Home > Final Expense Insurance > Biggest Mistakes

5 Biggest Mistakes People Make Buying Burial Insurance

Buying burial insurance should be a simple decision, but a few common mistakes can quietly make it cost more — or leave your family with less coverage than they counted on. Most of these mistakes happen for understandable reasons, and nearly all of them are easy to avoid once you know what to watch for. This guide walks through the five biggest mistakes people make when buying final expense insurance, and explains how each one happens.

Settling for Guaranteed Issue When You’d Qualify for Level Coverage

The “no health questions” policy feels like the easy choice. There is nothing to disclose, nothing to get wrong, and approval is automatic. But for most people, it is the most expensive way to buy burial insurance — and it comes with a catch that the easy front door hides.

A guaranteed issue policy accepts everyone in the age range with no health questions at all. In exchange, it costs more per dollar of coverage than a level policy, and it pays out more slowly at the start.

Here is the part that trips people up. Guaranteed issue is built for people who can’t qualify any other way — serious or recent health conditions that close the door on other policies. If you are reasonably healthy, you are very likely paying for a door you didn’t need to use.

Many common conditions still qualify for immediate level coverage when they are controlled. Examples include high blood pressure, high cholesterol, controlled type-2 diabetes, and sleep apnea managed on a CPAP. A level policy means full coverage from day one and a lower monthly premium for the same face amount.

The size of the gap depends on your age, your health, and the carrier. But the direction is always the same: if you qualify for level coverage, it beats guaranteed issue on both price and speed of payout — even when a guaranteed issue ad shows a low “starting at” number. For the same coverage at the same age, one carrier might price a healthy applicant near the bottom of the market while another sits well above it, which is why the comparison matters.

This is why the order of operations matters. Figure out which policy type you actually qualify for first, then compare prices within that type. Leading with “no health questions” skips that step and often locks in the priciest version of funeral insurance available.

One more thing worth clearing up, because it causes real confusion. “No medical exam” and “no health questions” are not the same. Most level policies skip the exam but still ask a short health questionnaire — and answering those questions honestly is what unlocks the cheaper, immediate coverage. Walking past the questions entirely is what lands you in guaranteed issue by default.

Buying From the First Company You Find

Final expense insurance is one of the most heavily advertised products aimed at seniors. The TV spot with the friendly host, the official-looking envelope in the mail, the single agent who only ever mentions one company — they all share a quiet cost. Buying from the first source you find usually means you never saw what else was on the table.

Start with the advertising. A lot of “as seen on TV” and direct-mail final expense offers are guaranteed issue policies — the no-questions kind with a waiting period built in. Healthy people often buy these by mail without realizing a cheaper, immediate policy was available to them. The mail piece doesn’t ask health questions because it isn’t trying to find your best rate. It’s selling one product to everyone.

The single-company agent has a different version of the same limit. A captive agent represents exactly one insurance company and can only offer that company’s products. If that one carrier isn’t the best fit for your age, your health, or your budget, the captive agent can’t send you somewhere better — even when somewhere better exists.

The cost of skipping the comparison is not small. For the same person, the same age, and the same coverage, prices swing meaningfully from carrier to carrier. One example shows a 60-year-old nonsmoker seeing roughly $50 a month at one carrier and around $80 at another for the same $10,000 of coverage. Same buyer, same coverage — a difference you only see if someone is actually checking more than one company.

There’s a detail here that surprises people. Many strong, highly rated final expense carriers don’t advertise on TV at all. They spend their money on competitive pricing instead of commercials, so the company that would have served you best may be one you’ve simply never heard of.

That is the whole case for comparing across carriers before you buy. An independent broker isn’t more expensive for doing it — the commission is already baked into the premium either way — but they can place you with the carrier that fits, instead of the one that happened to find you first.

Misunderstanding the Waiting Period

The single most painful surprise in burial insurance happens at claim time — and it lands on the family, not the buyer. Someone passes away a year into the policy, the family files the claim expecting the full amount, and the check comes back far smaller. The coverage was real. The misunderstanding was about when the full benefit kicks in.

