Home > Final Expense Insurance Cost > Final Expense Insurance in Your 80s

Final Expense Insurance in Your 80s for (2026)

Final expense insurance in your 80s is still a small whole life policy meant to cover funeral costs and final bills, but it works differently than it does at any younger age. The price is higher, the rules are tighter, and your choices are more limited. Most buyers in this age range should expect premiums that run from roughly $100 to well over $400 a month, depending on age, health, and how much coverage they want.

The 80s is the “qualify if you can” decade. Many carriers stop selling new policies at this age, guaranteed acceptance often becomes the main option, and family members frequently step in to help apply or pay the premium. The real question shifts from “what is the best coverage?” to “can I qualify for any coverage at all, and does buying it actually make sense?” This page is built to help you and your family work through that decision honestly.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

What Final Expense Insurance Looks Like in Your 80s — And Why This Decade Is Fundamentally Different

By your 80s, the conversation around burial insurance changes in a real way. The product itself is the same small whole life policy meant to cover funeral costs and final bills. What changes is how hard it is to get, how much it costs, and who ends up making the decision.

For most buyers at younger ages, the question is “what is the best coverage I can get?” In your 80s, the question often becomes “can I qualify for any coverage at all, and is buying it the right move?” That shift is what this page is built to help you and your family work through.

Why the 80s Is the Qualify-If-You-Can Decade

The 80s earns its name because the door starts to close. Most insurers cap guaranteed issue and final expense policies at age 85, though some carriers stop accepting new applicants at 80. A few specialty carriers go further, but the pool gets smaller every year.

Health-based plans get harder to win, too. Acceptance rates for plans that ask health questions drop sharply at 80 and older, and most applicants in this band end up in graded or guaranteed-issue coverage rather than level. Guaranteed acceptance, which asks no health questions at all, becomes the fallback for many people.

Premiums also climb to a point where the total math matters. And families step in more often, with adult children helping fill out the application, paying the premium, or driving the decision.

The Underwriting Environment in Your 80s

In your 80s, the realistic plan options narrow to graded benefit or guaranteed acceptance for most people. Level benefit, the plan that pays the full amount from day one at the lowest price, is reserved for the healthiest applicants at this age.

Qualifying for level benefit at 80-plus usually means no serious ongoing conditions. Carriers with the strictest health questions tend to set aside their lowest rates for seniors with no major uncontrolled conditions, while insulin-dependent diabetes, active cancer, COPD requiring oxygen, dialysis, or a recent heart attack or stroke push applicants elsewhere.

Expect a more thorough review than at younger ages. Even with no medical exam, the insurance company checks your prescription history. The carrier pool that issues to 80s applicants is small, and the group offering level benefit at this age is smaller still.

Who Should Buy Final Expense in Their 80s

Final expense insurance still makes sense for many people in their 80s. The clearest fit is the buyer who has not yet locked in coverage and whose family does not have other money set aside for funeral costs.

It also fits well when health is stable enough to qualify now and the premium is comfortable to pay. Good-fit situations include:

- A buyer whose income or savings can absorb the premium without strain.

- A couple where one spouse needs coverage and the other can pay the premium long-term.

- A family paying the premium on a parent’s behalf, where the family can sustain that payment for years.

The honest framing for this decade: 80s buyers and their families should look at the decision more carefully than at any earlier age, because the stakes are highest and the value is least automatic.

When 80s Buyers Should Not Buy

For some people in their 80s, the right answer is not buying at all. This is not a sales-friendly thing to say, but it is true, and a good agent will say it.

Buying is often the wrong call in these cases:

- Poor health with a short life expectancy, where total premiums would clearly pass the death benefit before it pays out.

- Substantial savings or assets already set aside that cover end-of-life costs.

- A premium that would force cuts to essentials like medication, food, or housing.

- Pressure from aggressive sales tactics when the family already has the means to cover final expenses.

If someone is steering an 80-something buyer toward an expensive policy they do not need, that person is not working in the buyer’s interest. Walking away can be the financially sound choice.

