Home > Final Expense

What Is Final Expense Insurance? (The Complete Guide For 2026)

Final expense insurance is a small whole life insurance policy that helps cover the costs that come at the end of life, such as a funeral, burial or cremation, and any unpaid bills left behind. This guide walks through what the product is, how it works, and who it’s designed for. Along the way, you’ll see how it compares to other kinds of life insurance, what the main policy types are, and why the same person can get very different rates from different companies.

What Is Final Expense Insurance and How Does It Work?

Final expense insurance is a small whole life insurance policy designed to cover the costs at the end of life. Most policies are sized between $5,000 and $35,000 — enough to handle a funeral and a few leftover bills, but not meant to replace a paycheck.

The key thing to understand is that this is not a separate kind of insurance. It is regular whole life insurance, just designed and priced for a specific job and a specific buyer.

Because it is whole life, the policy works the same way whole life always has. Four features matter most:

| Feature | What it means for you |

|---|---|

| Permanent coverage | The policy never expires as long as you pay the premium. It is there at age 70, 85, or 100. |

| Level premium | The price is locked when you buy. It never goes up as you age. |

| Cash value | The policy slowly builds a small savings amount over the years that you can borrow against if needed. |

| Tax-free death benefit | When you pass away, your beneficiary receives the payout, and the IRS does not count it as taxable income. |

A quick note on cash value: it grows slowly, and there is almost none in the first couple of years. Cash value is a nice extra, but it is not the reason to buy the policy. The real reason is permanent coverage at a price that never changes.

The death benefit is the heart of the product. When you die, the insurance company pays the money directly to the person you named — your spouse, a child, or anyone you choose. Under IRS rules, a standard life insurance payout is generally received income-tax-free.

Here is the simple version of how it all works. You answer a few health questions and pick a coverage amount. You pay the same premium every month for life. When you pass away, your family gets a tax-free check they can use right away.

Final Expense vs. Burial Insurance vs. Funeral Insurance

If you have shopped around at all, you have probably seen three different names: final expense insurance, burial insurance, and funeral insurance. It is easy to think these are three separate products. In almost every case, they are not — they describe the very same whole life policy.

So why all the different names? It comes down to marketing. Different companies and agents found that different words connect better with different people.

| Name you might see | Why is it used |

|---|---|

| Final expense insurance | Sounds broader and less blunt. Points to all end-of-life costs, not just the funeral. |

| Burial insurance | Plain and direct. Speaks to the cost many people worry about first. |

| Funeral life insurance | Names the single expense most families picture right away. |

The good news is that you do not have to worry about which term to search for. Whether a website says burial insurance or funeral insurance, the underlying policy is the same small whole life plan, with the same fixed premium and the same payout to your family.

There is one exception worth noting, because it is the only place where the names truly part ways. A product called “pre-need” insurance is sold directly by some funeral homes, and with that one, the money goes straight to the funeral home instead of to your family.

The difference is who gets the check. Under the standard policies we discuss on this page, your beneficiary receives the cash and decides how to spend it. With a pre-need plan, the funeral home is paid, and the money can only cover those home’s services.

For most people shopping for coverage, the takeaway is simple. Final expense, burial, and funeral insurance are three labels for one product, and the right way to compare offers is to look past the name and check the coverage amount, the premium, and the policy type.

How Final Expense Differs from Term Life Insurance

Final expense insurance and term life insurance are built very differently, and that difference matters most for older buyers. Term insurance is temporary by design. Whole life, which is what burial insurance is, is built to last. The sections below explain why that gap grows wider with age.

How Term Life Insurance Works for Older Buyers

Term life insurance covers you for a set number of years and then ends. Most term coverage also stops being available once you reach about age 80, and after 81, it is very hard to find at all.

The longer term lengths decrease as you age. If you apply in your 60s, a 30-year term is off the table, and many companies will not offer a 20-year term either. By age 70, a 10-year term is often the longest you can get.

