Home > Final Expense Insurance > Is It Worth It

Is Final Expense Insurance Worth It? In 2026, For Most People Over 50 — Yes

Is final expense insurance worth it? For most people over 50, the answer is yes. The reason is simple: a small whole life policy turns a funeral bill that often runs past $10,000 into a fixed monthly payment your family never has to scramble to cover. You are not buying a bill — you are handing the risk to an insurance company instead of leaving it with the people you love.

This page takes a clear position, but it will also be honest with you. There are a few situations where coverage is not the right move, and we will walk through those plainly so you can decide for yourself.

You will get a quick decision framework near the top, straight answers to the most common reasons people hesitate, and a clear next step at the end. You came here to make a decision, so let’s get to it.

Is Final Expense Insurance Actually Worth the Monthly Premium?

For most people over 50, yes — final expense insurance is worth the monthly premium. But whether it’s worth it for you comes down to one question, and it isn’t about the premium at all. It’s about whether your family could cover your funeral out of pocket, on short notice, without strain.

This section gives you the answer in three steps: the one money question that decides everything, a quick framework you can check off in five minutes, and an honest word about who this page is and isn’t for.

The $12,000 Question Most Families Can’t Answer

Here is the question that matters most. If you passed away tonight, could your family write a check for your full funeral by the end of the week — without borrowing, without a credit card, without asking relatives to chip in?

A full traditional funeral runs higher than most people expect. The national median for a funeral with viewing and burial is about $8,300, and once you add a vault, a cemetery plot, and a grave marker, the all-in total commonly lands near $12,000.

For many families, that check is hard to write on short notice. The Federal Reserve has found year after year that about 37% of U.S. adults — nearly 4 in 10 — could not cover even a surprise $400 expense with cash or its equivalent.

If a $400 bill is a stretch for that many households, a $12,000 funeral bill is out of reach for far more. This is not meant to frighten you. It’s simple math, and it’s the real test of whether final expense insurance is worth it for your family.

The 5-Minute Decision Framework

Here is a quick way to decide. Read each question and answer it honestly with a yes or no.

| Ask yourself | Your answer |

|---|---|

| Do you have $12,000 or more in liquid cash set aside just for funeral costs? | Yes / No |

| Does your immediate family have $12,000 or more they’re willing to spend on your funeral? | Yes / No |

| Do you carry permanent life insurance over $25,000 that will not expire? | Yes / No |

| Have you already pre-arranged and fully paid for your funeral? | Yes / No |

| Are you comfortable with your family covering any shortfall themselves? | Yes / No |

If any answer is “no,” a policy is mathematically justified — it fills a gap your family would otherwise have to fill themselves. If every answer is “yes,” the next section may apply to you, and that’s worth reading too.

Why This Page Takes a Position

This page is not a neutral list of pros and cons. It takes a position, because after years of sitting with families who were facing a funeral bill in real time, the pattern is clear: for most people over 50, the math favors having coverage.

That said, this page will also be honest about who final expense insurance is not for. The very next section covers the situations where coverage may not be the right move right now. The goal here is a clear decision, not a sale — so you’ll get the case for the product and the honest exceptions, side by side.

The “Savings Account” Trap: Why Saving $50 a Month Often Fails

“I’ll just save the money myself” is the most common reason people skip burial life insurance. It sounds responsible, and on paper it looks like the cheaper path. But it usually fails — not because of the money, but because of time.

Saving builds slowly. Insurance pays in full right away. That gap in timing is the whole problem, and it’s the reason a savings account often can’t do the job a policy does.

The Math — 20 Years to Reach What Insurance Delivers on Day One

Saving your way to a full funeral fund takes longer than most people think. At $50 a month in a high-yield account earning about 4% a year, it takes roughly 15 years to reach $12,000. With no interest at all, it’s a flat 20 years.

The trouble is the timeline. Most people shopping for final expense are already in their 60s or 70s, so a 15-to-20-year savings runway often runs past their life expectancy. The money simply may not have time to grow.

