Home > Final Expense Insurance Cost > 25,000 Final Expense Insurance

$25,000 Final Expense Insurance: Cost & Options

A $25,000 final expense insurance policy is a small whole life plan built to cover funeral costs, final medical bills, and other end-of-life expenses. At this size, the coverage usually does more than pay for a funeral — it can clear debts and still leave money behind for your family. That makes $25,000 the upper edge of the traditional final expense market, the point where buying coverage starts to look less like funeral planning and more like leaving a modest inheritance. What you pay each month depends on your age, your health, and whether you use tobacco, and the rate sections below break those numbers down in full.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a $25,000 level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

Who Should Consider a $25,000 Final Expense Plan — And Why This Tier Crosses Into Legacy Planning

At $25,000, the question changes. Smaller burial insurance policies are built to pay for a funeral and little else. A $25,000 plan does that and keeps going — it can clear debts and still leave money in your family’s hands.

That extra room is why this tier sits on a line. Below it, you are usually making a final expense decision. At $25,000, you may be making a legacy decision instead. This section helps you tell which one you are actually making.

Why $25,000 Sits at the Top of the Final Expense Market

$25,000 is a real breakpoint in this market, but not because no policy goes higher. Several simplified-issue burial insurance products reach $40,000 or even $50,000 for healthy applicants.

Where $25,000 becomes a true ceiling is on the easiest-to-qualify-for coverage. Guaranteed-issue policies — the ones with no health questions at all — are commonly capped right around $25,000, and most cap lower.

So $25,000 marks the point where two things happen at once. It is the top of what guaranteed and lenient products will offer, and it is where carriers start asking more health questions before they approve you. Above this amount, you are more likely to face tighter qualifying standards or get steered toward a larger whole life product built for higher face amounts.

Who $25,000 of Coverage Suits Best

This amount fits people who want full funeral coverage plus a real cushion left over. It is comprehensive coverage, not bare-minimum coverage.

You may be a strong fit if you:

- Want every funeral cost covered in any region, with money still remaining

- Carry $10,000 to $15,000 in debt or expect end-of-life medical bills

- Want to leave a modest but meaningful inheritance for children or grandchildren

- Have family who would otherwise chip in for your funeral, and want to spare them that

- Are in your 60s or early 70s, can comfortably afford the premium, and want the security of full coverage

The common thread is intent. People who do well at this tier want more than a paid-for funeral. They want to leave something behind, and $25,000 is enough to do both.

When $25,000 Still Falls Short

Sometimes $25,000 is not enough, and it is worth being honest about that. Final expense insurance is built for end-of-life costs, not for large financial obligations.

You may need more than this tier if you:

- Want one policy to cover both spouses’ eventual funerals, where $40,000 to $50,000 fits better

- Carry large debts like a sizable mortgage, business obligations, or heavy credit card balances

- Are planning premium services with significant family travel and extended ceremonies

- Mainly want to leave a real inheritance rather than cover final costs

If leaving a larger legacy is your main goal, a traditional whole life or simplified-issue whole life product may serve you better than a burial insurance policy. The tool should match the job.

When $25,000 Crosses Into Overbuying for Single Applicants

The opposite can also be true. For some single applicants, $25,000 is more coverage than the situation calls for, and a smaller policy would do the same work for less money each month.

You may be overbuying if you:

- Plan a direct cremation or a simple service in a lower-cost area

- Already have savings or a paid-off home that covers your end-of-life needs

- Have no dependents or close family who would benefit from the leftover money

- Are on a fixed income where the $25,000 premium strains your budget month after month

Buying more coverage than you need is not a free choice. The premium follows you for life. If a $15,000 policy covers your real costs, paying for $25,000 ties up money you may want elsewhere.

When the Final Expense vs. Traditional Whole Life Question Becomes Real

Here is the part most sellers skip. At $25,000 of coverage, healthier applicants in their 50s and 60s should genuinely ask whether a regular whole life or simplified-issue whole life policy — from a carrier that does not specialize in final expense — would price better.

The reason is how this product is built. Final expense underwriting is fast and forgiving, and you pay for that. Carriers charge more per dollar of coverage because they accept people with health issues and skip the medical exam.