Average Final Expense Insurance Costs in Your 80s

This section fixes the decade and looks at what burial insurance actually costs across it. The numbers below are sample monthly premiums; your real rate depends on your exact age, gender, health, tobacco use, coverage amount, state, and carrier.

One note on the figures: rates this page cites are non-tobacco sample premiums drawn from 2026 carrier and market data. Guaranteed acceptance plans run higher than the health-question plans shown in most rate charts.

Final Expense Rates in Your 80s by Age and Coverage Amount

The table below shows approximate monthly premiums for non-tobacco applicants by age and coverage amount in the early-to-mid 80s. These reflect health-question (simplified issue) pricing where available; guaranteed acceptance costs more.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 80 | $140 | $208 | $277 |

| 81 | $150 | $224 | $297 |

| 82 | $161 | $239 | $318 |

| 83 | $172 | $255 | $339 |

| 84 | $182 | $272 | $361 |

| 85 | $193 | $288 | $383 |

| 86 | $226 | $338 | $449 |

| 87 | $265 | $395 | $525 |

| 88 | $303 | $453 | $602 |

| 89 | $341 | $510 | $679 |

Sample monthly rates for male applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 80 | $99 | $147 | $194 |

| 81 | $107 | $158 | $210 |

| 82 | $114 | $170 | $225 |

| 83 | $122 | $181 | $240 |

| 84 | $129 | $192 | $254 |

| 85 | $136 | $203 | $269 |

| 86 | $165 | $245 | $326 |

| 87 | $197 | $294 | $391 |

| 88 | $230 | $343 | $456 |

| 89 | $263 | $392 | $522 |

Sample monthly rates for female applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

How Premiums Climb Across Your 80s

The premium curve through the 80s is the steepest of any decade. Each year of age adds real cost, and the gap between buying early in the decade and late is large.

As a rough guide, expect on the order of $15 to $25 more per month for each year of age on a $10,000 policy. Over the span from 80 to 86, that adds up to a meaningful difference for the same coverage.

There is a second cost to waiting that money alone does not capture. Because many carriers stop accepting new applicants between 80 and 85, waiting can shrink the time horizon for the policy to pay out while also reducing the number of carriers willing to issue at all.

Why Coverage Amount Availability Narrows in Your 80s

In the 80s, you cannot always buy whatever coverage amount you want. Carriers cap face amounts more tightly as age rises, and the cap can drop from one age to the next.

The pattern looks like this:

- Many carriers cap coverage around $15,000 to $25,000 for 80s applicants, and some lower it further past 85.

- Caps can shift year to year and carrier to carrier; a company offering $15,000 at 80 may offer only $10,000 at 84, while another keeps the same limit through 85.

- Guaranteed acceptance plans usually cap lower than health-question plans, often in the $10,000 to $12,000 range, sometimes less.

- $25,000 from one policy is severely limited in the 80s, and $30,000 is essentially unavailable.

The honest framing: you get the coverage that your age, health, and the willing carriers allow, not simply the amount you have in mind. This is one more reason that comparing several carriers matters.

How Tobacco Use Changes Costs in Your 80s

Tobacco use raises your premium at every age, and the 80s are no exception. A “yes” on the tobacco question commonly adds about 30% to 40% to the premium. At 80s coverage amounts, that can mean $50 to $120 or more in extra monthly cost.

One thing is specific to this decade: there is very little runway to undo it. Most carriers treat you as a non-tobacco user once you have been tobacco-free for 12 months. But at this age, the window to enjoy the savings from re-rating later is short.

For most tobacco users in their 80s, locking in coverage now, even at tobacco rates, tends to produce a better total outcome than waiting to quit and re-rate. The math on waiting rarely favors delay at this age.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 80 | $182 | $272 | $361 |

| 81 | $193 | $289 | $384 |

| 82 | $205 | $306 | $407 |

| 83 | $220 | $328 | $436 |

| 84 | $238 | $355 | $472 |

| 85 | $258 | $386 | $513 |

| 86 | $378 | $565 | $752 |

| 87 | $434 | $649 | $864 |

| 88 | $490 | $733 | $976 |

| 89 | $546 | $817 | $1,088 |

Sample monthly rates for male applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 80 | $136 | $202 | $268 |

| 81 | $148 | $220 | $292 |

| 82 | $161 | $240 | $319 |

| 83 | $175 | $261 | $348 |

| 84 | $192 | $287 | $381 |

| 85 | $211 | $315 | $419 |

| 86 | $248 | $371 | $493 |

| 87 | $288 | $430 | $572 |

| 88 | $327 | $489 | $651 |

| 89 | $367 | $548 | $730 |

Sample monthly rates for female applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

