Home > Final Expense Insurance Cost > Final Expense Insurance in Your 70s

Final Expense Insurance in Your 70s: What It Costs and How to Choose the Right Plan (2026)

Final expense insurance works a little differently once you reach your 70s than it did in your 60s. This is the decade where monthly premiums climb more noticeably, where more applicants are steered toward graded benefit plans instead of immediate full coverage, and where the choice of carrier starts to make a real difference in what you pay. It is also the decade where the timing of your decision matters most: each additional year of age tends to raise your premium and can narrow the plans you qualify for, sometimes permanently. This page walks you through what burial insurance looks like for buyers in their 70s — the costs to expect, how much coverage most people choose, how underwriting works at this age, and how to think clearly about whether to lock in coverage now or wait.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

What Final Expense Insurance Looks Like in Your 70s — And Why This Decade Changes Everything

By the time you reach your 70s, final expense insurance is still very much within reach — but the decision carries more weight than it did even a few years earlier. This is the decade where the price you lock in starts to move quickly with each birthday, where more applicants are routed into graded benefit plans, and where the difference between one carrier and another can mean hundreds of dollars a year for the same coverage. Choosing the right company, at the right time, has the biggest financial impact here that it will at any age.

Why the 70s Is the Narrowing-Options Decade

The 70s earns its reputation as the decade where choices begin to tighten. Premiums step up clearly from the rates a buyer would have seen in their early or mid-60s, and that gap widens steadily across the decade.

Underwriting standards also tighten. Health conditions that would have allowed a 65-year-old to qualify for a level benefit plan — the kind that pays the full amount from day one — increasingly push a 75-year-old toward a graded benefit plan instead.

Carrier availability starts to narrow, too. Some companies stop issuing new policies at age 75 or 80, and at least one A-rated carrier reduces its maximum coverage once an applicant reaches 76.

For many people, the 70s is also simply the decade when burial insurance moves from “something to think about” to “something to handle” — often after helping a parent or spouse through end-of-life costs firsthand.

Who Should Buy Final Expense in Their 70s

Final expense insurance in the 70s fits several common situations:

- Buyers who have not yet locked in coverage and whose health is stable enough to qualify now.

- Buyers with declining health who want to secure a plan before their qualification slips further.

- People who outlived earlier financial plans and now need coverage they never put in place.

- Couples where one spouse begins looking at coverage after watching the other navigate health changes.

The honest framing is straightforward: a 70s buyer shopping for the first time benefits from moving with intention. Waiting carries a real dollar cost and a real risk of qualifying for a less favorable plan tier later.

When 70s Buyers Should Pause Before Buying

Just as important is knowing when not to rush. Some 70s buyers should slow down even with the timing pressure working against them.

A buyer in poor health with a limited life expectancy should look closely at the cumulative premium math. A 78-year-old with serious health concerns could end up paying more in total premiums than the policy would ever pay out.

A buyer who already has substantial savings set aside for end-of-life costs may not need an additional policy at all.

And anyone being pushed hard toward a guaranteed acceptance product by an aggressive sales pitch should pause and check whether a graded or level benefit plan is achievable first, since those usually offer better value. Buying without an honest look at the numbers is sometimes worse than not buying.

Average Final Expense Insurance Costs in Your 70s

This is the section where the numbers come into focus. Rather than holding coverage steady and changing the age, the tables below fix the decade and let you see how burial insurance pricing moves across the ages within your 70s and across different coverage amounts. All figures are illustrative market ranges for a healthy, non-tobacco applicant, not a quote.