Term also tends to work against older buyers in one of two ways, depending on the product:

| Term structure | What happens to you |

|---|---|

| Renewable term | The premium is low at first, then jumps each time you renew, because the new price is based on your older age. Renewals can come every few years, and the cost can climb fast. |

| Decreasing term | The premium stays level, but the death benefit shrinks over time. The longer you live, the less your family receives. |

The result is the same problem from two directions. Term insurance gets harder to qualify for, more expensive, or less valuable at exactly the age when covering final costs matters most.

How Final Expense Compares

Final expense works the opposite way. The rate is locked at your age when you buy, and it never goes up. The death benefit never shrinks, and the policy never expires as long as you pay the premium.

That is the whole point of the product. It is built to solve the exact problems that make term insurance a poor fit for seniors. You are not racing against a clock or a rising bill. You buy it once, and it stays the same for the rest of your life.

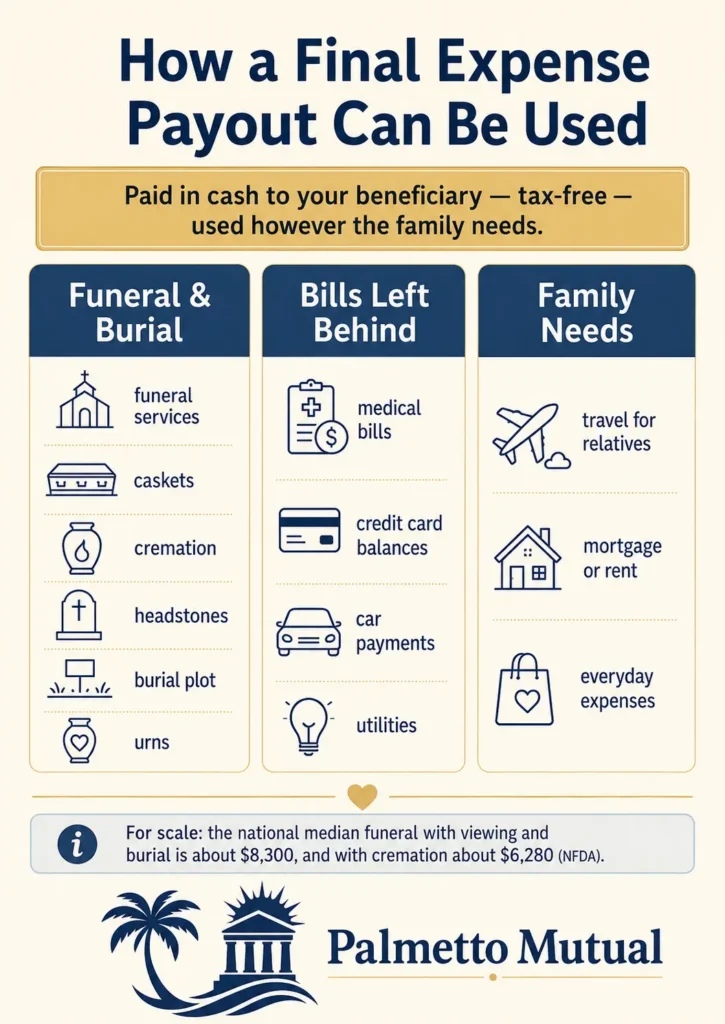

What the Payout Can Be Used For

When you pass away, the money from a funeral life insurance policy is paid in cash, directly to the person you named as your beneficiary. It does not go to a funeral home as a voucher or a credit. Your beneficiary receives a check and decides how to spend it.

That freedom is one of the most useful features of the product. The policy is meant to cover end-of-life costs, but there are no rules requiring the funds to be used only for a funeral.

Here is how families most often put the payout to work:

| Type of cost | Common examples |

|---|---|

| Funeral and burial | Funeral services, caskets, cremation, headstones, burial plot, urns |

| Bills left behind | Outstanding medical bills, credit card balances, car payments, utilities |

| Family needs | Travel for relatives attending the service, a mortgage or rent payment, and everyday expenses |

These costs add up quickly. The national median for a funeral with viewing and burial was about $8,300, and for cremation, about $6,280; those figures do not even include a cemetery plot or grave marker. A casket alone often runs around $2,000.