How Health Conditions Affect Costs in Your 80s

Health has its biggest effect on both price and qualification in the 80s. Most chronic conditions push applicants out of level benefit and into graded benefit or guaranteed acceptance, even when the condition is well controlled.

Some conditions can stop an application entirely. Insulin-dependent diabetes, active cancer, COPD requiring oxygen, dialysis, or a recent heart attack or stroke within two years commonly move applicants away from the lowest-cost plans, and the strictest carriers may not accommodate them at all.

The honest framing: a person who would have qualified for level benefit at 65 often finds themselves limited to graded or guaranteed acceptance at 82. The effect on availability and price is most dramatic here.

How Much Coverage Most People in Their 80s Actually Buy

Choosing a coverage amount in your 80s is a different exercise than it is at younger ages. The goal is not the largest policy you can find. It is the smallest amount that covers the real need at a premium you can comfortably keep paying.

The Most Common Coverage Amounts for 80s Buyers

Most buyers in their 80s land between $5,000 and $15,000 of burial insurance. Where they fall inside that band usually tracks age and budget.

In practice, the pattern looks like this:

- $5,000 to $10,000 is common for late-80s buyers and those on tighter fixed incomes.

- $10,000 to $15,000 is common for early-80s buyers with stable finances.

- $20,000 or more is uncommon in the 80s, both because carrier availability at higher face amounts narrows and because the premium becomes hard to sustain.

These amounts line up with what funerals actually cost. The median funeral with burial reached $8,300 in 2023, and 2026 estimates put it closer to $9,000 to $10,500 once cemetery and inflation costs are added. A $10,000 to $15,000 policy covers most of that without a large out-of-pocket gap.

Why Smaller Coverage Amounts Often Make More Sense in Your 80s

The financial math shifts in your 80s in a way it does not at younger ages. Because premiums are high, the total you pay in over time can approach the death benefit itself.

Here is the shape of it. A buyer at 82 paying around $200 a month for $15,000 of coverage could pay roughly $24,000 over a 10-year life expectancy. At that point the policy returns less than you put in, or close to it.

Smaller amounts often produce better value at this age. A $5,000 to $10,000 policy keeps the total premium burden manageable while still providing meaningful funeral funding. The honest version of the question shifts from “how much coverage do I want?” to “what is the smallest amount that meets the real funeral need at a premium I can sustainably afford?”

When 80s Buyers Should Stretch for More Coverage

Stretching for more coverage in the 80s is sometimes the right call. The deciding factor is almost always whether the premium is genuinely sustainable for whoever is paying it.

Larger coverage can make sense when:

- There is substantial outstanding debt or expected medical bills that would otherwise fall to the family.

- Adult children would meaningfully benefit from inheritance support and can help carry the premium.

- The family has the financial capacity to support a higher premium for the long term.

- One spouse can comfortably afford the premium covering both eventual funerals.

The key word is sustainable. A larger policy only helps if it stays in force, which means the payment has to fit the budget for years, not just at signing.

When 80s Buyers Should Accept Smaller Coverage

For many people in their 80s, accepting a smaller amount is the smarter financial move, and no one should feel pressured into a larger face amount that strains their security.

Smaller coverage is often right when:

- The plan is direct cremation rather than a traditional burial. Cremation with a memorial service commonly runs about $3,000 to $7,000.

- There are existing savings already earmarked for final expenses.

- The applicant is single with no dependents.

- A higher premium would force cuts to essentials like medication, food, or housing.

- The family can contribute to funeral costs without insurance.

Buying less coverage you can keep beats buying more coverage you have to drop later. That trade-off carries the most weight in this decade.