Final Expense Rates in Your 70s by Age and Coverage Amount

The tables below shows approximate monthly premiums across ages and coverage amounts in the 70s. These are blended market ranges drawn from carrier and broker rate data. Men generally pay more than women at every age, so each cell shows a range that spans both.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 70 | $75 | $111 | $147 |

| 71 | $79 | $117 | $155 |

| 72 | $84 | $125 | $165 |

| 73 | $90 | $133 | $176 |

| 74 | $95 | $141 | $187 |

| 75 | $100 | $149 | $197 |

| 76 | $108 | $159 | $211 |

| 77 | $115 | $170 | $226 |

| 78 | $123 | $182 | $242 |

| 79 | $130 | $193 | $256 |

Sample monthly rates for male applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 70 | $54 | $79 | $104 |

| 71 | $57 | $83 | $110 |

| 72 | $59 | $87 | $114 |

| 73 | $64 | $94 | $124 |

| 74 | $68 | $101 | $133 |

| 75 | $73 | $108 | $142 |

| 76 | $79 | $116 | $154 |

| 77 | $84 | $124 | $164 |

| 78 | $89 | $132 | $174 |

| 79 | $94 | $139 | $184 |

Sample monthly rates for female applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

How Premiums Climb Across Your 70s

The premium curve through the 70s is the steepest of any decade before the 80s. Each year of age adds a meaningful amount to the monthly cost — commonly in the range of $8 to $15 per year on a $15,000 policy.

Stretched across the decade, the gap is large. A buyer who locks in a $15,000 policy in the early 70s can pay $50 to $80 less per month than a buyer who waits until the late 70s for the very same coverage.

Because the premium never increases once you buy, that monthly difference rides along for the life of the policy. Over a typical policy life, the gap between an early-70s purchase and a late-70s purchase can add up to somewhere in the range of $10,000 to $18,000 in additional lifetime premiums for identical coverage. The plain takeaway: in your 70s, every year of waiting is genuinely expensive.

How Tobacco Use Changes Costs in Your 70s

Tobacco use raises final expense premiums at every age, and the 70s are no exception. A tobacco rate in this decade commonly runs well above the non-tobacco rate — at typical 70s coverage amounts, that often means $40 to $100 or more in additional monthly premium.

There is a decade-specific wrinkle worth understanding. Some carriers will move you to non-tobacco rates after you have been tobacco-free for a set period, often 12 months, but a 70s buyer has less runway to benefit from that than a younger applicant. Quitting now and re-rating after a year or two can still produce savings — the window to recover those savings is just shorter.

For some 70s tobacco users, locking in a tobacco rate today can actually produce a better total cost outcome than waiting to quit and re-rate, because the savings from waiting may not outweigh the premium increases that come with the added age. The right answer depends on the individual. A deeper breakdown lives on the tobacco guide.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 70 | $99 | $147 | $194 |

| 71 | $104 | $155 | $206 |

| 72 | $110 | $164 | $218 |

| 73 | $117 | $174 | $231 |

| 74 | $124 | $185 | $245 |

| 75 | $133 | $198 | $263 |

| 76 | $142 | $211 | $280 |

| 77 | $151 | $225 | $299 |

| 78 | $162 | $242 | $321 |

| 79 | $172 | $256 | $340 |

Sample monthly rates for male applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 70 | $73 | $107 | $142 |

| 71 | $76 | $113 | $150 |

| 72 | $80 | $119 | $157 |

| 73 | $85 | $125 | $166 |

| 74 | $89 | $132 | $175 |

| 75 | $95 | $141 | $187 |

| 76 | $102 | $152 | $201 |

| 77 | $109 | $162 | $214 |

| 78 | $116 | $172 | $228 |

| 79 | $126 | $187 | $248 |

Sample monthly rates for female applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

How Much Coverage Most People in Their 70s Actually Buy

Choosing a coverage amount in your 70s is a balance between what would fully cover your final costs and what fits comfortably in a fixed monthly budget. Most burial insurance buyers in this decade settle into a fairly narrow band, and understanding where other 70s buyers land can help you size your own policy with realistic expectations.