There is also a tax question worth answering here, because it comes up often. A standard life insurance death benefit is generally received income-tax-free by the beneficiary, so your family keeps the full amount. The payout is theirs to use the moment it’s needed.

Why Final Expense Insurance Is Ideal for Its Audience

Final expense insurance is built for a specific kind of buyer, and it fits that buyer better than almost any other life insurance product. But its design also makes it useful in a few situations most people never think about. This section covers both the people the product is made for and the less-obvious ways it can be put to work.

The Primary Audience for Final Expense Insurance

The core buyer is a senior on a fixed income who has no funds set aside for final costs. For that person, a large traditional policy is often out of reach or simply more than they need. Burial insurance is sized and built for exactly this situation.

Three strengths make it such a strong fit:

| Strength | Why it matters for this buyer |

|---|---|

| Easy to qualify | Most policies use simplified or guaranteed underwriting, with no medical exam and often fast approval. Health issues that block other coverage usually do not block this. |

| Small, affordable amounts | Coverage usually runs between $5,000 and $25,000, which keeps the monthly cost low enough to fit a tight budget. |

| A rate that never changes | The premium is locked at your age when you buy and stays the same for life, so a fixed-income household always knows the exact cost. |

Put together, these features answer the three things this buyer worries about most: getting approved, affording the payment, and keeping that payment steady for life.

Less-Obvious Uses Worth Considering

The lifetime rate lock also makes a small whole life policy useful in cases that have nothing to do with a fixed-income senior. The key is that a rate locked at a young age stays low for life, and the policy has decades to build cash value.

One example is a grandparent buying a small policy on a grandchild. With the parents’ consent, this locks in a rock-bottom childhood rate that never rises, and gives the policy a lifetime to grow cash value.

Another is an adult child securing coverage for an aging parent. Acting sooner, while the parent is healthier, can mean the difference between locking in coverage now and later watching health changes restrict options or push the parent into a higher-cost tier. Buying a policy on another person requires insurable interest and their consent, which a close family member can usually demonstrate.

The takeaway is that the product’s flexibility reaches well beyond the typical senior buyer.

Policy Types: Level, Graded, Modified, and Guaranteed Issue

Final expense policies come in four main flavors, and the one you get depends mostly on your health. This section gives a quick overview of each, so you can see the whole landscape. The detailed information for each type lives on its own dedicated page.

Here is the big picture at a glance:

| Policy type | Health needed | Payout in years 1–2 |

|---|---|---|

| Level benefit | Best health | Full benefit from day one |

| Graded benefit | Moderate issues | Partial benefit that grows each year, full from year three |

| Modified benefit | More serious issues | Your premiums back, often with interest |

| Guaranteed issue | Any health | Your premiums back, often with interest |

One thing to watch for as you shop: the industry often mixes up the words “modified” and “graded” in its marketing, even though they are not the same thing. The notes below explain the real difference.

Level Benefit

Level benefit is the best tier, with the lowest rates. It pays the full death benefit from day one, with no waiting period.

To qualify, you generally need to be in good health, with no significant conditions that would push you into a lower tier. [Internal link: Level Benefit guide]

Graded Benefit (True Graded)

A true graded policy pays only a part of the benefit if you die in the first two years, and that part usually grows each year. After year two, it pays the full benefit. A common example pays roughly 30% in year one, 70% in year two, and 100% from year three on.

It is built for people with moderate health issues who do not qualify for level coverage but can still pass a tier of health questions. [Internal link: Graded Benefit guide]

Modified Benefit

Modified benefit, sometimes called return-of-premium, returns the premiums you paid (often with a small amount of interest) if you die during a two-year waiting period. After that, it pays the full benefit.