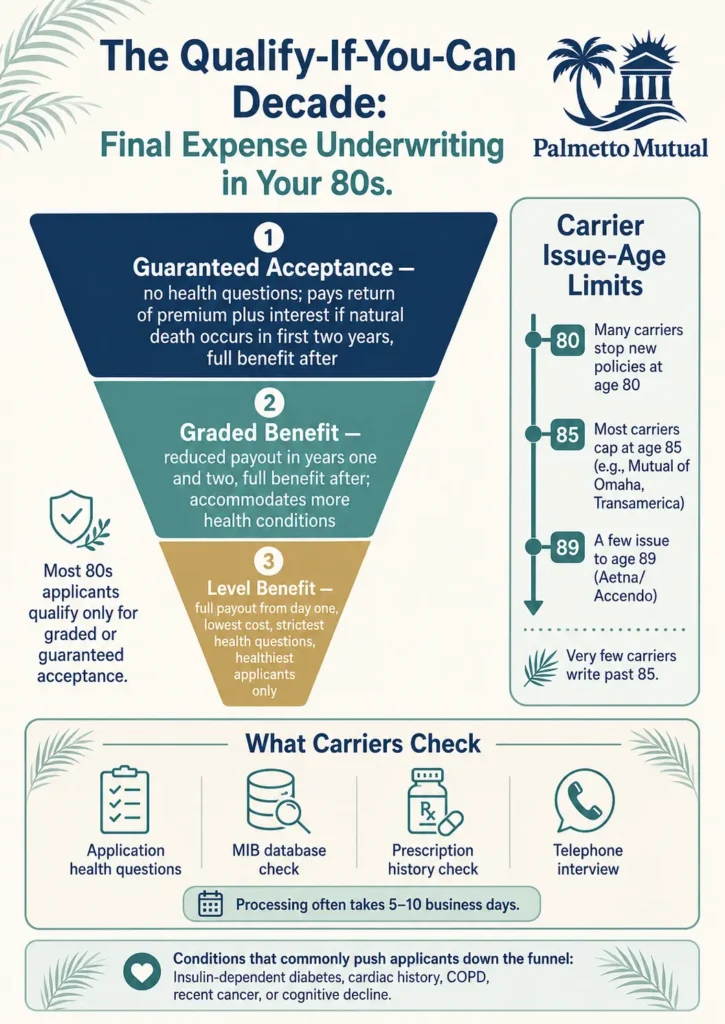

How Final Expense Underwriting Works in Your 80s

Underwriting is where the 80s feel most different. Carriers apply their closest scrutiny to applicants at this age, and the realistic plan outcomes narrow accordingly. Knowing what the carrier looks at helps you and your family go in with accurate expectations.

What Carriers Actually Evaluate for 80s Applicants

Even without a medical exam, final expense underwriting checks several things behind the scenes. For 80s applicants, those checks tend to be thorough rather than light.

A typical review pulls from these sources:

- The health questions on the application, which get a detailed read at this age.

- A Medical Information Bureau (MIB) database check, which flags serious impairments.

- A prescription history check, which cross-references your medications against your answers.

- A telephone interview, common at this age, to confirm the health information.

Because of these added steps, an 80s application often takes several business days to process rather than the near-instant decisions younger, healthier applicants sometimes get. Expect a more careful process, and answer the health questions accurately, since the prescription and MIB checks are designed to catch mismatches.

Why Most 80s Applicants End Up at Graded Benefit or Guaranteed Acceptance

Most people in their 80s do not qualify for level benefit, the plan that pays the full amount from day one. The reason is simple: the conditions and medications that would still allow level coverage at 65 routinely push 80s applicants into graded or guaranteed acceptance.

A quick guide to the three plan tiers helps here:

| Plan tier | Day-one payout | Underwriting |

|---|---|---|

| Level benefit | Full death benefit immediately | Strictest health questions |

| Graded benefit | Reduced in years one and two, full after | Moderate; accommodates more conditions |

| Guaranteed acceptance | Return of premiums plus interest if death is natural in first two years; full after | No health questions |

The carrier-by-carrier differences that create real qualification gaps in the 70s are more compressed in the 80s, since most carriers apply similarly strict standards at this age. The honest expectation: graded benefit or guaranteed acceptance are the realistic options for most 80s buyers, with level benefit reserved for the healthiest.