For a 60-year-old in good health, that trade may not be worth it. If you can comfortably pass fuller underwriting, a traditional whole life policy at $25,000 can cost less per month than the same coverage bought as final expense. We say this plainly because it points away from our own category when that is the right call: if you are healthy enough to qualify the traditional way, get both kinds of quotes before you decide.

What Does $25,000 Cover — From Funeral Costs to Family Financial Protection

At smaller coverage amounts, the question is “will this pay for the funeral?” At $25,000, that question is usually already answered. The real question becomes “what is my family receiving beyond the funeral?”

That shift is the whole point of this tier. Funeral insurance at $25,000 is rarely consumed entirely by the funeral itself. The leftover is the part worth planning for.

The Full Cost of an Upper-Tier Traditional Funeral in 2026

Start with the funeral. The national median cost of a funeral with viewing and burial is $8,300, and a funeral with cremation and viewing runs $6,280 (NFDA 2023 General Price List Study).

But those medians leave out cemetery costs — the plot, the vault or grave liner, and the monument. Add those, and a traditional burial commonly lands near or above $10,000. Buyers at the $25,000 tier often have specific upgrade preferences that push the number higher still.

The upgrades that drive cost most are:

| Upgrade category | Typical 2026 range |

|---|---|

| Premium or custom casket | $2,500 to $22,000 |

| Burial vault or grave liner | $900 to $7,000 |

| Mausoleum entombment (single crypt) | $4,000 to $17,000+ |

| Headstone or monument | $1,000 to $3,500 |

| Embalming and extended viewing | $775+ |

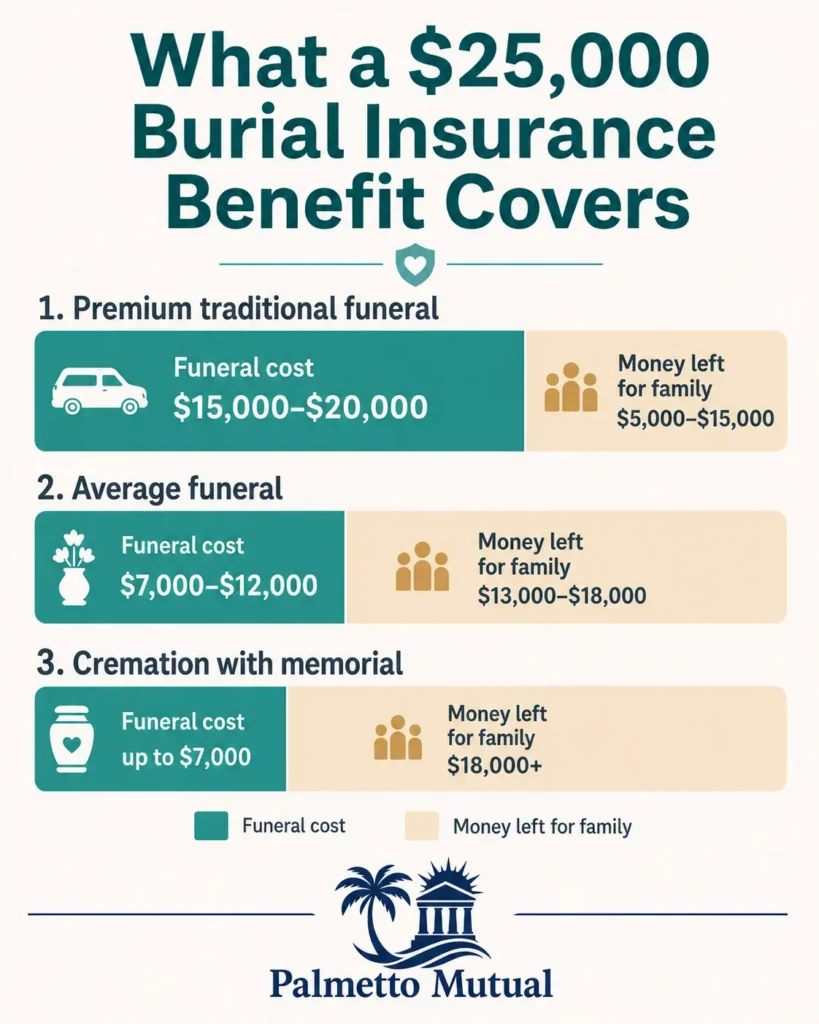

A premium traditional funeral — custom casket, mausoleum entombment, extended viewing, full services — can realistically reach $15,000 to $20,000. That is the upper edge of what this coverage tier is built to absorb.