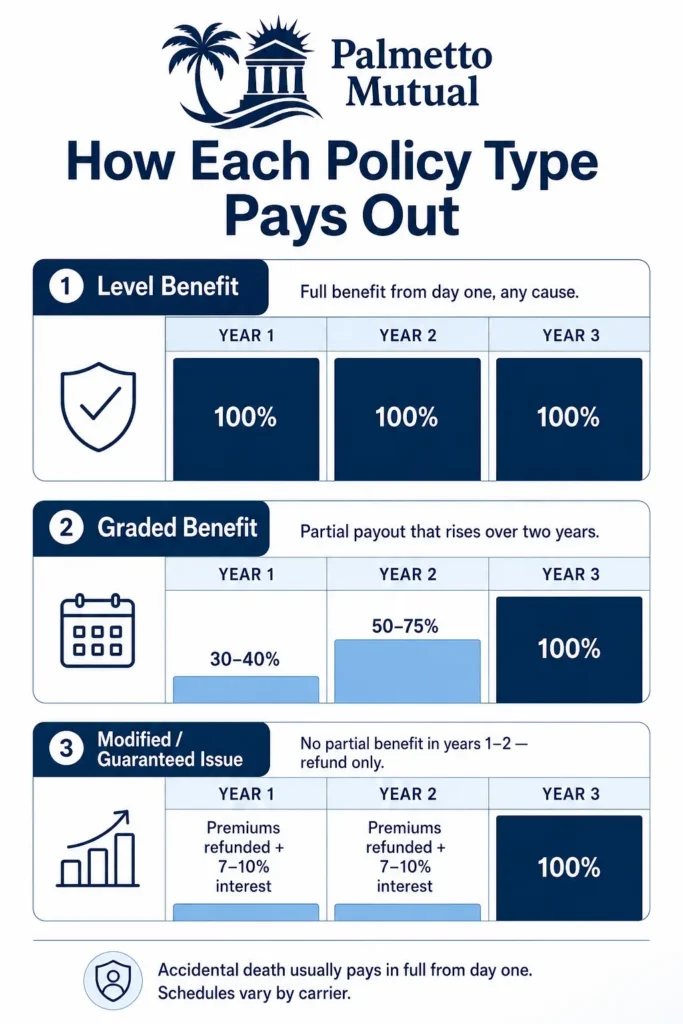

Not every burial insurance policy pays the full amount from day one. Whether it does depends on which of three structures the policy uses.

A level benefit policy pays 100% of the death benefit from the first day, for any cause of death. This is what most people assume they’re buying — and it’s what you get when you qualify on health. The other two structures work very differently in those early years.

A graded benefit policy phases the payout in over about two years. The exact schedule varies by carrier, but a common pattern pays roughly 30–40% of the face amount for a death in the first year, around 50–75% in the second year, and the full amount from year three onward.

A modified or guaranteed issue policy works differently again. During the first two years it pays no partial benefit at all — instead it refunds the premiums you paid, plus interest, commonly around 7–10%. The full death benefit only becomes available after that window closes.

Here’s the math that makes this real. Picture a $10,000 modified policy and a death 18 months in. Instead of $10,000, the family might receive only the premiums paid back plus a small interest bump — possibly a few hundred dollars against a funeral bill that can run $8,000 or more. That gap is exactly what families don’t see coming.

There is one consistent bright spot. Across these structures, accidental death usually pays the full benefit from day one, even during the waiting period. The reduced early payout applies to natural-cause deaths, which are the more common claim for this age group.

This is also why reading the benefit table matters. The fine print will say something like “return of premium in years one and two” for a modified or guaranteed policy, versus “full face amount day one” for a level policy. Confirming that line before you buy is what prevents the claim-time shock entirely.

One last clarification, because the terms get mixed up. The waiting period is not the same as the contestability period. The waiting period limits the early payout by design; the contestability period is a separate two-year fraud-check window that exists on nearly every policy, including level ones — and that’s the subject of the next mistake.

Getting the Health Questions Wrong

Most level and simplified burial insurance policies ask a short list of health questions instead of requiring a medical exam. Those answers do two things: they decide which tier and price you qualify for, and they become part of the contract. Getting them wrong — even by accident — can quietly set up a problem the family discovers only at claim time.

There are two ways this goes wrong, and they are very different.

The common version is innocent. People simply don’t have their own health details straight — the exact name of a condition, every medication they take, or the dosage. Application questions cover health history, medications, and tobacco use in detail, and an inaccurate answer, even an unintentional one, can place you in the wrong tier or create grounds for a later dispute. This isn’t dishonesty; it’s a memory and paperwork problem.

The rarer version is intentional — leaving off a known condition or understating tobacco use to get a better rate or an approval. Understating tobacco use is one of the most common application errors insurers see, and either kind of misstatement carries the same risk at claim time.

To see why accuracy matters so much, you have to understand what happens after a death. If the insured dies within the first two years, the insurer can open a closer review of the original application — this window is called the contestability period. During it, the insurer can compare what was written on the application against the actual record.

Insurers check those answers against real data: medical records, prescription history, and the MIB database that tracks insurance application history. If a meaningful answer doesn’t match — something that would have changed the price or the decision to insure — that’s called a material misrepresentation, and it can lead to a reduced payout or a denied claim.

The hard part for families is that this can happen even when the mistake was honest. During the contestability window, an unintentional error can still be grounds for a denial — intent isn’t always required. After two years, the policy generally becomes incontestable, and insurers usually must prove intentional fraud to challenge a claim.

