Home > Final Expense Insurance Cost > 40,000 Final Expense Insurance

$40,000 Final Expense Insurance: Cost & Options

A $40,000 final expense insurance policy is a whole life plan built to cover funeral costs and final bills, then leave the rest behind for your family. For a healthy, non-tobacco applicant, monthly rates at this size commonly run from roughly $150 to $400 or more, depending mostly on your age and sex, with very few carriers offering this much coverage. At $40,000, you are also at the far outer edge of the burial insurance market, and for many buyers a simplified-issue whole life policy from a regular life insurance company is the better-priced and more honest choice.

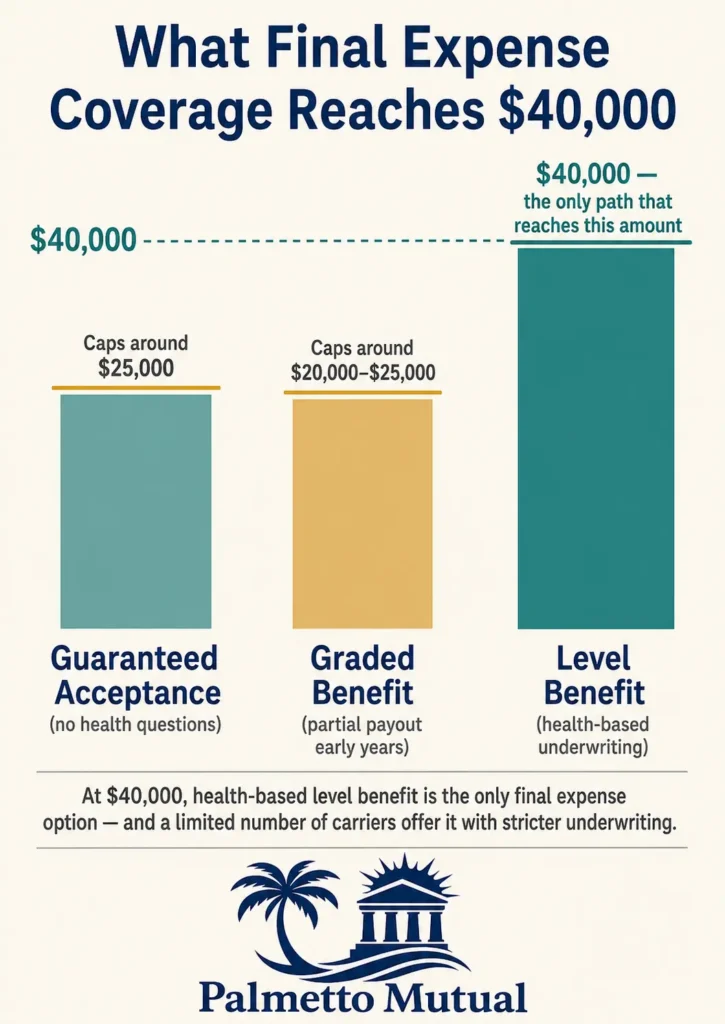

It also helps to know two limits up front. Graded benefit and guaranteed acceptance plans are not sold at $40,000, so health-based level benefit underwriting is the only path within the final expense category, and even that is offered by just a handful of carriers with stricter health questions than you would face at $20,000 or $25,000.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a $40,000 level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

Who Should Consider a $40,000 Final Expense Plan — And Why Most Buyers at This Level Should Compare Other Products First

A $40,000 plan sits at a point where final expense insurance stops being the obvious answer for most people. This section helps you decide whether you should be shopping for burial insurance at this size at all, or whether a different kind of life insurance would serve you better.

Why $40,000 Is at the Outer Edge of the Final Expense Market

Most final expense carriers build their products for smaller amounts. Industry reviews show typical burial insurance coverage running from about $2,000 up to $25,000, with a smaller number of carriers stretching to $40,000 or $50,000.

The carriers that do offer $40,000 ask more of you. Expect more detailed health questions, prescription history checks, and medical record reviews for borderline cases — underwriting that is noticeably stricter than what you would face at $20,000 or $25,000.