Common 80s Health Conditions and How They Affect Qualification

How a specific condition affects qualification varies by carrier, but some general patterns hold at this age. The table below is a guide to typical outcomes, not a guarantee, since each carrier underwrites differently.

| Condition | Typical outcome in your 80s |

|---|---|

| Controlled high blood pressure | Level Day 1 Coverage |

| Type 2 diabetes, oral medication | Level Day 1 Coverage |

| Type 2 diabetes, insulin | Level Day 1 Coverage |

| Cardiac history | Level Day 1 Coverage |

| COPD | Level Day 1 Coverage |

| Recent cancer, within 2 to 3 years | Typically guaranteed acceptance |

| Cognitive decline or dementia | Typically guaranteed acceptance |

One important nuance: timing matters. Some carriers apply a two-year look-back on cardiac events like heart attacks, stents, or strokes, meaning the same history can produce a better offer once enough time has passed.

Why Some 80s Applicants Get Declined Entirely

Declines tend to come from a few directions:

- Some carriers simply stop issuing new policies after 80, and others after 85.

- Some will not issue to applicants with specific conditions regardless of age.

- Some flag a recent hospitalization, cardiac event, or cognitive concern as too high a risk.

A decline from one carrier does not mean you are uninsurable. Underwriting standards differ, so the right next step is to shop other carriers rather than assume no coverage exists.

When Multi-Carrier Underwriting Helps in Your 80s

At younger ages, shopping multiple carriers is mostly about finding a lower rate. In your 80s, the bigger payoff is finding a carrier willing to issue at all.

Because standards differ, the practical wins look like this:

- An applicant declined by one carrier often finds approval at another with different criteria.

- An applicant offered guaranteed acceptance at one carrier is sometimes offered graded benefit at another, with meaningfully better economics.

- A specialist in older-age underwriting may accept a profile that a generalist treats as an edge case.

This is the decade where multi-carrier expertise produces the largest qualification differences, even though rate variation is more compressed than at younger ages.

Should You Lock In Final Expense in Your 80s — Or Wait?

The buy-now-versus-wait question carries different weight in your 80s than at any earlier age. At younger ages, waiting mostly means paying more later. In your 80s, waiting can mean losing the ability to buy at all.

The Real Cost of Waiting From Your 80s Into Late 80s

The premium jump from the early 80s to the late 80s is steep. A $10,000 policy that runs roughly $150 to $220 a month at 82 can run closer to $280 to $380 or more at 87 for the same coverage.

But premium is not the biggest issue. Availability is. Because many carriers stop accepting new applicants between 80 and 85, waiting from 82 to 87 can mean losing access to most of the market, not simply paying a higher rate.

The honest framing: in your 80s, waiting often means losing access to coverage altogether rather than just paying more for it.

Why Health Changes During Your 80s Often Eliminate Buying Options Entirely

Health in the 80s can change quickly, and each change tends to narrow the options. An applicant can move from qualifying for graded benefit, to qualifying only for guaranteed acceptance, to being declined by every carrier, in a relatively short span.

Events that commonly trigger that slide include a new cancer diagnosis, a heart attack or stroke, significant cognitive decline, or a hospitalization for a chronic condition. Any one of them can take a final expense policy off the table.

The honest framing: waiting through the 80s is a bet that your health stays steady. At this age that bet frequently loses, and the cost of losing is permanent uninsurability, not just a higher premium.

When Locking In at 80 Substantially Beats Locking In at 85

Buying early in the decade carries real advantages over waiting just a few years. The case for locking in at 80 rather than 85 rests on three points.

The premium is meaningfully lower, often $80 to $120 or more per month less for the same coverage. The carrier pool willing to issue is largest at 80 and shrinks each year after. And underwriting outcomes are most favorable at the youngest 80s ages, when fewer health flags have accumulated.

Put together, the buyer who locks in at 80 usually pays less over the life of the policy and faces a far lower chance of being declined than the buyer who waits to 85.

