Home > Final Expense Insurance Cost > Final Expense Insurance in Your 60s

Final Expense Insurance in Your 60s: Rates, Coverage, and Why This Decade Matters (2026)

Your 60s are the heart of the final expense insurance market. More people buy burial insurance during this decade than any other, and for good reason: most applicants are still healthy enough to qualify for the best plan tiers, while premiums stay affordable on a fixed income. This page walks through what coverage looks like for buyers in their 60s, the monthly rates to expect across common coverage amounts, and how much coverage most people in this age range actually purchase. It also covers a truth worth understanding early: locking in a policy during your 60s usually produces the best long-term value, since waiting into your 70s typically means higher lifetime premiums and a real chance your health changes could move you out of the lowest-priced plan tier.

| Carrier | Monthly | Annual | Plan Details |

|---|

Rates shown are estimates for a level/preferred whole life final expense policy, for comparison purposes only. Actual premiums may vary based on health underwriting. Not all companies are available in all states. Contact Palmetto Mutual for exact pricing and eligibility.

What Final Expense Insurance Looks Like in Your 60s — And Why This Decade Matters Most

Your 60s are the center of gravity for burial insurance. This is the decade when most people first sit down to plan for funeral and end-of-life costs, and it is also the decade when the numbers work most in your favor. You are usually healthy enough to qualify for the best pricing, but not yet old enough for premiums to climb out of reach.

That combination is what makes this decade the most important one for the buying decision. Understanding why helps you decide whether to lock in coverage now or wait.

Why the 60s Is the Heart of the Final Expense Market

More final expense buyers purchase coverage in their 60s than in any other decade. Industry sources consistently describe seniors aged roughly 60 to 69 as the core of the market, and many agents note that buyers commonly apply in their early 60s to lock in a lower lifetime rate.

The reasons are practical, not emotional. By your 60s you are usually still healthy enough for a carrier’s best underwriting tier. Premiums are still affordable on a fixed or near-retirement income. And the conversation about end-of-life costs becomes harder to put off as retirement begins.

Because so many buyers shop in this decade, carriers compete hardest here. That competition means more product options and more aggressive pricing for 60s applicants than at any older age.

The Underwriting Environment in Your 60s

Most people in their 60s qualify cleanly for level benefit whole life — the lowest-priced plan tier, with full coverage from day one. This holds true even with common, well-managed conditions.

Controlled high blood pressure, high cholesterol managed with a statin, type 2 diabetes treated with oral medication, and mild arthritis typically still allow level benefit qualification with the right carrier. Carriers expect most applicants over 60 to have a few items in their medical file, and the product is built around that reality.

Because carriers compete for 60s applicants, underwriting tends to be more forgiving here than it becomes in the 70s and 80s. That is a genuine advantage of buying during this decade, and it is worth knowing as you weigh your options.

Why Premiums Are Still Affordable in Your 60s

Rates in your 60s sit in a sweet spot. They are higher than what you would have paid in your 50s, but well below what the same policy will cost if you wait into your 70s.

As a real-world anchor, a $10,000 Mutual of Omaha Living Promise level policy runs about $33 a month for a 60-year-old non-tobacco woman, rising to roughly $53 a month by age 70 for the same coverage. The steepest jumps in the entire rate curve come later, in the years between 75 and 80, when premiums climb sharply.

For most fixed-income retirees, the 60s is the last decade where meaningful coverage stays comfortably within budget. That is the core affordability argument for acting during this decade rather than after it.

Who Should Buy Final Expense in Their 60s vs. Wait

Not everyone in their 60s is in the same position, so the timing decision is not one-size-fits-all. The guidance below is a starting point, and the full buy-now-versus-wait math is covered later on this page.

Buyers who generally benefit from purchasing now include:

- Those with any health history that could worsen, since today’s clean qualification is not guaranteed to last

- Those whose family health history suggests conditions may be coming

- Those nearing retirement who want to lock in a fixed expense before income tightens

- Those who simply want the certainty of a premium that never changes

Buyers who can more reasonably wait include:

Those still genuinely unsure whether final expense insurance is the right product for their situation, which is worth resolving first

Very healthy applicants with strong family longevity, who can lock in slightly later without a large cost penalty

Average Final Expense Insurance Costs in Your 60s

This section fixes the decade and shows how monthly premiums move across two variables: your age within the 60s, and the coverage amount you choose. Burial insurance prices climb with each birthday, so seeing both at once helps you understand the cost of acting now versus later.