How $25,000 Covers Any Funeral With Substantial Buffer Remaining

Even at the high end, $25,000 covers the funeral and leaves money behind. After a premium service in a costly region, you can still expect roughly $5,000 to $15,000 remaining, depending on your choices and where you live.

That buffer is real money with real jobs. It can:

- Clear medical bills from end-of-life care

- Pay off meaningful debt

- Cover several months of household expenses for a surviving spouse

- Provide direct financial support to family during a hard transition

This is the favorable case for the tier. Burial insurance at $25,000 rarely leaves your family scrambling, even when funeral choices are generous.

$25,000 for Average and Modest Funeral Choices — Significant Funds Remain

For average or modest services, the leftover grows. Against a funeral in the $7,000 to $12,000 range, $25,000 leaves roughly $13,000 to $18,000 available beyond funeral costs.

At that gap, the death benefit stops being funeral funding and becomes a genuine financial event for your family. This is the point where you should consciously decide who receives the remaining money and what you want it to do.

That decision is worth making on purpose. Money left without a clear intent still helps, but money left with a plan — for a spouse, a grandchild, a specific need — does more.

$25,000 for Cremation Buyers — Funeral Costs Become a Small Fraction

For cremation buyers, the math tilts even further. Even cremation with a full memorial service rarely exceeds about $7,000, which leaves $18,000 or more available (NFDA cremation median $6,280, 2023).

At that point, the funeral is a small slice of the benefit. A cremation-focused buyer choosing $25,000 is, in plain terms, making a legacy decision, not a final expense decision.

That is not wrong — but it is worth naming. If most of your benefit is meant for family rather than your funeral, it is fair to ask whether a final expense policy is the best-priced way to leave that money, or whether a different life insurance product would serve the goal better.

How Families Actually Use $25,000 Death Benefits

The death benefit is paid as a tax-free cash lump sum, usually within days, and your family can use it however they need. There are no rules tying it to the funeral.

At this coverage amount, families commonly use the money to:

- Clear all remaining medical and credit card debt

- Give a surviving spouse 6 to 12 months of household expenses during transition

- Help adult children with funeral travel and time off work

- Leave a meaningful inheritance for grandchildren

- Fund a college savings goal the deceased cared about

- In some cases, pay down a remaining mortgage balance on the family home

The pattern is clear: at $25,000, funeral life insurance is doing two jobs at once. It buries the cost of dying, and it hands the family a real financial head start at the same time.

$25,000 Whole Life Rates by Age (Non-Tobacco Applicants in Good Health)

This is the headline rate section for the most common buyer: a non-tobacco applicant in reasonably good health. Before the numbers, it helps to understand what drives them.

How $25,000 Whole Life Pricing Works at the Top of the Final Expense Market

Carriers price a burial insurance policy on four things: your age when you apply, your gender, your tobacco status, and your health tier. Once the policy is issued, the premium is locked. It never goes up, and the death benefit never goes down.

At $25,000, you are near the upper edge of simplified-issue underwriting — the path where you answer health questions but take no medical exam. Most carriers will write $25,000 this way, but several apply slightly stricter health standards at this face amount than they do at $15,000 or $20,000.

That can mean a few extra health questions, or an occasional prescription or medical-record check for borderline applicants. The practical takeaway: the carrier that gives one person the best $25,000 rate is not always the same carrier that does for the next person. Comparing across carriers is where the savings live.

$25,000 Whole Life Monthly Rates by Age

The table below shows sample monthly premiums for non-tobacco applicants in good health, by age and gender.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $72 | $56 |

| 55 | $86 | $65 |

| 60 | $105 | $78 |

| 65 | $137 | $98 |

| 70 | $182 | $129 |

| 75 | $246 | $177 |

| 80 | $345 | $242 |

Sample monthly rates for level benefit at $25,000 of coverage, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

Two patterns hold across nearly all carriers. Premiums rise steadily with age, and women pay less than men for the same coverage because women live longer on average.