This is also the size where final expense pricing often loses to other products. Simplified-issue and traditional whole life from regular life insurance carriers frequently price better per dollar at $40,000, which is why many readers landing here would be better served by shopping life insurance more broadly.

Why Graded Benefit and Guaranteed Acceptance Aren’t Options at $40,000

Two common “easier approval” products simply do not exist at this size. Graded benefit plans, which pay a partial amount in the first year or two before reaching full value, are generally capped around $20,000 to $25,000.

Guaranteed acceptance plans — the kind with no health questions — top out lower. Most carriers cap guaranteed-issue coverage at $25,000, and many sit below that. No carrier offers $40,000 with no health questions, because the payout risk is too high to insure blind.

That leaves one path. At $40,000, health-based level benefit underwriting is the only way to get this much coverage inside the final expense category. If you cannot qualify for level benefit at $40,000, you cannot buy $40,000 of final expense on a single policy — you would need to combine smaller policies, accept less coverage, or move to a different product entirely.

Who $40,000 of Coverage Genuinely Suits

Some buyers have a real reason to want this much, and a real reason to get it through final expense rather than another route. The common thread is good health plus a need for speed or simplicity.

- Applicants in good health who specifically want simplified-issue underwriting and faster approval. Final expense often approves in roughly 24 to 48 hours, versus four to six weeks for fully underwritten traditional whole life.

- Retirees carrying meaningful debt, often in the $20,000 to $30,000 range, who want the policy to clear those balances.

- Couples who want one policy to cover both eventual funerals plus a meaningful amount left over.

- People with specific final wishes that run well above an average funeral.

- Buyers already declined by traditional life insurance carriers, for whom final expense underwriting is the only practical path to this amount.

When $40,000 Falls Short Even at This Coverage Level

If your real goal is passing on wealth or protecting a business, $40,000 is the wrong tool. Buyers focused on generational wealth transfer or business continuity are usually better served by $50,000 to $250,000 through traditional whole life or term life.

The same is true for couples with both significant combined debt and inheritance goals. Two separate policies, or one policy of $50,000 or more, often fits better than stretching a single $40,000 burial insurance plan to do everything.

The honest summary: at $40,000, if the underlying goal is meaningful wealth transfer, you are shopping in the wrong product category.

When $40,000 Is More Than Single Applicants Genuinely Need

The mistake can also run the other direction. Plenty of single applicants buy more than they need at this tier.

- Single applicants without dependents or close family who would actually use a large legacy fund.

- People with substantial savings or paid-off property that already covers end-of-life costs.

- Applicants whose adult children are financially independent and have said they neither need nor want an inheritance.

- Seniors on fixed incomes where a $40,000 premium creates real monthly strain.

Overbuying here is common and costly. The premium gap between $25,000 and $40,000 is large, and it is rarely worth it without a specific legacy or couples-coverage reason.

When Final Expense Is Almost Certainly the Wrong Product at $40,000

For most healthy applicants in their 50s and early 60s, this is the key point. Simplified-issue or traditional whole life from non-final-expense carriers usually offers materially better pricing for the same $40,000 — often well below final expense rates for the same person.

Final expense underwriting is faster and more forgiving, but you pay for that convenience. At $40,000, that convenience premium becomes a substantial monthly difference for the same applicant profile — money spent on lenient underwriting whether you need it or not.

So if you can comfortably qualify for traditional underwriting, which most healthy buyers in their 50s and early 60s can, pause here. Shop traditional and simplified-issue whole life before committing to final expense at $40,000. You will likely come out ahead.