A level final expense policy works the other way. It pays the full benefit from day one — the first month the policy is in force, your family is covered for the entire amount. The policy buys the time that saving cannot.

| Monthly deposit | Years to reach $12,000 (at 4% APY) |

|---|---|

| $25 | About 24 years |

| $50 | About 15 years |

| $75 | About 11 years |

| $100 | About 8 years |

| $150 | About 6 years |

The Year 2 Problem — Savings vs. Policy Side-by-Side

The clearest way to see the trap is to compare two people. Both are 65. One starts saving $50 a month; the other buys a $12,000 policy at about $60 a month. Both pass away two years later, at 67.

| Savings account path | Policy path | |

|---|---|---|

| Monthly commitment | $50 | $60 |

| Total paid over 24 months | $1,200 | $1,440 |

| Balance or benefit at death | About $1,250 | $12,000 |

| Family shortfall on funeral | $10,750 | $0 |

| Tax treatment | Interest is taxable | Death benefit is tax-free |

The saver did everything right and still left their family about $10,750 short. The policyholder paid a little more each month and left their family fully covered, tax-free.

What Happens to the Savings Account When You Actually Need It

There’s a second problem with the savings plan. A “funeral fund” rarely stays a funeral fund.

Over a 15-to-20-year window, life happens. A medical bill, a car repair, a leaking roof, or a grandchild who needs help — all of it pulls from the account that was supposed to be untouchable.

A funeral life insurance policy doesn’t work that way. Once the premiums are paid, the death benefit is locked in by contract and reserved for your beneficiary. Everyday emergencies can’t drain it.

When Saving Actually Does Work (The Honest Exception)

Saving instead of buying coverage can make sense — for the right person. If you’re under 50, in good health, earning a strong income, and you can realistically build $25,000 or more in a dedicated account within a decade, self-funding may be enough.

For that profile, a high-yield savings account, or a small permanent policy as a backstop, can do the job. But for most people over 55, or anyone whose health is declining, the timeline doesn’t cooperate — and that’s exactly where a policy earns its place.

When Final Expense Might Not Be the Right Move Right Now

This page makes the case for coverage, but honesty cuts both ways. There are real situations where a policy isn’t the right step right now, and you deserve to hear them plainly.

None of these have anything to do with how much money you have. They come down to two simple things: your monthly budget and whether the need is already covered.

If the Premium Would Stretch Your Monthly Budget Past Comfort

A policy that causes you stress every month isn’t the right policy. If the premium would crowd out groceries, medication, or your other bills, that’s a real problem worth taking seriously.

But the answer usually isn’t “no coverage.” It’s a smaller policy. A $5,000 plan covering a direct cremation and immediate costs — which run about $1,500 to $3,000 — beats having no coverage at all.

The goal is to right-size the coverage to fit your budget, not to walk away from it. A quick rate calculator can help you find a face amount and premium that sit comfortably in your monthly plan.

If You Already Carry Permanent Life Insurance Over $25,000

If you already own a permanent life insurance policy worth more than $25,000, a separate burial insurance policy may simply be redundant. The end-of-life need is already covered by what you have.

The key word is permanent. This means whole life, universal life, or guaranteed universal life — a policy built to last your whole life and pay out whenever you pass.

Term life insurance does not count here, because term policies expire. Many term policies are marketed in ways that sound permanent, so check that yours has a lifetime guarantee and won’t lapse at a certain age. If it expires, the coverage may not be there when your family needs it.

If You’ve Already Pre-Arranged and Paid for Your Funeral in Full

If you’ve already pre-planned and fully paid for your funeral with a reputable funeral home, the core need is handled. There may be no reason to add a policy on top of it.

It’s worth knowing that pre-paid plans carry their own risks. If the funeral home closes or you move out of the area, your plan may not transfer cleanly, and some states offer weak protection for pre-paid funds.

Still, if your arrangement is fully paid, locked in, and properly protected, the core expense is covered. For readers weighing this path, the pre-paid funeral plans guide walks through what to check before deciding.

What to Do If One of These Applies to You

If one of these three situations fits you, thank you for reading this far — and know that much of the rest of this page may not apply to your situation. That’s a good place to be.

If you’re still gathering information, other resources on the site may serve you better from here. The complete final expense guide covers the basics from the ground up, and the comparison guides can help if you’re still weighing your options. No pressure either way.

Debunking the $255 Social Security Death Benefit Myth

Many families assume Social Security will help pay for a funeral. There is a death benefit — but it’s $255, and most people misunderstand both how small it is and how few families actually receive it.