That gender gap is most visible at this coverage level. Because the premium scales with the death benefit, the dollar difference between a man and a woman of the same age is wider at $25,000 than it is on a small policy — so for couples pricing coverage together, it is worth quoting each person separately rather than assuming one rate fits both.

Why $25,000 Rate Variation Across Carriers Becomes Substantial

Every carrier uses its own pricing formula, so two people with identical profiles can get very different quotes. The same applicant can see monthly premiums vary by 30% or more across carriers for the exact same coverage.

At $25,000, that percentage turns into serious money. A gap that looks like $30 or $40 a month is real every month, for life — and over a 20-year policy, the difference between the most and least competitive carrier compounds into thousands of dollars in total premium paid.

This is why shopping multiple carriers at $25,000 is not a nice-to-have. The coverage is identical from carrier to carrier; only the price changes. An independent broker shops the same profile across many carriers at once, which is the practical way to land the lowest rate you qualify for.

Why the Cost-of-Waiting Math Hits Hardest at $25,000

Because the premium locks at the age you buy, waiting has a permanent price. A 60-year-old who locks in $25,000 today pays that fixed rate for life. The same person waiting until 70 will pay a markedly higher rate — final expense premiums climb steeply through the late 60s and 70s.

Waiting also risks more than price. If your health changes before you buy, you may no longer qualify for the best level-benefit rate. At $25,000, a downgrade from level to graded benefit does not just raise the premium — it changes the payout structure for the first two to three years, which we cover in detail in the graded section below.

So the cost of waiting at this tier is two costs stacked together: a higher locked-in premium, plus the risk of a worse benefit structure if your health shifts. Both get larger the longer you wait.

Whether $25,000 Final Expense Beats Traditional Whole Life at Your Age and Health

For healthy applicants in their 50s and early 60s, this is the honest question to ask. Final expense pricing carries a built-in premium for its lenient underwriting and fast approval — you pay extra per dollar of coverage for that convenience whether you need it or not.

If you can comfortably pass fuller underwriting, a simplified-issue or traditional whole life policy from a non-final-expense carrier may price better at $25,000. The leniency you would be paying for is only worth it if your health actually requires it.

The fair move is to compare both before deciding. A good broker will price funeral life insurance against broader whole life options and tell you which one wins for your age and health — even when the answer points outside the final expense category.

$25,000 Whole Life Rates by Age (Tobacco Users)

This section mirrors the one above, but for tobacco users. The structure is the same; the prices are higher, and the underwriting details matter more.

What Tobacco Use Adds to a $25,000 Premium

Tobacco use raises your rate because it shortens average life expectancy, so carriers price it as higher risk from day one. The surcharge commonly runs about 30% to 50% above non-tobacco rates.

At $25,000, that percentage becomes a large monthly figure, especially at older ages — and because the premium is locked for life, that gap compounds dramatically over the years you hold the policy.

One wrinkle matters before you assume you’ll pay tobacco rates: carriers do not all define “tobacco user” the same way. Cigarettes always count. Cigars, pipes, vaping, and smokeless are handled differently from carrier to carrier, and look-back windows vary, usually between 12 and 24 months. Those differences are exactly why carrier matching matters so much at this tier.

$25,000 Whole Life Tobacco Rates by Age

The table below mirrors the non-tobacco structure, showing sample monthly premiums for tobacco users.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $91 | $74 |

| 55 | $115 | $92 |

| 60 | $144 | $108 |

| 65 | $195 | $137 |

| 70 | $264 | $182 |

| 75 | $358 | $245 |

| 80 | $511 | $333 |

Sample monthly rates for level benefit at $25,000 of coverage, tobacco. Rates require answering health questions, and approval is not guaranteed.

Read this table against the non-tobacco table above to see the surcharge in real dollars at your age. The gap is widest in absolute terms at the older ages, where the base premium is already high.

Re-Rating to Non-Tobacco After Quitting — Major Long-Term Savings at $25,000

Here is the part most TV-advertised products never mention. Many carriers will reclassify you to non-tobacco rates after you have been tobacco-free for a set period — often 12 to 24 months, depending on the carrier.

At $25,000, that re-rating is worth real money over the life of the policy, because the surcharge you shed applies to every remaining monthly premium. The shorter the carrier’s required tobacco-free window, the sooner those savings start.