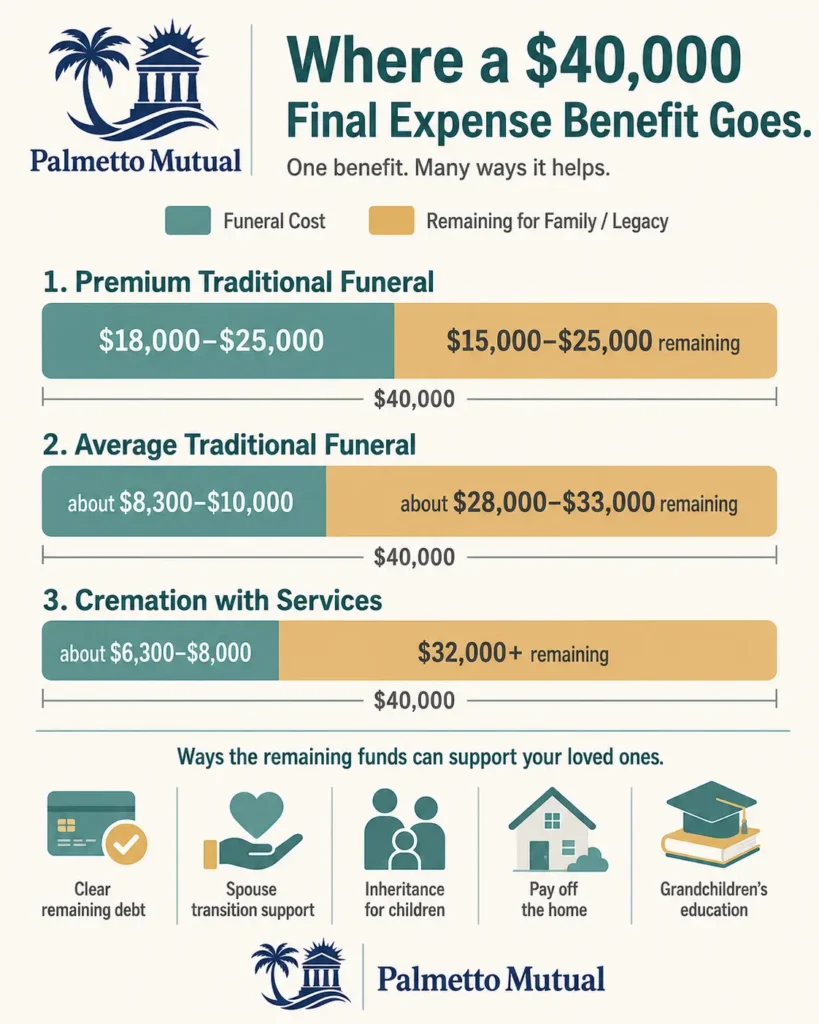

What Does $40,000 Cover — From Premium Funeral Services to Real Family Legacy

At smaller amounts, burial insurance is mostly about the funeral. At $40,000, the funeral becomes a small slice of what the death benefit actually does, and the real story is legacy planning.

The Cost of a Premium Traditional Funeral in 2026

A standard traditional funeral is well below $40,000. The NFDA reports a national median of about $8,300 for a funeral with viewing and burial, rising to roughly $9,995 once a vault is added.

The high end runs higher. A premium service — custom casket, mausoleum entombment, extended viewing, full services, family travel, and a reception — can reach the $18,000 to $25,000 range, especially in high-cost regions. A mausoleum alone can add several thousand dollars, and a private family walk-in mausoleum can run far more.

Buyers shopping at $40,000 rarely have an average funeral in mind. They usually have specific upgrades, multi-generational considerations, or regional costs that push the funeral toward that higher range.

How $40,000 Funds a Premium Funeral and Substantial Legacy

Even with premium funeral choices, a large share of the death benefit is left over. After a $18,000 to $25,000 service, roughly $15,000 to $25,000 or more remains for other purposes.

That leftover amount does real work for a family. Common uses include:

- Clearing remaining medical bills and credit card debt in full.

- Giving a surviving spouse a year or more of household expenses during a hard transition.

- Helping adult children with major life costs like a down payment, education, or a business.

- Leaving meaningful inheritances split among several beneficiaries.

- Paying down or paying off a remaining mortgage on the family home.

- Funding college savings for grandchildren.

$40,000 for Average Funeral Choices — Major Legacy Funds Remain

For buyers planning an average or modest traditional service, the gap is even wider. After a funeral in the $8,000 to $12,000 range, roughly $28,000 to $33,000 remains.

At that point, the death benefit is clearly a multi-purpose family event, not just funeral money. It covers immediate end-of-life costs, gives a surviving spouse transition support, and leaves a genuine legacy for children and grandchildren.