Here is the part that marketing often blurs: modified still requires you to pass a tier of health questions on that carrier’s application. If you do not pass, that carrier declines you. Modified is not the same as guaranteed issue. [Internal link: Modified Benefit guide]

Guaranteed Issue

Guaranteed issue asks no health questions at all. Anyone within the carrier’s age range is automatically approved.

Its payout looks a lot like modified: your premiums back (often plus interest) during a two-year waiting period, then the full benefit after. The key difference is the qualifying step. Guaranteed issue has none, while modified still makes you pass a health question tier.

Why the Same Person Gets Different Rates from Different Carriers

Here is something many people never learn: the same person can get very different answers from different insurance companies. One carrier might offer full coverage at a low rate, while another might put that identical applicant in a worse tier or turn them down. With burial insurance, the carrier you apply to matters a great deal. The three areas below are where companies differ most.

Health Underwriting Varies by Carrier

Each carrier sets its own rules for treating a given health condition, and those rules are far from uniform. One company may accept a condition at the tier level, while another may grade it or decline it outright.

The examples are real. A person with diabetes and neuropathy might land at level coverage with one carrier and be graded with another. Someone with COPD might be declined by one company and accepted at a level plan by another.

These underwriting niches are not small details. Placing an application with the right carrier can be the difference between full coverage on day one and a two-year waiting period.

Gender Pricing Varies by Carrier

Companies also price men and women differently, each using its own mortality data and pricing models. Because of that, the company with the lowest rate for a 65-year-old man is often not the lowest for a 65-year-old woman with the same health.

The lesson is simple. There is no single “cheapest company” for everyone. The best rate depends on who is applying.

Tobacco Pricing and Look-Back Periods Vary by Carrier

Tobacco is treated differently from one carrier to the next, too. The smoker surcharge usually runs about 30% to 50% above the non-tobacco price, but the exact amount varies by location.

The look-back period also varies. In the broader market, it can range from 12 months to 5 years, though a 12-month look-back is the standard in the final expense world. Palmetto Mutual works only with carriers that use a 12-month look-back, so a former smoker who has been quit for a year qualifies for non-tobacco rates with the carriers we represent.

That one difference can meaningfully change the monthly price for someone who recently quit.

How to Apply and Who to Work With

When you buy final expense insurance, you are really choosing along two separate lines: who you work with, and how you meet with them. Neither choice is right nor wrong. Each has its own trade-offs, and the goal here is simply to help you see which combination fits your comfort level.

Captive Agent vs. Independent Broker

A captive agent represents a single insurance company. That focus has a real upside: deep knowledge of that one carrier’s products, underwriting quirks, and rates. The trade-off is that they are limited to what that one company offers, so if you are not a good fit there, they cannot place you elsewhere.

An independent broker represents several carriers. They can shop your application across companies to find the best fit for your health, gender, tobacco status, and budget. The tradeoff runs the other way: they usually have less depth on any single carrier than a captive agent would.

| Captive agent | Independent broker | |

|---|---|---|

| Carriers | One company | Several companies |

| Strength | Deep expertise on that one carrier | Can shop for the best fit across carriers |

| Tradeoff | Cannot place you elsewhere if you don’t fit | Usually less depth on any single carrier |

In-Home Visit vs. Phone Appointment

The second choice is how the application gets done. An in-home visit means the agent meets you face-to-face, traditionally at the kitchen table. It suits people who value a personal relationship and like having someone present to walk them through it.

A phone or virtual appointment means the application is completed over the phone from your own home. There is no home visit and no scheduling around an agent’s travel, and the process is generally faster. It suits people who prefer convenience and would rather not have a stranger come to the house.

| In-home visit | Phone appointment | |

|---|---|---|

| Where | At your kitchen table | From your home, by phone |

| Best for | Personal, face-to-face connection | Convenience and speed |

| Pace | Set by the visit | Generally faster |

Both paths lead to the same kind of funeral insurance coverage. What differs is the experience of getting there, and that is a matter of personal preference.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.