When 80s Buyers Reasonably Wait

Few 80s buyers benefit from waiting, but a handful of situations are legitimate. These are exceptions, not the rule.

Reasonable reasons to wait can include:

- Poor health with a limited life expectancy, where the better question is whether buying makes financial sense at all.

- Waiting out a specific medical situation that may improve the underwriting outcome within a few months.

- Arranging the logistics of a family-paid premium structure before applying.

Even in these cases, the risk of waiting is the highest of any age. Anyone choosing to wait should do so with clear eyes about the chance of losing access entirely.

Why Lapsing a Policy You Can’t Afford Is Worse Than Buying Less Coverage

A common and costly mistake in this decade is buying more coverage than the budget can sustain, then dropping the policy when the premium becomes unaffordable. That outcome loses both the coverage and the money already paid in.

Lapsing a final expense policy in the 80s can mean walking away from thousands of dollars in premiums with nothing to show for it. The cash value on these small whole life policies is modest, so a lapse usually is not recoverable in any meaningful way.

The honest framing: buying less coverage at a premium you can keep always beats buying more coverage that lapses. Decide the sustainable monthly premium first, then size the coverage to fit it, not the other way around.

Best Carrier Considerations for Buyers in Your 80s

Shopping carriers in your 80s follows a different logic than at younger ages. The priority order flips. Instead of chasing the lowest rate first, you are looking for a carrier willing to issue at all.

Why Carrier Selection Works Differently in Your 80s

At younger ages, carrier selection is largely a hunt for the best price. In your 80s, it is first a hunt for availability. Some carriers stop new business at 80, some at 85, and only a few go beyond.

Beyond simple availability, carriers differ in what they offer 80s applicants: better plan-tier options, more lenient underwriting, or more reasonable rates within the limited pool. The honest framing for this decade: shop for availability first, qualification second, and rate third, which is the reverse of the priority order that makes sense at younger ages.

Which Carriers Actually Issue to 80s Applicants

The pool of carriers willing to write coverage past 80 is smaller than most people expect, and it thins further past 85. A handful of carriers specialize in older applicants and treat them as a core market rather than an edge case.

A few carriers commonly come up at these ages:

- Mutual of Omaha and Transamerica both issue to age 85, with Mutual of Omaha often among the lowest-cost options.

- Aetna issues up to age 89, one of the highest issue-age ceilings in the market, and prices within a few dollars of the cheapest carriers at 80-plus.

- AIG and other niche carriers are frequently cited for flexible underwriting on higher-risk applicants.

The right carrier for an 82-year-old is often a specialist in older-age underwriting rather than a generalist.

How Carrier Underwriting Niches Affect 80s Applicants

Carriers carve out niches, and at this age those niches matter a great deal. The same applicant can get very different offers depending on which carrier’s rules fit their profile.

Niche differences show up in several ways:

- Some carriers will offer graded benefit to an 80s applicant where another offers only guaranteed acceptance.

- Some continue issuing past 85 when most have stopped.

- Some allow higher face amounts, up to $20,000 to $25,000, where others cap at $15,000.

- Some apply a look-back window on conditions like cardiac events or cancer remission, which can move an applicant into a better tier once enough time has passed.

The right carrier for an 84-year-old managing type 2 diabetes is radically different from the right carrier for an 86-year-old in good health.

Why Multi-Carrier Shopping Matters Most in Your 80s for Different Reasons

At younger ages, comparing carriers mostly saves money. In your 80s, it changes outcomes that money alone cannot.

The differences that multi-carrier shopping can produce at this age include:

- Approval at a specialist carrier instead of a decline across the board.

- A graded-benefit offer instead of guaranteed acceptance, with meaningfully better economics.

- Access to $15,000 to $20,000 of coverage instead of a $10,000 cap.

This is precisely where an independent agency that can compare many carriers at once earns its place. Because the landscape is so constrained at these ages, talking through your specific age, health, and coverage need on a phone consultation is often the most reliable way to find the carrier that fits. Palmetto Mutual works as an independent broker across multiple carriers for exactly this reason.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.