This is the tier where beneficiary structure deserves real thought. Think through whether you want a single beneficiary, several beneficiaries with specific percentages, contingent beneficiaries, or an irrevocable designation, so the money reaches the right people in the proportions you intend.

$40,000 for Cremation Buyers — Coverage Is Almost Entirely Legacy

For cremation-focused buyers, $40,000 is far beyond end-of-life need. The NFDA median for a funeral with viewing and cremation is about $6,280, and even cremation with full memorial services and family travel rarely tops $8,000.

That leaves $32,000 or more as pure legacy. And at that point, the decision is no longer really about funeral planning at all.

If you are cremation-focused and shopping at $40,000, you are almost certainly making a legacy decision, and final expense is rarely the right structure for it. Traditional whole life or simplified-issue whole life usually fits that goal better and prices better.

How Families Actually Use $40,000 Death Benefits

The death benefit is paid in cash, directly to your named beneficiary, and they can use it however they need. At this size, that use almost always tilts toward legacy rather than funeral costs.

In practice, families put $40,000 toward things like clearing all remaining debt, giving a surviving spouse a year or more of breathing room, helping adult children with major expenses, splitting an inheritance across several beneficiaries, funding grandchildren’s education, paying off the family home, seeding a family business, or finishing a financial goal the person had been working toward.

$40,000 Whole Life Rates by Age (Non-Tobacco Applicants in Good Health)

These rates apply to healthy applicants who do not use tobacco. Because graded benefit and guaranteed acceptance plans are not sold at $40,000, this is one of only two rate sections on the page — level benefit non-tobacco here, and tobacco rates in the next section.

How $40,000 Whole Life Pricing Works at the Outer Edge of the Final Expense Market

Carriers price a whole life burial insurance policy on four main things: your age when you apply, your sex, your tobacco status, and your health tier. Your premium is locked in at issue and never goes up, and your coverage never goes down.

The catch at $40,000 is qualification, not price mechanics. This amount sits above the standard simplified-issue range for most carriers, so the few that offer it apply stricter health standards — more detailed questions, prescription database checks, and medical record reviews for borderline applicants.

That means a clean approval at $25,000 does not guarantee a clean approval at $40,000. Some applicants who qualify easily at the lower amount are declined or offered a smaller face amount at $40,000, and carrier availability tightens sharply above age 75.

$40,000 Whole Life Monthly Rates by Age

The table below shows estimated monthly premiums for $40,000 of level benefit whole life coverage, non-tobacco, by age and sex.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $114 | $88 |

| 55 | $135 | $102 |

| 60 | $166 | $122 |

| 65 | $217 | $155 |

| 70 | $289 | $204 |

| 75 | $391 | $281 |

| 80 | $550 | $385 |

Sample monthly rates for level benefit at $40,000 of coverage, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

Note on availability: several carriers cap $40,000 issuance at age 75 or 80, so coverage options become severely limited above 75 and may require shopping a narrow set of carriers.

The gender gap matters most at this size. Women generally pay less than men for the same coverage because they live longer on average, often around 20 to 25 percent less, and at older ages on a $40,000 policy that difference can translate into a meaningful monthly dollar gap.

Why $40,000 Rate Variation Across Carriers Is Dramatic

Carrier shopping always matters, but at $40,000 the stakes are unusually high. Very few carriers compete in this face amount, and the ones that do use very different pricing strategies, so two applicants with identical profiles can see widely different quotes.

The dollar consequences compound over time. A premium difference of even $60 to $150 a month between the most and least competitive carrier becomes thousands of dollars over a 20-year policy life — money paid for nothing but a less competitive carrier.

At this coverage level, multi-carrier shopping is not optional. It is the single highest-leverage financial decision in the whole purchase, which is exactly where an independent broker comparing several carriers earns its keep.

Why Locking In $40,000 in Your 50s Is the Strategic Decision

Because the premium is set by your age at issue and never changes, buying earlier locks in a lower lifetime cost. A 55-year-old who qualifies in good health pays that fixed rate for life.

Waiting adds cost in two ways. Premiums rise steadily with each year of age, and final expense costs climb fastest after age 50 — for example, average monthly costs roughly quadruple between age 50 and age 80 on a $10,000 policy in one 2026 analysis, and the same steepening applies at $40,000.