Knowing the real numbers here matters, because it directly affects whether you need funeral insurance to cover the gap.

What the $255 Social Security Benefit Actually Is

Social Security pays a one-time Lump-Sum Death Payment of $255 to certain survivors. The amount was capped at $255 by the Social Security Amendments of 1954, and it has never once been adjusted for inflation.

To put that in perspective, if the $255 had simply kept pace with inflation since 1954, it would be worth roughly $2,900 today. A 2024 Senate bill proposed raising it to exactly that — $2,900 — to reflect the cost of living, but it has not become law.

Even at $2,900, it still wouldn’t cover a modern funeral. At $255, it covers almost none of it.

Who Actually Qualifies for the $255 Payment

Most people assume the $255 goes to whoever pays for the funeral. It doesn’t. It cannot be paid to a funeral home, a friend, or an extended family member.

The payment goes first to a surviving spouse who was living with the person who died. If there’s no eligible spouse, it can go to a child who already qualifies for Social Security benefits on the parent’s record — generally a minor, a student under 19, or an adult disabled before age 22.

This leaves many families with no eligible recipient at all. Financially independent adult children don’t qualify, and an unmarried person with no dependent children often has no one who can claim it. In fact, federal data shows that in 2023, fewer than 38% of insured-worker deaths resulted in any payment being made.

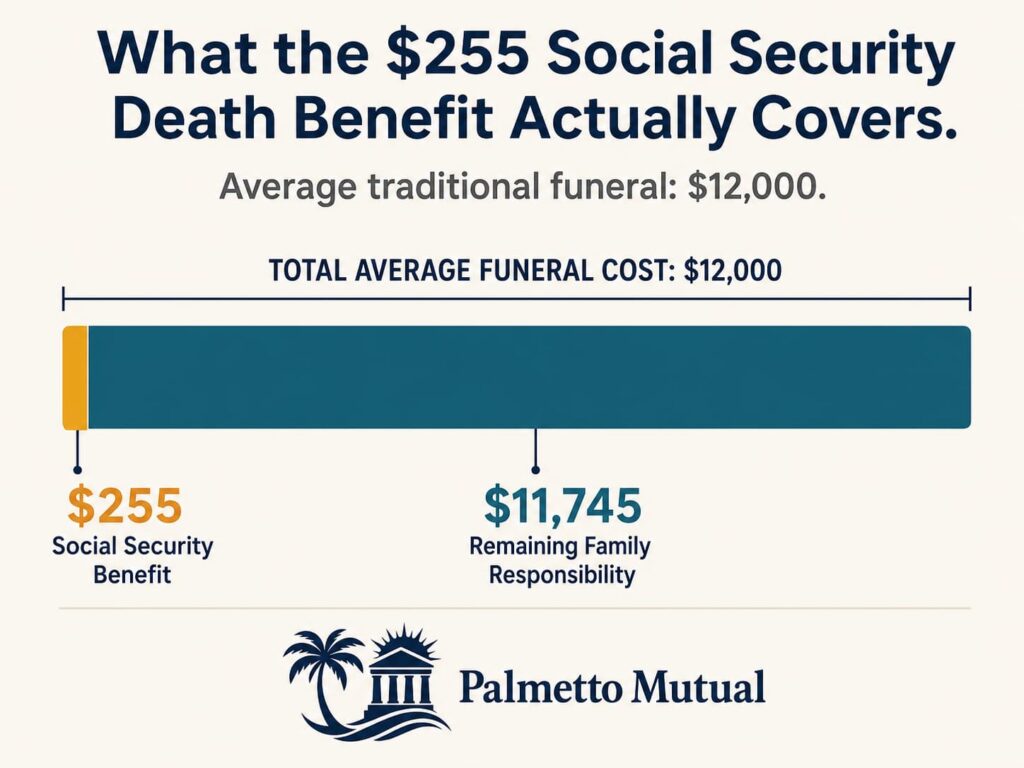

What $255 Actually Covers in 2026

The math is stark. A traditional funeral with viewing and burial commonly runs about $9,000 to $12,000 once you include a vault, plot, and marker, while a direct cremation runs about $1,500 to $3,000.