Final Expense Rates in Your 60s by Age and Coverage Amount

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 60 | $44 | $65 | $85 |

| 61 | $47 | $69 | $90 |

| 62 | $50 | $72 | $95 |

| 63 | $52 | $76 | $100 |

| 64 | $54 | $79 | $104 |

| 65 | $57 | $84 | $110 |

| 66 | $60 | $89 | $117 |

| 67 | $64 | $94 | $124 |

| 68 | $67 | $99 | $131 |

| 69 | $71 | $105 | $139 |

Sample monthly rates for male applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 60 | $33 | $48 | $63 |

| 61 | $35 | $51 | $66 |

| 62 | $37 | $53 | $69 |

| 63 | $38 | $55 | $73 |

| 64 | $40 | $58 | $76 |

| 65 | $42 | $60 | $79 |

| 66 | $44 | $64 | $84 |

| 67 | $46 | $68 | $89 |

| 68 | $49 | $71 | $94 |

| 69 | $51 | $75 | $99 |

Sample monthly rates for female applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

These figures are planning benchmarks, not quotes. Because carriers price the same applicant differently, the only way to know your exact rate is a multi-carrier comparison for your specific profile.

How Premiums Change Across Your 60s

Premiums rise steadily through the decade, and the curve steepens toward the late 60s. Using the representative rates above, a $15,000 policy for a non-tobacco woman runs about $48 a month at 60 and roughly $68 at 68 for the same coverage.

The early-60s increases are gentle, often just a few dollars a year. The late-60s increases are larger, because each year closer to 70 carries more actuarial risk for the carrier.

The practical takeaway is that the gap between buying at 62 and buying at 68 is meaningful — not catastrophic, but large enough to weigh seriously when deciding on timing. Locking in earlier in the decade locks in the lower number for life.

How Tobacco Use Changes Costs in Your 60s

Tobacco use raises your premium, because carriers price smokers as a higher mortality risk from day one. At the coverage amounts common in your 60s, that surcharge typically adds somewhere around $20 to $60 or more per month compared with a non-tobacco rate for the same policy.

Tobacco look-back rules matter more in this decade than at older ages, because many buyers in their 60s are recent quitters. Most carriers ask whether you have used tobacco in the past 12 months, but some look back two to three years.

That difference can decide everything. A buyer who has been tobacco-free for, say, 14 months qualifies as non-tobacco at a carrier with a 12-month look-back, but would still be classed as a tobacco user at a carrier looking back 24 months. For burial insurance shoppers who recently quit, getting matched to a carrier with the shorter look-back can move them into the lower rate tier.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 60 | $61 | $90 | $119 |

| 61 | $65 | $96 | $126 |

| 62 | $67 | $100 | $132 |

| 63 | $70 | $103 | $137 |

| 64 | $73 | $108 | $143 |

| 65 | $77 | $113 | $150 |

| 66 | $81 | $120 | $159 |

| 67 | $85 | $126 | $167 |

| 68 | $90 | $134 | $177 |

| 69 | $95 | $141 | $187 |

Sample monthly rates for male applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 60 | $46 | $68 | $89 |

| 61 | $48 | $71 | $94 |

| 62 | $51 | $75 | $98 |

| 63 | $53 | $78 | $103 |

| 64 | $56 | $82 | $108 |

| 65 | $58 | $86 | $113 |

| 66 | $61 | $90 | $119 |

| 67 | $64 | $95 | $125 |

| 68 | $67 | $98 | $130 |

| 69 | $71 | $105 | $139 |

Sample monthly rates for female applicants, level benefit, tobacco. Rates require answering health questions, and approval is not guaranteed.

How Health Conditions Affect Costs in Your 60s

The most common conditions among 60s applicants usually do not move you out of the best pricing tier. Controlled hypertension, type 2 diabetes managed with oral medication, cholesterol managed with a statin, and mild, stable heart conditions typically still allow level benefit qualification with the right carrier.

Less common but more serious conditions can push an applicant toward graded benefit, which limits the payout during the first two years. These include a recent cardiac event, insulin-dependent diabetes with complications, and a COPD diagnosis.

Because each carrier weighs these conditions differently, the same health profile can earn level benefit at one company and graded at another. That variation is exactly why comparing carriers matters for anyone with a health history.