The bigger risk at $40,000 is health. Because carriers apply strict standards at this size, a decline after a health change is genuinely common, so waiting risks not just a higher price but losing access to $40,000 of coverage altogether. For anyone set on this amount, earlier is dramatically more favorable.

Why $40,000 Final Expense Often Loses to Traditional Whole Life

This is the most important point in the section for healthy buyers. For most people in their 50s and early 60s in good health, simplified-issue or traditional whole life from non-final-expense carriers prices better per dollar at $40,000 than final expense does.

Final expense charges a premium for lenient, fast underwriting — value you pay for whether you use it or not. At $40,000, that convenience premium becomes a substantial monthly difference for the same applicant, and it compounds into thousands of dollars over the life of the policy.

The tradeoff is timing: traditional underwriting can take four to six weeks versus roughly 24 to 48 hours for final expense. Most healthy applicants come out ahead accepting that wait. If that describes you, compare traditional and simplified-issue whole life before assuming final expense is the right category at this face amount.

$40,000 Whole Life Rates by Age (Tobacco Users)

Tobacco users can absolutely get $40,000 of level benefit burial insurance if they qualify on health — but they pay a meaningful surcharge. This section mirrors the non-tobacco rates above.

What Tobacco Use Adds to a $40,000 Premium

Across the final expense market, tobacco users typically pay about 30 to 50 percent more than non-tobacco users for the same coverage. On a $40,000 policy, that percentage turns into a large monthly dollar gap, especially at older ages, and it compounds heavily over the life of the policy.

What counts as “tobacco” varies by carrier. Cigarettes always count, while cigars, pipes, vaping, and smokeless tobacco are treated inconsistently — though at roughly 95 percent of carriers, any tobacco or nicotine use within the look-back window is priced the same as cigarettes.

Look-back periods also vary. Most carriers want to see 12 months tobacco-free for the non-tobacco rate, though some require up to 24 months. At $40,000, getting matched to a carrier whose definition and look-back fit your history is one of the most financially consequential factors in the whole decision.

$40,000 Whole Life Tobacco Rates by Age

The table below shows estimated monthly premiums for $40,000 of level benefit whole life coverage at tobacco rates, by age and sex.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 50 | $144 | $117 |

| 55 | $182 | $145 |

| 60 | $229 | $172 |

| 65 | $310 | $218 |

| 70 | $420 | $289 |

| 75 | $571 | $391 |

| 80 | $816 | $531 |

Sample monthly rates for level benefit at $40,000 of coverage, tobacco. Rates require answering health questions, and approval is not guaranteed.

As with non-tobacco pricing, $40,000 availability narrows sharply above age 75, and the same wide carrier-to-carrier spread applies — magnified here because the tobacco surcharge sits on top of an already-large face amount.

Re-Rating to Non-Tobacco After Quitting — Major Long-Term Savings at $40,000

If you quit, you may be able to lower your rate. After 12 to 24 months tobacco-free, many carriers will reclassify an applicant to non-tobacco rates, removing the surcharge.

It helps to know how this works in practice. Re-rating is usually not automatic — you ask your current insurer to review the policy, and if you qualify as a nonsmoker your premium may drop, though in some cases buying a brand-new policy gets you a better result than re-rating the old one.

At $40,000, the stakes are large enough to shape strategy. Removing a 30 to 50 percent surcharge on a $40,000 policy saves a significant amount over the policy’s life, which is real money most generalist and TV-advertised products never mention. For a current tobacco user, it is worth weighing whether to lock in coverage now, wait until past the look-back window, or compare traditional whole life products with different tobacco rules entirely.

Carrier-Specific Tobacco Underwriting Becomes Critical at $40,000

The fine print carries real dollars here. Whether a carrier uses a 12-month or 24-month look-back can decide whether you land in the tobacco or non-tobacco class, and on a $40,000 policy that single classification difference compounds into thousands of dollars over the policy’s life.

Product type also matters. Occasional cigar users sometimes qualify for non-tobacco rates at carriers that ask only about cigarettes, which at $40,000 can save a meaningful amount each year. Vapers, by contrast, face inconsistent treatment, and smokeless tobacco is almost always treated as tobacco use.