The Most Common Coverage Amounts for 70s Buyers

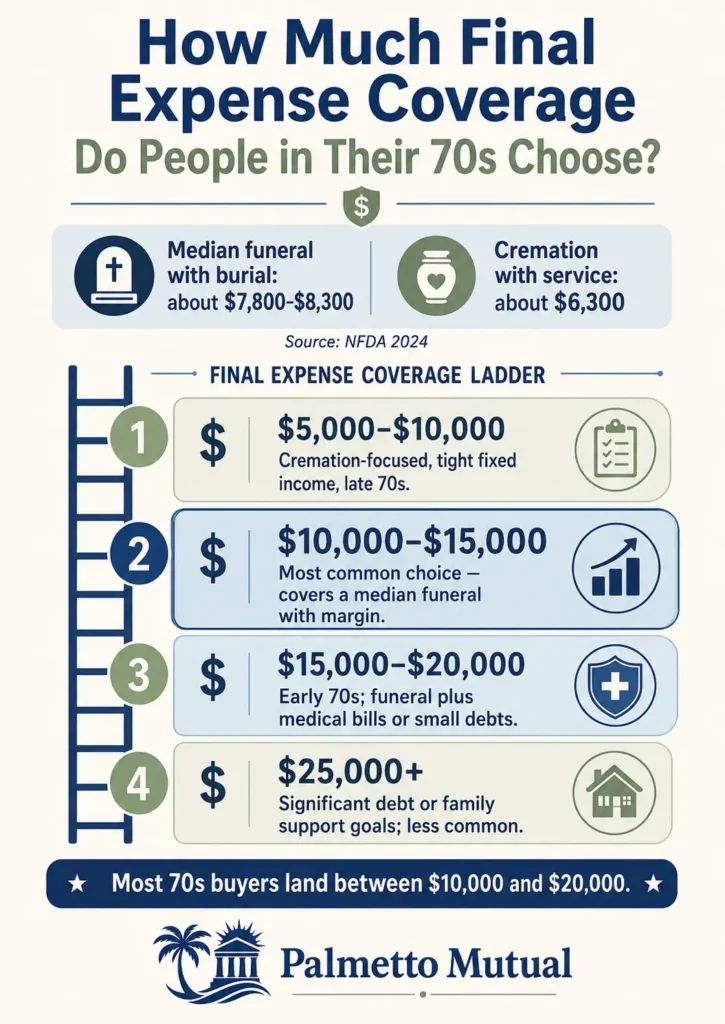

The typical 70s buyer purchases somewhere between $10,000 and $20,000 in coverage. That range lines up closely with the national median funeral cost, which the NFDA reports at roughly $7,800 to $8,300 for a service with burial, with cremation running lower at around $6,300.

Within that band, lower amounts tend to go with late-70s buyers and tighter budgets, while $15,000 to $20,000 is more common among early-70s buyers and those with more financial room.

Higher amounts of $25,000 or more are less common in the 70s than in younger decades. At this age, premiums on larger policies become genuinely expensive, so many buyers face a real choice between a bigger death benefit and a premium they can sustain for life.

Why 70s Buyers Often Buy Less Coverage Than They Originally Wanted

Many people come into the decision wanting $20,000 to $25,000 in coverage, then find that the premium at those amounts strains a fixed income. This is a common and understandable gap between the goal and the budget.

The realistic question often shifts from “how much coverage do I want?” to “how much coverage can I comfortably pay for, every month, for the rest of my life?” That second question is the one that keeps a policy in force.

The 70s is the decade where this gap shows up most clearly. It is also where an honest conversation about the tradeoffs does the most good, because the worst outcome is buying more than you can sustain and letting the policy lapse later.

When 70s Buyers Should Stretch for More Coverage

Sometimes reaching for a higher amount is the right call. A few situations where that holds true:

- You live in a higher cost-of-living area where funerals run closer to $13,000 to $16,000 once cemetery, monument, and service costs are added in.

- You carry meaningful outstanding debt or expect significant final medical bills.

- You and a spouse want a policy that covers a funeral and leaves something to support the surviving partner.

- You have adult children for whom a modest inheritance would make a real difference.

The honest framing is that stretching for more coverage in your 70s can be the right decision, but it should be a deliberate one based on a real need rather than aspirational planning.

When 70s Buyers Should Accept Less Coverage

Just as often, accepting a smaller amount is the wiser move. Consider a lower coverage amount if:

- You are planning a direct cremation rather than a traditional burial, which costs considerably less.

- You already have savings set aside specifically for final expenses.

- You are single with no dependents relying on a death benefit.