So $255 covers roughly 2% to 3% of a traditional funeral, or somewhere between 8% and 17% of a direct cremation. It might cover a portion of the flowers.

It does not cover the casket, the embalming, the service, the cemetery plot, the headstone, or the funeral director’s fees. The bulk of the bill still lands on the family.

| Item | Amount |

|---|---|

| Total traditional funeral | $12,000 |

| Covered by $255 Social Security benefit | $255 |

| Remaining family responsibility | $11,745 |

The point of this picture is the size of the gap. No one who sees $255 next to $12,000 walks away thinking Social Security “handles it.”

Other Government Programs That Don’t Cover the Gap

Other programs people count on don’t fill this gap either. Medicare is health insurance for living beneficiaries and pays nothing toward a funeral. Medicaid does not pay funeral costs. And SSI has no burial payout of its own.

Some states and counties run small indigent-burial programs for families in extreme financial need. These typically provide only a basic direct burial or cremation, with no service.

The honest takeaway is simple. The federal government does not cover end-of-life costs in any meaningful way, which is why planning for this expense falls almost entirely to the individual and the family.

Note: this section discusses end-of-life costs and benefits, which can be a heavy topic. If any of it raises personal concerns, a benefits counselor at your local Social Security office or Area Agency on Aging can talk through your specific situation.

The Real Cost of Waiting: Age-Banded Premiums and Health Declines

Waiting to buy coverage feels harmless. It isn’t. With final expense insurance, two separate forces work against you every year you wait — your age and your health — and both can only move in one direction.

This section explains the mechanism behind both, so you can see why “later” almost always costs more than “now.”

How Age-Banded Premiums Actually Work

Final expense premiums are set by your age on the day you apply — not your age when the policy pays out. Every birthday moves you into a higher age band, and a new policy costs more as a result.

This is not a rate hike on a policy you already own. Once your policy is issued, your premium is locked for life and never goes up. The increase only applies to new applicants, because each year you’re one year closer to the actuarial event the carrier is pricing for.

So the cost of waiting isn’t theoretical. The same coverage simply carries a higher price tag the day after each birthday, and that higher price then locks in for the life of the new policy.

The Premium-by-Age Table

The table below shows how the monthly cost of the same $15,000 level policy climbs with age. The progression is the point: the coverage doesn’t change, but the price does.

| Age at Application | Female (monthly) | Male (monthly) |

|---|---|---|

| 55 | $40 | $53 |

| 60 | $48 | $65 |

| 65 | $60 | $84 |

| 70 | $79 | $111 |

| 75 | $108 | $149 |

| 80 | $147 | $208 |

Sample monthly rates for level benefit at $15,000 of coverage, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

As a general pattern, the same face amount often costs roughly two to three times as much at 75 as it does at 55 — which is why locking in earlier matters. Readers looking for their own decade can see the age-specific guides, such as the cost of coverage at 65 and similar pages.

How a Single Health Diagnosis Can Change Your Eligibility Tier

Age is only half the story. Your health determines which underwriting tier you qualify for, and the tiers carry very different prices and waiting periods.

There are three main tiers. Level benefit offers the best rates and full coverage from day one. Graded benefit costs more and pays only a partial benefit in the first couple of years. Guaranteed issue is the most expensive and comes with a waiting period before the full benefit is available.

| Level benefit | Graded benefit | Guaranteed issue | |

|---|---|---|---|

| Typical health profile | Good, moderate, or managed conditions | Serious Health Conditions | Very Serious Conditions |

| Cost vs. Level | Baseline (lowest) | Higher than Level | Highest |

| Waiting period | None — immediate | 2 years | 2 to 3 years |

| Death benefit during waiting period | Full benefit from day one | Partial benefit (often around 30–40% in year one and 70–80% in year two; varies by carrier) | Return of premiums paid, plus interest |

The exact cost difference between tiers depends on the carrier and is best seen through the rate calculator. The structure, though, is consistent across the industry.

Here’s why this connects to waiting. A single new diagnosis — a recent heart attack, COPD on oxygen, or certain cancers — can move you from Level to Graded, or from Graded to Guaranteed Issue, from one year to the next. The same policy can suddenly cost more and carry a waiting period it didn’t have twelve months earlier. Readers managing a specific condition can see the dedicated guides, such as the diabetes and heart condition pages.