The takeaway is the same as for pricing: at $40,000, matching your specific tobacco history to the right carrier’s rules is one of the highest-leverage moves in the entire purchase, and it is exactly the kind of carrier-by-carrier sorting an independent broker is positioned to do.

What Health-Compromised Applicants Should Do When $40,000 Isn’t Available Through Standard Underwriting

If your health keeps you from qualifying for level benefit at this size, you still have real options. This section walks through them honestly, because forcing $40,000 of burial insurance through workarounds is often not the smartest path.

Why Most Health-Compromised Applicants Will Be Declined at $40,000

At this size, moderate health issues that would be a non-event at lower amounts can lead to a decline. Final expense carriers are generally lenient — well-managed conditions like controlled high blood pressure, high cholesterol, or even well-managed Type 2 diabetes often don’t move the price, and what they really screen for are “knockout” events like a recent stroke or heart attack.

The trouble is that $40,000 raises the bar. Carriers offering this face amount apply progressively stricter standards, because their risk is concentrated in a small number of larger policies that they manage through tighter underwriting.

So applicants with controlled chronic conditions, recent diagnoses, certain medication profiles, moderate heart conditions, COPD, or insulin-dependent diabetes are routinely declined at $40,000 even when those same people would qualify cleanly at $15,000 to $25,000.

How to Combine Multiple Policies to Reach $40,000 of Coverage

If a single $40,000 level benefit policy isn’t available, you can sometimes reach the total by combining policies, a practice often called stacking or laddering. Each policy is its own contract with its own beneficiary setup, and you can hold more than one.

A practical version might pair a $25,000 level benefit policy with a $15,000 graded benefit policy from a different carrier, or split $20,000 level plus $20,000 graded across two carriers. The policies pay out independently and add up to the total face amount you want.

There are real tradeoffs to understand. You qualify twice, you manage two policies, and the combined premium is higher than a single $40,000 level policy would have cost — so this gets you to the number, but at a meaningfully higher price.

When Stepping Down to $25,000 or $30,000 Is the Smarter Decision

For many applicants, taking a smaller single policy beats chasing $40,000 through combinations. A $25,000 level benefit policy is widely available, prices efficiently, and skips the cost and complexity of juggling two contracts.

The honest math often favors the step-down. Clean single-policy underwriting at $25,000 to $30,000 frequently produces a better long-term outcome than forcing $40,000 through workarounds that stack up premium costs.

It’s worth asking whether the extra $10,000 to $15,000 of coverage is truly needed, or whether it’s overbuying dressed up as thoroughness. For a lot of buyers, the simpler, lower-cost policy is the better decision.

When Simplified-Issue Whole Life Is the Right Path Instead

If your real goal is leaving an inheritance or broader family protection at $40,000, and level benefit final expense won’t issue, simplified-issue whole life from a non-final-expense carrier is often the better route. These products generally offer higher coverage amounts than final expense, frequently up to $50,000 or more, with some carriers reaching $100,000.

The key point is leniency at higher face amounts. Simplified-issue whole life uses a health questionnaire instead of a medical exam and accepts many applicants with moderate health issues, particularly those in their 50s and 60s with controlled chronic conditions.

That means some carriers will issue $40,000 of simplified-issue whole life to someone who’d be declined for $40,000 of final expense, often at competitive premiums. Before defaulting to a multi-policy final expense workaround, it’s worth comparing simplified-issue whole life — exactly the kind of cross-product comparison an independent broker can run for you.

When the Underlying Goal Suggests a Different Product Category Entirely

Sometimes the honest answer is that final expense was never the right category. If your actual goal is generational wealth transfer, business continuity, or substantial family support — rather than covering end-of-life costs — the better fit may be traditional whole life, term life at an appropriate face amount, or a combination.

At $40,000, most buyers aren’t really shopping for funeral insurance in the traditional sense — they’re shopping for life insurance broadly. Naming the underlying goal usually clarifies the right product.

And often that exercise reveals the right category isn’t final expense at all. Getting clear on what the money is actually for is the most valuable step a health-compromised buyer at this tier can take, and it’s the kind of conversation an independent broker is built to have.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.