This is where carrier choice at purchase pays off later. Palmetto Mutual works exclusively with carriers that use a 12-month tobacco look-back, which is the most favorable end of that range — it means a buyer who quits can reach the earliest possible re-rating window rather than waiting two years or longer. If quitting is on your horizon, the look-back period your carrier uses is worth asking about before you sign.

Carrier-Specific Tobacco Underwriting Becomes Critical at $25,000

The granular underwriting nuance carries major dollar stakes at this tier. The difference between a 12-month and a 24-month look-back at two carriers can decide whether a recent quitter is classed as tobacco or non-tobacco — and at $25,000, that classification is worth thousands of dollars over the policy’s life.

Tobacco type matters too, but less forgivingly than many buyers hope:

- Cigarettes are always rated as tobacco use, at every carrier, even one cigarette in the look-back window.

- Cigars, pipes, vaping, and smokeless are rated the same as cigarettes at roughly 95% of final expense carriers once any use is reported.

- A narrow set of carriers rates cigarette use only — meaning an occasional cigar user can sometimes qualify for non-tobacco rates with the right carrier. This is the exception, not the rule.

The point is not that cigar or vape users usually escape the surcharge — at most carriers they do not. The point is that the small number of carriers with favorable tobacco rules are worth finding, because at $25,000 the difference is large. Matching your specific tobacco history to the right carrier is one of the highest-leverage decisions in the whole purchase, and it is exactly the kind of matching an independent broker does for you.

$25,000 Graded Benefit Policy Rates by Age

Graded benefit is the middle tier of burial insurance. It is for applicants who have some health issues — enough to miss the best level-benefit rates, but not enough to be limited to the highest-risk products. At $25,000, this tier carries real weight, so it is worth understanding before you read the rates.

How Graded Benefit Works on a $25,000 Policy

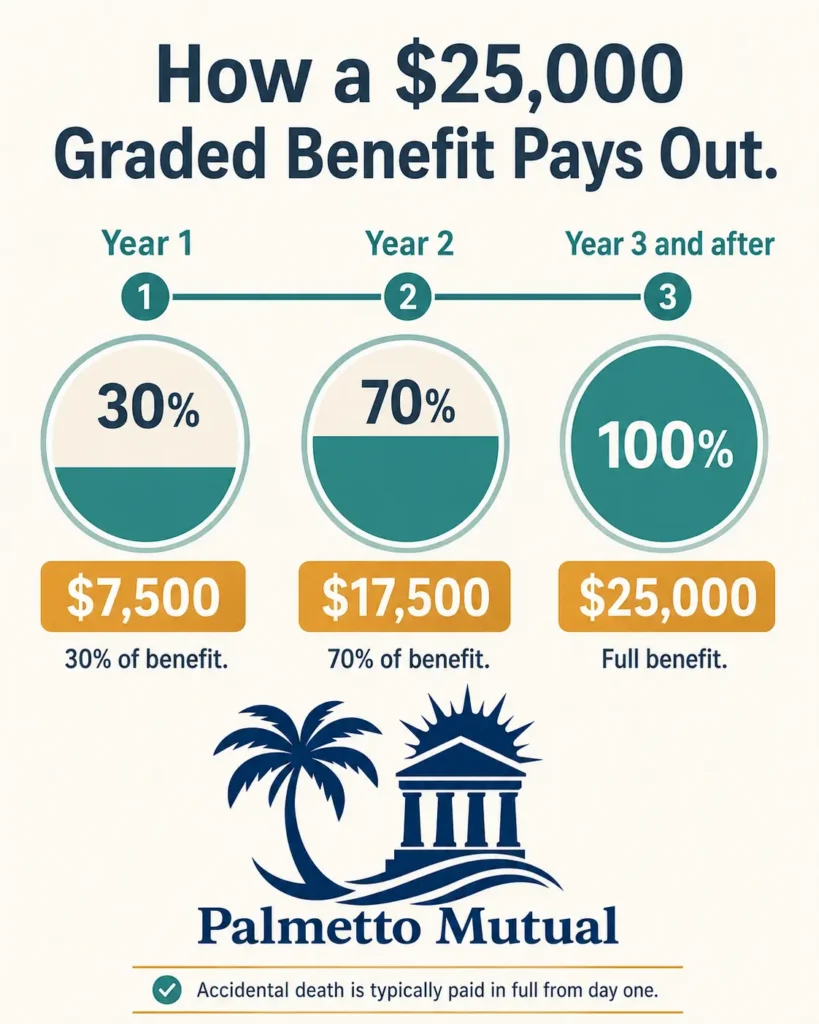

A graded benefit policy limits the payout for the first two years, then pays in full. The most common structure pays 30% of the death benefit in year one, 70% in year two, and 100% from year three onward.