Why “I’ll Wait Until Next Year” Is the Most Expensive Decision

Put the two forces together and the cost of waiting compounds. Wait one year, and you pay one year more of age-banded premium — and you risk a health event that permanently changes which tier you qualify for.

That’s why “I’ll think about it” is rarely a neutral choice. It’s an active financial decision with a real, measurable cost attached to it.

If a disqualifying health event has already happened, coverage still exists — guaranteed issue policies are built for exactly that situation . But because guaranteed issue is the most expensive path and includes a waiting period, it’s best treated as a backstop, not a first choice, while level coverage is still on the table. The reason burial insurance rewards acting sooner is simply that both the clock and your health history only move one way.

Why Funeral Homes Increasingly Require Payment Before Services

There’s a shift in the funeral business that most families don’t learn about until they’re standing at the counter. The way and the timing of payment has changed, and it changes the math on whether you need coverage.

This isn’t a scare tactic — it’s a plain look at how the industry actually operates today.

The Shift from Billing to Upfront Payment

Funeral homes used to run on trust. Services were performed, the family was billed, and payment followed over the next month or two.

That model has largely faded. Today, most funeral homes require full payment, or a substantial deposit, before services begin. A commonly cited reason is simple: funeral homes too often performed services and were never paid, leaving them to absorb the cost.

This isn’t true at every funeral home, and some still offer payment plans or deposits. But upfront payment has become the standard expectation, particularly at larger and corporately owned providers.

What “Payment Before Services” Actually Means in Practice

Here’s how it usually unfolds. After a death, the family contacts a funeral home. Before the body is even transported, the funeral home typically asks how the bill will be paid and may require a deposit or proof of a payment method.

Before embalming, preparation, or any visible services begin, the rest of the payment is often required or secured.

A family without quick access to $8,000 to $12,000 can stall right at the first step. The arrangements wait until the funds are sorted out — which is a hard place to be in the first hours after losing someone.

How a Final Expense Policy Changes This Dynamic

This is where funeral life insurance fits the moment. Many final expense carriers allow an assignment of benefits, which lets the death benefit be paid straight to the funeral home instead of reimbursing the family later.

On a clean, complete claim filed outside the two-year contestability period, some final expense carriers can move quickly — at best within a few days, and a handful advertise as fast as 24 to 48 hours. More commonly, claims take from about a week to several weeks, so the realistic benefit is speed relative to paying out of pocket and waiting, not instant funds.

Either way, an assignment lines the policy’s payout up with the funeral home’s payment request far better than scrambling for cash. Without coverage, families lean on savings, credit cards, or funeral loans to bridge the gap — each of which carries its own cost.

What the Industry Shift Means for Your Decision

The upfront-payment trend changes the picture for anyone who assumed they could “figure it out” after a death. The window to figure it out has shrunk from weeks to, in many cases, hours.

Even a family with moderate savings can be caught flat-footed when a funeral home asks for several thousand dollars before moving the body. So the real question isn’t only whether the money exists somewhere — it’s whether it’s accessible on the timeline the industry now expects. That timing problem is the gap a policy is built to close.

Your Policy as a Guaranteed Inheritance, Not Just a Funeral Fund

Most people think of a final expense policy as money for a funeral. It’s that — but for many families, it’s something more.

For a middle-income household, this small policy is often the only guaranteed, tax-free sum of money a person can be certain they’ll leave behind. That changes what it really is.

Most Middle-Income Families Won’t Leave a Traditional Inheritance

Here’s a reality that surprises people. The median retirement savings for Americans aged 65 to 74 is about $200,000.

That sounds like a lot until you watch where it goes. Healthcare costs, everyday living, and the chance of needing long-term care all draw it down — and more than 70% of people who reach 65 will need some long-term care in their lives. Home equity often goes toward that care, too.

By the time a middle-income person passes, there’s frequently little left to hand down. That isn’t a failure, it’s just how modern retirement works. But it does mean the inheritance many families pictured doesn’t always show up.

A Final Expense Policy Is Contractually Guaranteed

This is where a policy stands apart. Retirement accounts rise and fall with the market. Home equity and savings can be drained by medical bills or a long life.