- A higher premium would create real strain on a tight fixed income.

A smaller policy you can comfortably keep for life beats a larger one you may have to drop. In final expense insurance, a policy that lapses helps no one, so matching the premium to your budget protects the whole purpose of the coverage.

Coverage Amount Recommendations by 70s Profile

Here is where common 70s profiles tend to land, as a starting point for your own decision:

- Early 70s, stable health, reasonable budget — usually $15,000 to $20,000.

- Late 70s, fixed income — usually $10,000 to $15,000.

- Significant debt or family obligations — may stretch to $20,000 to $25,000 despite the premium.

- Cremation-focused — usually $5,000 to $10,000.

These are general patterns, not prescriptions. Your right number depends on your funeral plans, your other resources, and what you can pay each month without strain.

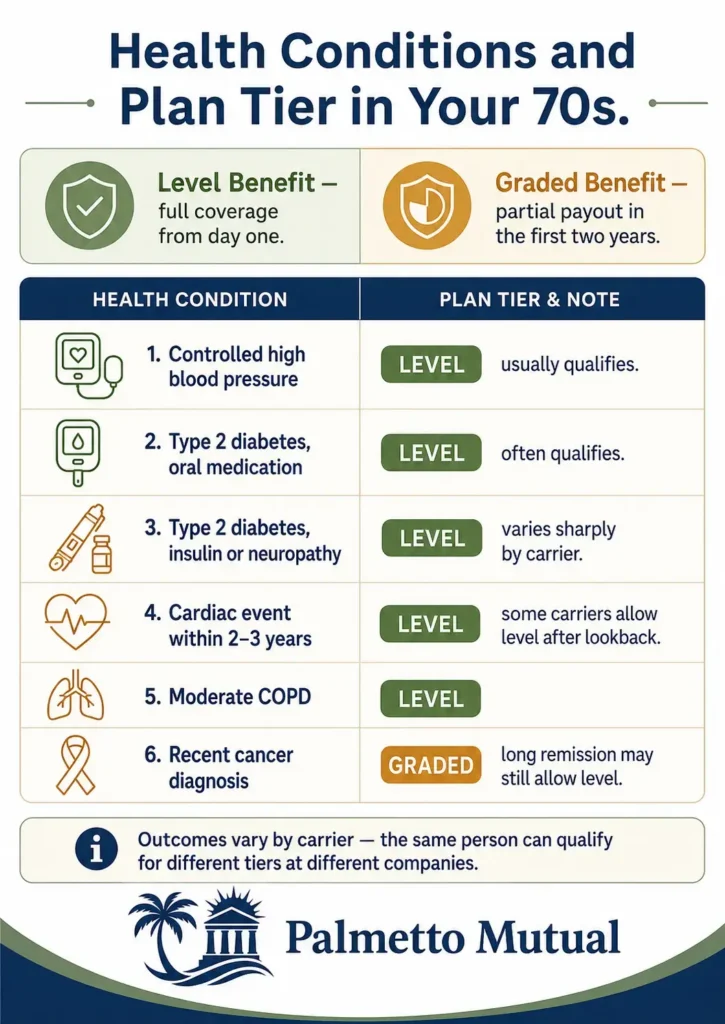

How Final Expense Underwriting Works in Your 70s

Underwriting is how an insurance company decides whether to approve you and which plan tier you qualify for. Knowing what carriers look at — and why their decisions matter more in this decade — helps you apply in the right place the first time and avoid an unnecessary downgrade in your burial insurance options.

What Carriers Actually Evaluate for 70s Applicants

Final expense insurance uses what is called simplified-issue underwriting. There is no medical exam and no blood draw — instead, you answer a short set of yes-or-no health questions, usually five to ten of them.

Carriers then verify your answers against outside data. The two main checks are the Medical Information Bureau (MIB), a shared database insurers use to spot inconsistencies, and your prescription drug history, which often reveals the conditions you are being treated for.

Some carriers also conduct a short telephone interview to confirm the application, often lasting around 8 to 12 minutes for a final expense policy. Decisions frequently come back quickly — sometimes within minutes, often within a few days — though carriers tend to apply more scrutiny at 70s ages than at younger ones.