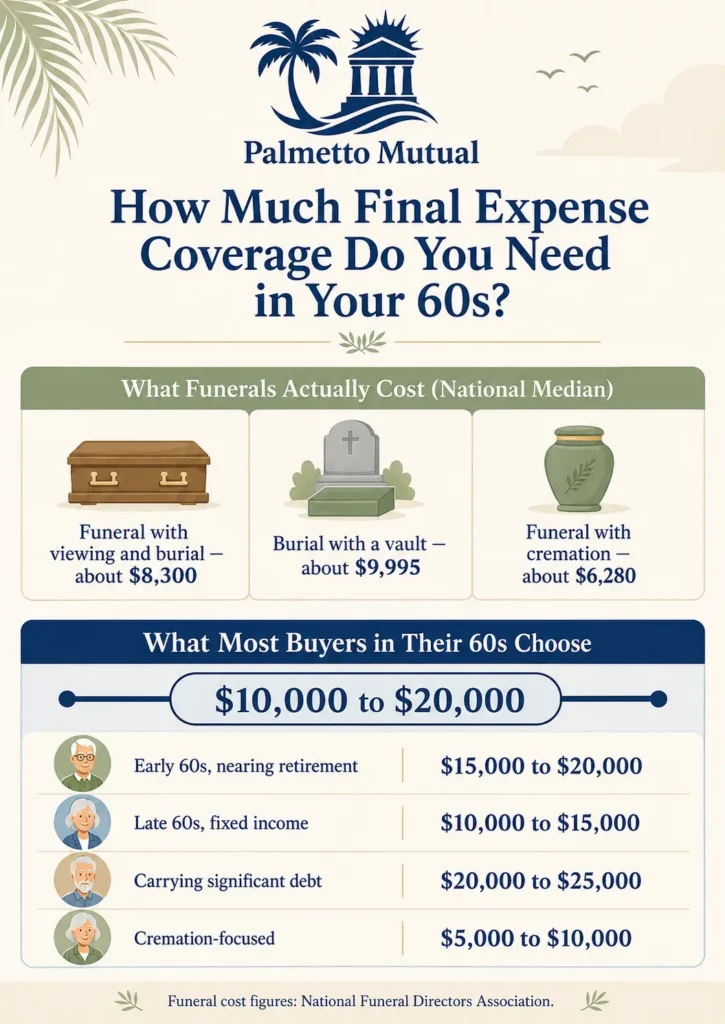

How Much Coverage Most People in Their 60s Actually Buy

Choosing a coverage amount is really about matching the death benefit to the bills you want it to cover. For most burial insurance buyers in their 60s, that lands in a fairly predictable range, with sensible reasons to go higher or lower.

The Most Common Coverage Amounts for 60s Buyers

The majority of buyers in their 60s purchase between $10,000 and $20,000 of coverage. Within that band, the choice tends to track age and goals.

The $10,000 to $15,000 range skews toward early-60s buyers and those mainly covering funeral costs. The $15,000 to $20,000 range skews toward late-60s buyers and those who want funeral coverage plus a financial cushion for family.

Amounts of $25,000 and up are less common. They generally fit buyers with significant outstanding debt or a specific legacy goal, rather than the typical funeral-only buyer.

Why Most 60s Buyers Land Between $10K and $20K

The range is anchored to what funerals actually cost. The National Funeral Directors Association reports a national median of about $8,300 for a funeral with viewing and burial, and about $6,280 for a funeral with cremation; adding a vault pushes the burial figure closer to $9,995.

That math makes $10,000 the natural entry point and $15,000 to $20,000 the comfortable, comprehensive range. These amounts cover the funeral with room left for a headstone, final medical bills, or small debts, while premiums stay manageable on a typical 60s budget.

Higher amounts ($25,000 and up) usually require either real outstanding obligations or a specific legacy intent to justify the added premium. Lower amounts (around $5,000) generally only suit cremation-focused buyers in this decade.

When 60s Buyers Should Consider More Coverage

Some situations call for stepping above the typical range. Funeral insurance should match your real obligations, and for some buyers those obligations are larger than the national median suggests.

Consider more coverage if you:

- Live in a higher-cost region where funerals commonly run $13,000 to $16,000

- Carry significant outstanding medical bills, credit card balances, or other debts

- Have adult children who would otherwise help pay for the funeral

- Want one policy to cover both an eventual funeral and some ongoing support for a surviving spouse

If any of these fit, the $20,000 and $25,000 amounts are worth a closer look.

When 60s Buyers Should Consider Less Coverage

Just as often, buyers in their 60s need less than they assume. Buying more coverage than your situation requires only adds premium you do not need.