On a $25,000 policy, that math is concrete:

| Timing of death (natural causes) | Amount paid |

|---|---|

| During year one | $7,500 (30%) |

| During year two | $17,500 (70%) |

| Year three and after | $25,000 (100%) |

Accidental death is typically paid in full from day one. Some carriers use a different structure called modified or return-of-premium, which pays back your premiums plus interest (often around 10%) instead of a percentage during the first two years. It is worth confirming which structure a given policy uses before you buy.

At $25,000, those partial payouts are substantial. A $17,500 payout in year two is meaningful protection — and it is the kind of first-years coverage that the highest-risk guaranteed acceptance products generally do not provide at this face amount, since those carry a full two-year wait.

$25,000 Graded Benefit Monthly Rates by Age

The table below shows sample monthly premiums for a $25,000 graded benefit policy by age and gender.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $91 | $73 |

| 55 | $118 | $92 |

| 60 | $144 | $111 |

| 65 | $187 | $144 |

| 70 | $258 | $193 |

| 75 | $369 | $269 |

| 80 | $562 | $404 |

Sample monthly rates for graded benefit at $25,000 of coverage. Graded benefit plans pay a reduced amount if death occurs during the first two policy years. Rates require answering health questions, and approval is not guaranteed.

Graded benefit premiums run higher than level benefit premiums for the same coverage, because the carrier is accepting more health risk. Read these figures against the level-benefit table earlier on the page to see the difference in real dollars at your age.

Why Graded Benefit Is Often the Only Path to $25,000 for Health-Compromised Applicants

For applicants with moderate health conditions, graded benefit is frequently the practical way to secure $25,000 of meaningful coverage from a single funeral insurance policy. The reason is what the alternatives give up.

If you do not qualify for level benefit, your other option is the highest-risk, no-health-questions product. But those products pay nothing close to the full benefit in the first two years — typically just premiums back plus interest if death is from natural causes during that window. Graded, by contrast, pays a real partial benefit from the start: $7,500 in year one and $17,500 in year two on a $25,000 policy.

[Verification flag for your pass: the outline frames single-policy $25K guaranteed-acceptance coverage as essentially unavailable, which my research did not confirm — $25K is commonly the GI cap, not an impossibility. The argument above does not depend on that claim, since graded’s first-two-years advantage over GI holds either way. Confirm GI availability against your current carrier panel.]

That difference is why accurate level-versus-graded qualification matters more at $25,000 than at any lower amount. The gap between what graded pays early and what the highest-risk products pay early is at its widest when the face amount is this large.

Who Lands in Graded Benefit at $25,000

Graded benefit is offered when the carrier sees moderate risk — health conditions that are real but not severe or recent enough to disqualify level coverage. Common profiles include:

- A severe health diagnosis one to two years in the past

- Controlled chronic conditions that exceed a carrier’s level-benefit thresholds

- Certain medications flagged in a prescription history check

- Severe heart conditions

- COPD with Oxygen use

There is one wrinkle specific to this coverage amount. Carriers often apply stricter level-benefit standards at higher face amounts, so an applicant who would qualify for level benefit at $10,000 or $15,000 can land in graded at $25,000. This is another reason carrier matching matters here — the same health profile can be classed differently at $25,000 depending on which carrier reviews it.

$25,000 Guaranteed Acceptance Rates by Age (Where Available)

[Verification flag for your pass: this section is written to the outline’s premise — that single-policy $25K guaranteed acceptance is essentially unavailable and must be assembled from combined policies. My research suggests $25,000 is more commonly the standard GI cap than an impossibility, so please verify single-policy availability against your carrier panel before publishing. Source notes below cite only claims the research supports; I have not attached citations to the availability premise.]

Guaranteed acceptance is the last-resort tier of burial insurance — no health questions, no medical exam, approval based on age alone. At $25,000, the practical challenge is availability, which is why this section is framed around reaching that amount rather than assuming a single policy delivers it.