How Health Changes During Your 70s Affect Qualification

Because the underwriting environment is already tight in this decade, a new health event has an outsized effect on what you can qualify for. The timing of your application relative to your health can change the outcome dramatically.

Consider two versions of the same person. A 72-year-old who applies right after a cardiac event is commonly steered to a graded plan. The same person who had already locked in a level plan at 70 keeps that full day-one coverage for life, no matter what happens to their health afterward.

That is the core reason 70s buyers face more qualification risk than buyers in any earlier decade. Health conditions at this age carry the most weight, and waiting often means accepting a downgrade that does not reverse.

Why Multi-Carrier Underwriting Matters Most in Your 70s

Applying directly to a single carrier in your 70s often produces a worse result than it needs to — a decline, or a graded offer, when a level plan was achievable somewhere else. The reason is simple: each carrier has its own underwriting niche, and those niches diverge most widely at this age.

A 74-year-old with type 2 diabetes and neuropathy might be declined at one company, offered graded benefit at a second, and offered level benefit at a third — for the exact same health profile. Knowing which carrier treats which condition most favorably is where an independent agent working across many carriers earns their value.

Should You Lock In Final Expense in Your 70s — Or Wait?

The decision to buy now or wait carries more financial weight in your 70s than in any earlier decade. The reason is straightforward: premiums rise with every birthday, and your health has more chances to change in ways that affect what you can qualify for. This section walks through the real math of waiting so you can make the call with clear eyes.

The Real Cost of Waiting From Your 70s Into Your 80s

The premium jump between a 70s purchase and an 80s purchase is large. Industry rate analysis points to the sharpest single jump landing between ages 75 and 80, where average premiums climb by roughly the same amount for men and women.

A $15,000 level benefit policy bought in the early 70s commonly costs far less per month than the same policy bought in the early 80s. Because the premium locks in at purchase and never rises, that monthly gap rides along for the life of the policy.

There is also the question of whether you can buy at all. Most carriers stop issuing new policies somewhere between ages 80 and 85. Waiting into your 80s does not just cost more — it narrows the menu and, for some buyers, closes it.

Over the full life of a policy, the difference between buying in the early 70s and waiting into the early 80s can add up to many thousands of dollars in additional lifetime premiums, and that assumes you still qualify at the later age. The math favors locking in earlier.

Why Health Changes During Your 70s Often Disqualify Buyers Permanently

Most 70s applicants who develop a new condition mid-decade get moved to a graded benefit plan, and some are declined for the plans they want. A new cancer diagnosis, a cardiac event, a stroke, or significant cognitive decline can each take a level benefit plan off the table.

Worsening control of an existing condition does the same. Diabetes that becomes harder to manage, advancing COPD, or a deteriorating heart condition can each trigger a downgrade, and those downgrades generally do not reverse.

The honest framing is that waiting through your 70s is a bet that your health holds steady for years to come. At this age, that is a bet that often does not pay off, which is why securing burial insurance while you qualify carries real value.

When Locking In at 72 Substantially Beats Locking In at 78

Buying at the front of the decade beats buying at the back of it on two fronts at once. The premium is meaningfully lower — commonly $40 to $60 or more per month less at 72 than at 78 for the same policy — and that gap is locked for life.

The underwriting environment is also friendlier at the younger ages. More carriers compete for your business, you likely have fewer accumulated health conditions, and you have a longer stretch of coverage ahead.

Put together, the buyer who locks in at 72 often pays many thousands of dollars less over the life of the policy than the buyer who waits to 78, and faces far lower risk of a qualification downgrade along the way.

When 70s Buyers Reasonably Wait

Few 70s buyers have a strong reason to wait, but some situations are legitimate. A short, purposeful delay can make sense when:

- You are in the middle of a major transition — downsizing, relocating, or finishing a financial plan — and want your picture stable before committing to a premium.

- You have a significant surgery or treatment program coming up, and waiting until after recovery may produce a clearer underwriting result.

- You are genuinely unsure how much coverage you need and a brief pause would help you decide.