Consider less coverage if you:

- Plan a direct cremation rather than a traditional burial

- Already have savings specifically earmarked for final expenses

- Are single without dependents or close family who would need a financial buffer

- Are on a tight fixed income where the difference between $10,000 and $20,000 creates real budget strain

For buyers who realize they need less, the smaller amounts are a better fit.

Coverage Amount Recommendations by 60s Profile

These profiles are general starting points, not firm rules. Your own number depends on your funeral plans, debts, and budget.

The early-60s buyer working toward retirement typically lands around $15,000 to $20,000, balancing funeral costs with a family cushion.

The late-60s fixed-income retiree typically lands around $10,000 to $15,000, focused on covering the funeral comfortably without straining the monthly budget.

The 60s buyer carrying significant debt typically needs $20,000 to $25,000 so the benefit covers both the funeral and the outstanding balances.

The cremation-focused 60s buyer typically lands around $5,000 to $10,000, since cremation costs are well below traditional burial.

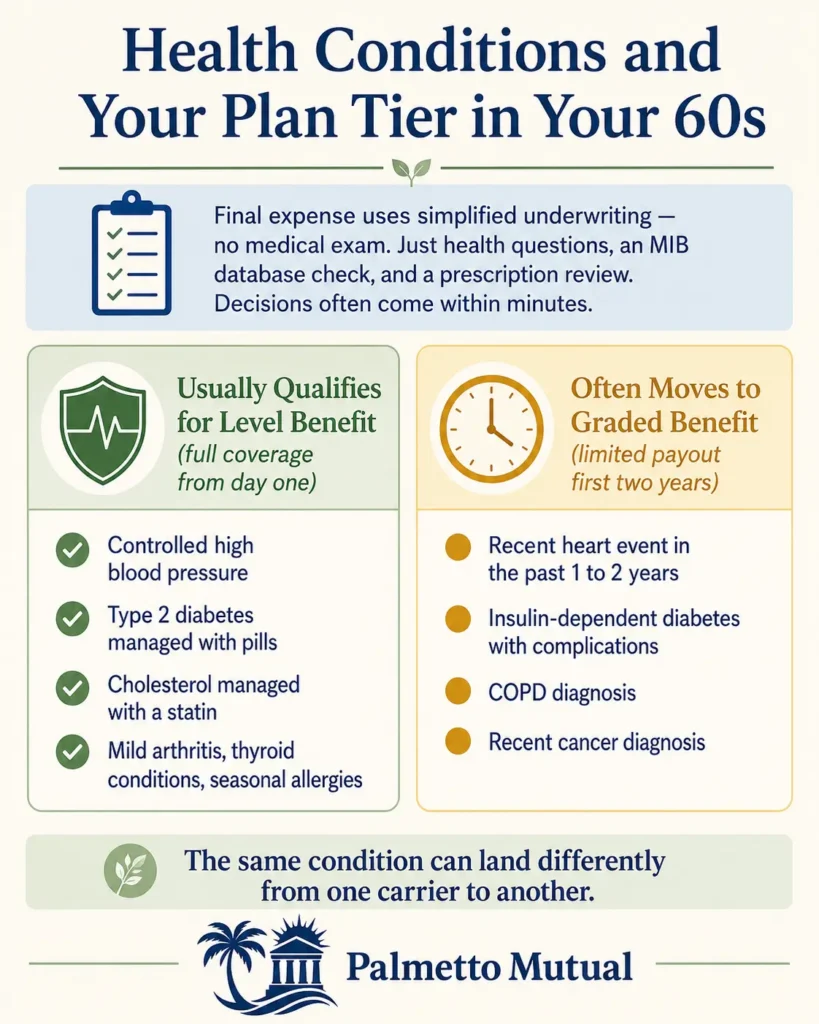

How Final Expense Underwriting Works in Your 60s

Final expense insurance uses simplified underwriting, which means no medical exam and no blood draw — just a short set of health questions and some database checks. Knowing what carriers actually look at helps you understand why you might qualify for one plan tier over another.

What Carriers Actually Evaluate for 60s Applicants

Carriers base their decision on three things: your answers to the application’s health questions, a check of the Medical Information Bureau (MIB) database, and a review of your prescription history through an Rx database. Occasionally a borderline application gets a closer look, but full medical record reviews are not the norm.

The prescription and MIB checks mainly exist to confirm that your answers line up with your records. If your medications match what you reported, the application usually moves straight to approval.

Most applications in this decade are decided quickly — often within minutes, and at most within a few business days. There is no long waiting period for a decision on simplified-issue coverage.