Why $25,000 Guaranteed Acceptance Coverage Is Almost Nonexistent

Guaranteed acceptance products carry the most risk for the carrier, since they cannot screen out any health condition. To manage that risk, carriers limit how much guaranteed coverage they will write per policy — many cap well below $25,000, at $10,000, $12,000, or $15,000.

Because of those caps, an applicant who needs guaranteed coverage and wants a full $25,000 may not find it in a single policy from a given carrier in their state and age band. The common workaround is to combine policies from two different carriers to reach the total.

This is practical market knowledge that most generalist pages skip, because it does not point to one clean product to recommend. But for an applicant who genuinely needs this route, knowing it exists is the difference between giving up on $25,000 and assembling it.

How to Combine Policies to Reach $25,000 of Guaranteed Acceptance Coverage

The combination approach is straightforward in concept. An applicant takes a $15,000 guaranteed acceptance policy from one carrier and a $10,000 guaranteed acceptance policy from another, reaching $25,000 total with no health questions on either.

There are real trade-offs to weigh before going this route:

- Total cost is higher. Two combined policies will generally cost more than a single $25,000 level benefit policy would, because guaranteed acceptance is the most expensive coverage per dollar.

- Each policy has its own two-year contestability period. The standard two-year window applies independently to each policy, so both clocks run separately.

- You apply twice. The application happens with each carrier separately, and each policy is a separate contract to manage.

Carrying more than one policy is perfectly normal and allowed. The question is whether the combined cost and the doubled paperwork are worth it for the applicant, or whether accepting a lower single-policy amount would serve them better.

Combined Premium Costs for Multi-Policy GI Reaching $25,000

The table below approximates combined monthly premiums for a $15,000 plus $10,000 guaranteed acceptance combination by age and gender.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $109 | $85 |

| 55 | $144 | $110 |

| 60 | $159 | $127 |

| 65 | $212 | $156 |

| 70 | $247 | $188 |

| 75 | $348 | $270 |

| 80 | $617 | $440 |

Sample monthly rates for guaranteed issue coverage at $25,000. Guaranteed issue policies require no health questions and cannot be declined, but include a two-year waiting period before the full benefit is payable.

Combined guaranteed acceptance premiums at $25,000 run well above what graded benefit costs for the same total coverage. When you fill in these figures, place them next to the graded table above so the reader can see directly what the no-health-questions route costs compared to qualifying for graded.

The Cumulative Premium Reality on $25,000 Guaranteed Acceptance Coverage

Here is the math a buyer at this tier needs to see clearly. Because guaranteed acceptance premiums are high and rise sharply with age, the total premiums paid over time can approach or pass the death benefit itself.

For combined guaranteed acceptance policies totaling $25,000 bought at age 75, the premiums paid over a normal life expectancy can come close to or exceed the $25,000 benefit. Bought at 80 with a full life expectancy, cumulative premiums can run well beyond the benefit amount.

For some applicants in their late 70s and 80s, guaranteed acceptance is still the only option, because nothing else will take them. The goal here is not to scare anyone away from coverage they need — it is to make sure they choose it knowing what they will pay over time relative to what the policies will pay out.

When to Pursue $25,000 of GI Coverage — And When to Accept Less

Guaranteed acceptance at $25,000 is the right call for a specific applicant: someone who genuinely does not qualify for level or graded benefit, who genuinely needs the full $25,000 of immediate coverage, and who understands the cumulative premium math above.

It is the wrong call in two common situations:

- An applicant who would qualify for graded benefit but gets steered to guaranteed acceptance anyway. Graded is dramatically cheaper and provides real partial coverage from the first day. Being pushed past it is a costly mistake at $25,000.

- An applicant in their late 70s or 80s where the cumulative premium math is unfavorable. For some buyers at these ages, a smaller policy at an affordable premium serves them better than $25,000 they will overpay for.

One plain warning belongs here. At $25,000, anyone steering you toward guaranteed acceptance without first thoroughly checking whether you qualify for graded benefit is not working in your interest. The honest first step is always to test graded qualification, because for most health-compromised applicants it is the better deal — and that test is exactly what an independent broker should do before guaranteed acceptance is ever on the table.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.