Even in these cases, the delay should be measured in months, not years. Waiting in your 70s carries real cost and real qualification risk, so the reason to wait should be concrete.

When the Cumulative Premium Math Argues Against Buying

For some 70s buyers, the math points the other way. A buyer in poor health with a limited life expectancy can end up paying more in total premiums than the policy will ever pay out.

Picture a 78-year-old with serious health concerns buying a guaranteed acceptance policy at a high monthly premium. Over their remaining years, the premiums paid could exceed the death benefit, and a graded or guaranteed plan may also pay only a return of premiums if death comes in the first two years.

This deserves an honest look rather than a sales pitch. For some buyers, the answer is to buy anyway because the family needs the coverage in hand regardless of the math. For others, keeping the money makes more sense. Both choices are valid — what matters is seeing the numbers clearly enough to decide on purpose.

Carrier Considerations for Buyers in Your 70s

Which company you apply to matters more in your 70s than at any other age. Carriers price the same applicant differently and judge the same health history differently, so the right match can mean both a lower premium and a better plan tier. This section covers what to weigh, with deeper carrier-by-carrier detail on the best companies hub.

Why Carrier Selection Matters Most in Your 70s

Rate variation between carriers is at its widest in this decade. Even for routine profiles, quotes for the same coverage can differ by a wide margin — one analysis found a 72-year-old woman receiving quotes from roughly $78 to $105 a month for the same $10,000 policy depending on the insurer.

That spread comes from the fact that each carrier sets its own rates and underwriting appetite. The company that prices aggressively for a healthy 71-year-old is often not the company that treats a 76-year-old with diabetes most favorably.

Stacked over the life of a policy, the difference between the most and least competitive carrier can run into the thousands. When the gap between a level and a graded plan is added on top, the stakes of choosing well climb higher still.

What Makes a Carrier “Good” for 70s Buyers

A strong carrier for a 70s buyer tends to share a few traits. Use these as an evaluation framework rather than a ranking:

- Competitive rates for this decade. Some carriers price the 70s aggressively despite the higher risk, while others become uncompetitive at these ages.

- Lenient underwriting on common 70s conditions such as controlled diabetes, cardiac history, and COPD. Aetna, for instance, is known among independent agents for accepting conditions other carriers decline.

- Reasonable age and coverage limits. Some carriers cap new policies at 75 or 80, or reduce the maximum coverage at a certain age, which directly affects 70s buyers.

- Strong financial strength, such as an A.M. Best rating of A or higher, which matters even more when the claim window is shorter.

- Useful rider options, like an accelerated death benefit that pays early in the event of a terminal diagnosis.

How Carrier Underwriting Niches Affect 70s Applicants

Carriers carve out niches, and those niches matter most when the stakes are highest. Some companies underwrite 70s applicants more generously, accepting at a level plan what others would grade or decline. Others specialize in tobacco users, or price well in the early 70s but turn expensive later in the decade.

Mutual of Omaha, for example, considers insulin-using diabetics for level coverage when the diagnosis came at age 50 or older, while routing diabetic neuropathy to graded only. A different carrier may handle that same applicant entirely differently.

Age caps add another layer — some carriers stop at 75, others at 80 or 85 — which changes what is available depending on where you fall in the decade. The right company for a healthy 71-year-old non-tobacco applicant is frequently a very different company from the right one for a 76-year-old with diabetes and a cardiac history.

Why Direct-to-Carrier Shopping Often Falls Short in Your 70s

Going straight to one carrier in your 70s often produces a worse outcome than the market would allow — a decline when another company would have approved you, a graded offer when a level plan was achievable elsewhere, or simply a higher rate than comparison shopping would have surfaced.

This is the decade where that gap is widest, because carrier underwriting varies most here. Applying to a single company means betting that the one you picked happens to be the best fit for your exact age and health, which is rarely the case.

A more reliable path is a short phone conversation with an independent agent who can run your specific profile across multiple carriers at once and tell you, in writing, where you actually stand. Given how much timing and qualification matter at this age, that comparison is less about sales and more about making sure you see the full picture before you decide.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.