Common 60s Health Conditions and How They Affect Qualification

Most conditions common at this age do not block you from level benefit, the lowest-priced tier. The table below summarizes how typical conditions tend to be treated, with the right carrier.

| Condition | Typical effect on qualification |

|---|---|

| Controlled high blood pressure | Usually allows level benefit |

| Type 2 diabetes on oral medication | Usually allows level benefit |

| Cholesterol managed with a statin | Usually allows level benefit |

| Mild arthritis, hypothyroidism, seasonal allergies | Usually allows level benefit |

| Recent cardiac event (within 1–2 years) | Often pushes toward graded benefit |

| Insulin-dependent diabetes with complications | Usually allows level benefit |

| COPD diagnosis | Usually allows level benefit |

| Recent cancer diagnosis | Often pushes toward graded benefit |

These are general patterns, not guarantees. The right carrier match matters, which is why deeper, condition-by-condition guidance is worth reviewing.

Why Some 60s Applicants Get Pushed to Graded Benefit

Graded benefit limits the payout during the first one to two years, usually returning premiums paid plus interest if death occurs from natural causes in that window, then paying the full benefit afterward. Several things commonly trigger a graded offer even for an otherwise healthy 60s applicant.

Carriers apply stricter standards as a health picture gets more complex. Someone with several controlled conditions might earn level benefit at one carrier and graded at another.

Timing matters too. A diagnosis within the past 12 to 24 months often triggers graded benefit even when the condition is well controlled, and a medication change in the past 6 to 12 months can flag in the Rx check and affect the offer. For borderline applicants, these carrier-by-carrier differences are significant.

How to Improve Your Plan Tier Qualification in Your 60s

You have more influence over your outcome than many buyers realize. A few factors consistently improve the odds of qualifying for level benefit.

- Time since diagnosis: Many carriers treat a condition diagnosed two or more years ago more favorably than a recent one

- Medication stability: Being stable on the same regimen for 12 or more months generally helps

- Documented follow-up care: Routine, documented care for a chronic condition often qualifies better than gaps in care

- Tobacco-free time: Completing a full 12-month tobacco-free period before applying can move you from tobacco to non-tobacco rates, a meaningful difference

None of these are tricks; they simply give the carrier cleaner data to price you accurately.

When to Apply With a Multi-Carrier Agent vs. Direct

Going directly to a single carrier works fine if you are very healthy with no health concerns — you get that one company’s pricing for your profile. The limitation is that you only see one company’s answer.

A multi-carrier agent becomes more valuable the moment any health complexity enters the picture, because underwriting niches vary so much between carriers. The same applicant can qualify for level at one company and graded at another, so being matched to the right carrier affects both your rate and your plan tier.

Should You Lock In Final Expense in Your 60s — Or Wait?

The biggest timing question for burial insurance is whether to buy now or put it off. Because your rate is locked in for life the day you buy, the decision has real financial weight. This section lays out the math and the trade-offs honestly, including the cases where waiting is the smarter move.

The Real Cost of Waiting From Your 60s Into Your 70s

Waiting raises your premium in two ways: the monthly rate climbs with each birthday, and you pay that higher rate for the entire life of the policy. The rate never resets, so the number you lock in is the number you keep.

Using representative Mutual of Omaha Living Promise pricing, a $15,000 level policy for a man runs in the neighborhood of $60 to $70 a month at 62, but closer to $100 to $130 a month if he waits until 72. The steepest part of the curve comes later still, in the years between 75 and 80.

Stretched over a 20-year policy life, a monthly gap of roughly $40 to $60 adds up to somewhere around $10,000 to $14,000 or more in extra lifetime premiums for the same death benefit. The exact figure depends on your profile, but the direction is consistent: locking in earlier in the decade costs less over the life of the policy.

Why Health Changes During Your 60s Can Disqualify You From Level Benefit

The cost-of-waiting math assumes your health stays steady enough to keep qualifying for level benefit. That assumption does not always hold.

Many people qualify cleanly for level benefit in their early 60s but develop a condition in their late 60s or early 70s that moves them to graded benefit if they wait. A new diagnosis — cancer, a recent cardiac event, a stroke — can take level benefit off the table entirely, while worsening control of an existing condition such as diabetes or COPD commonly triggers a graded offer.

Put plainly: waiting is a bet that your health holds steady enough to keep your level qualification. That bet sometimes pays off, but it often does not, and the downside is both a higher rate and a waiting period on the benefit.

When Locking In at 62 Beats Locking In at 68

For most buyers, buying earlier in the decade comes out ahead. The advantages stack on top of each other.