A couple of fair caveats keep this in perspective. Contested denials are not the norm — most claims are paid, and an answer only counts against the claim if it was truly material to the risk. Minor or irrelevant errors generally don’t qualify.

The takeaway isn’t fear — it’s care. The goal is simply to answer every question accurately and completely. Bring your medication list and condition history to the application, and if you’re unsure how to answer something, ask rather than guess. Because most final expense applications are completed with an agent over the phone, having someone walk through the questions with you is one of the best safeguards against an innocent mistake.

Sizing the Benefit Wrong

Picking the coverage amount sounds like the easy part. But getting it wrong in either direction costs the family something — too much, and the premium becomes a burden you carry for years; too little, and the benefit doesn’t stretch far enough when the funeral bill arrives. The goal is to match the benefit to the real need, not to a round number or a sales target.

Start with what the money actually has to cover, because that’s the anchor for the whole decision. A funeral with viewing and burial runs a median around $8,300, climbing to roughly $9,995 once a vault is added; a funeral with cremation and viewing runs closer to $6,280. Cemetery plots, headstones, and other extras can push the total higher, and burial life insurance is often also used for leftover medical bills or small debts.

Buying More Than You Need

The over-buy side is less common, but it has a real cost. A larger face amount means a higher monthly premium, and you pay that higher premium every month for as long as you hold the policy — potentially for decades. If the funeral plan is a simple cremation, a benefit sized for an elaborate burial is money going out the door each month for coverage the family won’t need.

There’s a more serious version of over-buying, and it’s the affordability trap. Final expense premiums are fixed, but if you size the coverage so high that the premium strains a fixed income, the risk is that the policy eventually becomes unaffordable.

Here’s why that matters so much with this product. If the policy lapses for non-payment, the coverage ends — it won’t pay out later when the family needs it. In the early years there’s usually little or no cash value to fall back on, so a lapse can mean losing much of what was paid in. An oversized premium you can’t sustain is worse than a right-sized one you can keep for life.

Buying Less Than You Need

The more common mistake runs the other way: choosing a benefit that’s too small for the real cost. It’s an understandable instinct — a lower coverage amount means a lower premium, so the smaller policy looks easier on the budget today.

The problem shows up at claim time. If the benefit is $5,000 but the funeral the family chooses runs $9,000 or more, the family has to cover the gap out of pocket during a hard week. The policy helped, but it didn’t do the job it was bought to do.

This is also why a fixed benefit deserves a second look over time. Funeral costs keep rising, but a death benefit you locked in years ago does not. A $10,000 policy that comfortably covered a funeral when you bought it may fall a little short a decade or two later — worth keeping in mind when you choose the starting amount.

The fix for both directions is the same: size the benefit against the actual funeral plan and the real local cost, not against a default number or whatever an ad suggests. A right-sized policy covers the need, keeps the premium sustainable for life, and avoids both traps.

How to Avoid Every One of These

You don’t need five separate strategies to dodge these five mistakes. Almost all of them trace back to the same root — buying too fast, from too few options, without matching the policy to your actual health and needs. Fix that, and most of these problems never start.

Here’s the short version of what to do instead, mistake by mistake:

- Don’t default to guaranteed issue. Answer the health questions and find out what you actually qualify for first — if you’re reasonably healthy, level coverage is cheaper and pays in full from day one.

- Don’t buy from the first source. The TV spot, the mail piece, and the single-company agent all show you one option; the same person and coverage can be priced very differently across carriers, so compare before you commit.

- Don’t assume day-one full coverage. Read the benefit table and know which structure you’re buying — level pays in full immediately, while graded and modified policies limit the early payout for the first couple of years.

- Don’t guess on the health questions. Bring your medication list and condition history, answer accurately and completely, and ask when you’re unsure — accuracy protects the claim.

- Don’t size by a round number. Match the benefit to your real funeral plan and local cost, high enough to cover it but affordable enough to keep for life.

Notice that nearly every “do instead” above points to one move: compare honestly across carriers before you apply, and get placed in the right policy type for your health. That single step prevents the guaranteed-issue default, the first-source trap, the wrong policy structure, and the wrong size all at once.

This is exactly where an independent broker earns its keep. An independent agent represents many carriers and works for you, not one company — so they can match your health profile to the carrier most likely to approve you for the best-fit policy, instead of selling you the one product they happen to carry. And because most final expense applications are completed over the phone with an agent, you have someone walking you through the health questions in real time, which heads off the innocent-mistake problem too.

The practical next step is simple: rather than respond to the first ad you see, get a side-by-side comparison across carriers for your age, health, and coverage need — most often by talking it through with an independent agent over the phone, who can quote several companies in one conversation.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.