the longer you wait, the higher the rate — a 50-year-old pays significantly less than an 80-year-old for the same $10,000 policy. The steep part of that curve comes later, not now.

Why Health Changes During Your 50s Are Less Likely to Disqualify You

This is where the 50s genuinely differs from later decades. Most people who develop a new condition during their 50s still qualify for level benefit if they apply afterward, because the underwriting environment at this age is forgiving enough to absorb it.

That is the opposite of the 60s-and-70s argument, where a new diagnosis can permanently push you into a higher-priced graded plan. Graded benefit policies, which cost more and carry a waiting period, exist for people with managed conditions who no longer qualify for level coverage.

So waiting through your 50s carries less underwriting risk than waiting through later decades. If you want to defer the decision into your late 50s or early 60s, you can usually do so without losing access to favorable qualification — though that is never guaranteed, since a serious diagnosis can change the picture at any age.

When Locking In at 52 Genuinely Beats Locking In at 58

Even within the decade, buying earlier has real advantages. The premium difference is modest — often $10 to $20 a month less at 52 than at 58 for the same policy — but it is not the only factor.

The bigger edge is cash value. Final expense is whole life, so it slowly builds value over time, and a policy issued at 52 simply has more years to accumulate. Cash value grows tax-deferred but builds slowly, and most policyholders do not accumulate meaningful value in the first seven to ten years. Starting earlier gives that slow growth more runway.

So the buyer who locks in at 52 typically pays a bit less over the policy’s life and ends up with meaningfully more cash value than the buyer who waits until 58 for identical coverage.

When Waiting Until Late 50s or Early 60s Makes Sense

Here is the counterpoint, because waiting is often the right call in this decade. You may reasonably hold off if you:

- Are genuinely unsure whether final expense is the right product category for you

- Are still in your working years and would benefit more from term life during that stretch

- Want to put the premium toward retirement contributions, a mortgage payoff, or kids’ education first

- Are facing a major life transition — retirement, downsizing, relocating — and want your financial picture to settle

None of these is a reason to ignore the decision forever. But unlike a 70-year-old, a healthy 53-year-old usually does not pay a steep penalty for taking another year or two to get it right. Burial insurance will still be there, and likely still at favorable terms.

Whether Final Expense Is Even the Right Product in Your 50s

This is the most important check at this age. For many healthy 50s buyers, a traditional life insurance product serves their goals better than final expense.

Term life delivers far more coverage per dollar during working years. Term life provides more coverage for a lower price if you are still relatively healthy. Traditional whole life offers permanent coverage at a lower cost per dollar than final expense for someone who can qualify for full underwriting. Whole life policies cost far more per month than comparable term coverage and make the most sense for buyers with estate-planning goals, lifelong dependents, or a guaranteed inheritance strategy. And for healthy applicants wanting larger amounts, simplified-issue whole life from non-final-expense carriers often prices better than final expense above $25,000.

The honest recommendation: before committing to funeral life insurance in your 50s, look at term life, traditional whole life, and simplified-issue whole life. For many 50s buyers, the right answer is one of those alternatives.

Best Carrier Considerations for Buyers in Your 50s

Once you have decided final expense is right for you, the next question is which carrier. The good news is that picking a carrier in your 50s is lower-stakes than at older ages — but it still matters more than most people realize. Here is what to weigh.

Why Carrier Selection Matters Differently in Your 50s

Rates do vary between carriers in your 50s, but the spread is narrower than in the 60s and 70s. A 50s applicant typically sees something like 20% to 40% variation between carriers, versus a wider gap at older ages.

The reason is qualification. Because most 50s applicants qualify for level benefit almost everywhere, pricing compresses — carriers are competing for the same low-risk applicant. Even at age 70, a man’s monthly premium for $10,000 ranged from $70 at one carrier to $77 at another, a gap that adds up to hundreds of dollars over a decade.

Carrier choice still matters. On a 50s policy held for decades, the difference between the most and least competitive carrier can total several thousand dollars in lifetime premium. The financial stakes are just lower than they will be later.

What Makes a Carrier “Good” for 50s Buyers

The right carrier for a 50s buyer is not just the cheapest one this month. Because you may hold this policy 30 to 40 years, durability and features matter more than at older ages. Worth weighing:

- Competitive 50s pricing, since some carriers price aggressively for this decade to win younger customers

- Strong long-term financial stability, because you will rely on this carrier paying a claim decades from now

- Useful rider options like accelerated death benefit, accidental death, or return of premium

- A solid cash value structure, since you have the longest accumulation runway

Financial strength deserves special weight here. AM Best ratings reflect an insurer’s ability to meet long-term obligations, and they carry more weight for whole life buyers because the relationship may last decades. A common benchmark is an AM Best rating of A or higher. Many companies include an accelerated death benefit rider at no extra charge, which is a nice baseline to look for.

How Carrier Underwriting Niches Affect 50s Applicants

Carriers are not interchangeable — each has conditions and customer profiles it treats more favorably than others. Some specifically court 50s applicants and offer their best rates at these ages. Others run tobacco-friendly underwriting, which matters for 50s smokers planning to quit and re-rate. One carrier prices smokers the same as nonsmokers on certain products, which makes it a standout for tobacco users.

Rider niches matter too. Features like return of premium work better when a policy has decades to grow, which favors younger buyers. But the brochure label rarely tells the full story. Two carriers may both advertise the same rider yet behave very differently at claim time, since the rider wording and how it is administered are what control.

So the best carrier for a healthy 52-year-old who wants rich features is often different from the best carrier for a 58-year-old focused purely on the lowest premium.

Why Multi-Carrier Quotes Still Matter in Your 50s

Even though going direct is more viable in your 50s than at older ages, comparing carriers still tends to produce better results. Because underwriting guidelines vary so much, a condition that raises your rate at one company may be accepted at a standard rate by another, which is why comparing your profile across many carriers finds the lowest price.

A 50s buyer who shops several carriers commonly finds rates well below what they would get applying to the first major company they research. Over a 30-plus-year policy, that gap compounds into real money. And there is a risk to doing it yourself piecemeal. Applying to several companies at once on your own can work against you, since multiple applications in a short window can hurt your underwriting outcome.

The cleanest way to compare accurately is a single conversation that shops your specific profile across multiple carriers at once. A short phone consultation lets a licensed agent match your age, health, and goals to the carrier that views you most favorably — without the risk of stacking applications. That is the most reliable path to an accurate, competitive quote for your situation.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.