The premium is meaningfully lower — often $20 to $40 a month less at 62 than at 68 for the same policy. The underwriting environment is also most favorable early in the decade, with more carriers competing and fewer health conditions accumulated.

There is a longer runway, too. A policy bought at 62 has more years to build cash value than the same policy bought at 68. Taken together, the early-decade buyer typically pays less over the life of the policy for identical coverage.

When Waiting Until Late 60s Makes Sense

Waiting is sometimes the right call, and it is worth being honest about that rather than pushing everyone to buy immediately. A few situations genuinely favor waiting.

- Very healthy applicants with strong family longevity, who have not yet retired and would rather defer the premium expense for now

- Buyers still unsure whether final expense insurance is even the right product category for them, which is worth resolving first

- Buyers anticipating a major financial change — downsizing, a retirement transition — who want their budget to settle before committing to a new monthly expense

If one of these describes you, a short delay can be reasonable, as long as you go in understanding the rate and underwriting risk that comes with it.

Whether Final Expense Is Even the Right Product in Your 60s

Before committing, it is worth asking whether final expense is the best fit at all. For some buyers — especially healthy people in their early 60s — it may not be.

Final expense pricing carries a built-in premium for its lenient, no-exam underwriting. A healthy early-60s buyer who could pass medical underwriting might get more coverage per dollar from a traditional whole life or term policy from a standard carrier, since they are paying for flexibility they do not strictly need.

The honest recommendation is not to commit to funeral insurance in your 60s without first checking whether traditional life insurance would serve your goals better. For many people final expense is still the right answer — but it is worth confirming, not assuming.

Best Carrier Considerations for Buyers in Your 60s

Which company you apply to can change your rate and your plan tier more than almost any other decision. For burial insurance buyers in their 60s, carrier choice matters more than at any other age, and understanding why helps you shop wisely. The deepest carrier-by-carrier guidance lives on a dedicated page, but the decade-specific considerations are covered here.

Why Carrier Selection Matters Most in Your 60s

Carriers compete hardest for 60s applicants because this is the core of the market. That competition produces wide price spreads for the same buyer.

It is common to see prices for identical coverage range widely between carriers — one company asking $60 a month while another asks $110 for the same policy. Because that spread is widest where competition is most intense, comparing carriers in your 60s can produce some of the most meaningful savings in the entire final expense market.

The takeaway is simple: the same applicant, same coverage, can pay very different amounts depending on which carrier they land with. Shopping is where the money is.

What Makes a Carrier “Good” for 60s Buyers

A strong carrier for a 60s buyer balances price, underwriting fit, and reliability. No single factor tells the whole story.

The qualities worth weighing include:

- Competitive 60s rates, since some carriers price aggressively for this decade specifically

- Lenient underwriting on common 60s conditions like controlled hypertension, type 2 diabetes, and managed cholesterol

- Reasonable tobacco look-back periods, where a 12-month look-back helps recent quitters qualify at non-tobacco rates

- Strong financial ratings, such as an A.M. Best rating of A or higher, which speaks to long-term claim reliability

- Useful rider options, especially an accelerated death benefit that lets you access part of the benefit early if you are diagnosed with a terminal illness

How Carrier Underwriting Niches Affect 60s Applicants

Carriers do not underwrite alike. Each has its own niches, and matching your profile to the right one matters for both rate and plan tier.

Some carriers underwrite diabetic applicants more favorably than others. Some specialize in tobacco users, some price cardiac history more leniently, and some offer the best rates for the youngest 60s applicants but become uncompetitive at the older end of the decade.

This is why one carrier is rarely right for everyone. The best fit for a healthy 62-year-old non-tobacco applicant is often not the best fit for a 68-year-old with type 2 diabetes, and getting matched correctly affects what you pay and which tier you land in.

Why Direct-to-Carrier Quotes Often Aren’t the Best Deal in Your 60s

Going straight to one carrier gives you exactly one company’s price for your profile. That is fine if you happen to pick the carrier that views your health most favorably — but you have no way to know that from a single quote.

An independent agent who works with several carriers can compare the pricing of five to ten companies for your exact profile and surface the most favorable one. Given the wide rate spread at 60s ages, the gap between a single direct quote and the best multi-carrier quote commonly runs $20 to $50 or more a month for the same coverage and the same applicant.

That is the practical case for working with a multi-carrier broker rather than buying blind. A short phone consultation is usually the most accurate way to get real, side-by-side quotes for your specific age, health, and coverage goals — not a sales step, just the most direct path to comparing your actual options.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.