A final expense policy’s death benefit works differently. Once the policy is in force and any waiting period has passed, the carrier is legally required to pay the full face amount to your named beneficiary.

No market downturn shrinks it. No surprise expense drains it. It pays exactly what the contract promises, which is something almost nothing else in a retirement budget can claim.

What’s Left After the Funeral Goes to Your Family

Now the part most people overlook. If the policy pays $15,000 and the funeral costs $9,000, the remaining $6,000 belongs to your beneficiary.

They decide what to do with it — pay off a small debt, cover their own bills during time off to grieve, help a grandchild, or simply keep it. It’s money that would not have existed otherwise.

For many families, this is the only tax-free cash gift they’ll ever receive from a parent or spouse. The policy quietly turns into a small legacy on top of covering the funeral.

The “Legacy Math” Most People Never Consider

The numbers make the point better than words. The example below is illustrative — actual premiums depend on age, health, sex, and carrier, and the on-site rate calculator returns real figures.

| Amount | |

|---|---|

| Policy purchased at age 65 | $15,000 face amount |

| Monthly premium (illustrative) | About $75 |

| Total premiums paid by age 82 (life expectancy) | About $15,300 |

| Death benefit paid to family | $15,000 |

| Funeral costs covered | About $9,000 |

| Net tax-free cash to beneficiary | About $6,000 |

Look at what this shows. Over a normal lifetime, the total paid in roughly equals the benefit paid out — so the coverage nearly breaks even on its own.

And on top of breaking even, it still delivers about $6,000 in tax-free cash that wouldn’t have existed. That reframes the premium from an “expense” into something closer to forced savings with a guaranteed payout at the end.

“I’m on a Fixed Income” — Why This Is the Only Policy Built for That

If you’re living on a fixed income, you might assume insurance is one more bill you can’t take on. It’s worth looking closer, because final expense insurance is one of the few products actually built for a fixed budget.

The reason comes down to one feature that almost nothing else in retirement offers: a price that never moves.

The Premium Never Increases — Ever

Final expense is whole life insurance, and the premium is level for the life of the policy. The amount you’re quoted at 65 is the same amount you pay at 75, at 85, and at 95.

That’s very different from most coverage. Term insurance expires or renews at much higher rates. Medicare supplements tend to rise with age and inflation.

A locked-in premium is one of the only recurring costs a retiree can fix in place for good. Once it’s set, it simply doesn’t change.

Matching a Fixed Expense to a Fixed Income

For a Social Security recipient or a pension-only retiree, predictability is everything. Nearly every other cost keeps climbing.

Take Medicare Part B: the standard premium rose to $202.90 a month in 2026, up from $185.00 in 2025 — the first time it has crossed $200. Rent, groceries, and auto and home insurance all push higher year after year too.

A final expense premium sits still through all of it. It becomes a known, fixed line in the budget — easier to plan around than almost any other bill you have.

| Expense | Cost trajectory over time |

|---|---|

| Final expense premium | Flat — locked for life |

| Medicare Part B premium | Rising (e.g., $185.00 in 2025 to $202.90 in 2026) |

| Average rent | Rising year over year |

| Average grocery costs | Rising year over year |

| Medicare supplement premium | Rising with age and inflation |

The flat line against all the rising ones is the whole argument. On a fixed income, a cost that never moves is rare and valuable.

Why “I Can’t Afford It” Often Means “I Can’t Afford the Wrong Size”

Here’s the part worth slowing down on. Many people decide they can’t afford any policy because they were quoted on $25,000 or $30,000 of coverage.

The fix usually isn’t walking away — it’s choosing a smaller face amount. A $5,000 or $7,500 policy covering a direct cremation and immediate costs often lands in the range of roughly $25 to $45 a month for many applicants in their 60s and early 70s, though it varies by age, sex, health, and carrier.

For many budgets, that’s closer to a streaming subscription than a mortgage payment. The rate calculator can show the face amount and premium that fit comfortably, so funeral insurance becomes a question of what size, not whether at all.

The 48 Hours After Death: With Coverage vs. Without

The real difference a policy makes shows up in the first two days. The same 48 hours play out in two very different ways depending on whether coverage is in place.

This is the heart of it — not a sales point, but the lived experience your family will or won’t have.

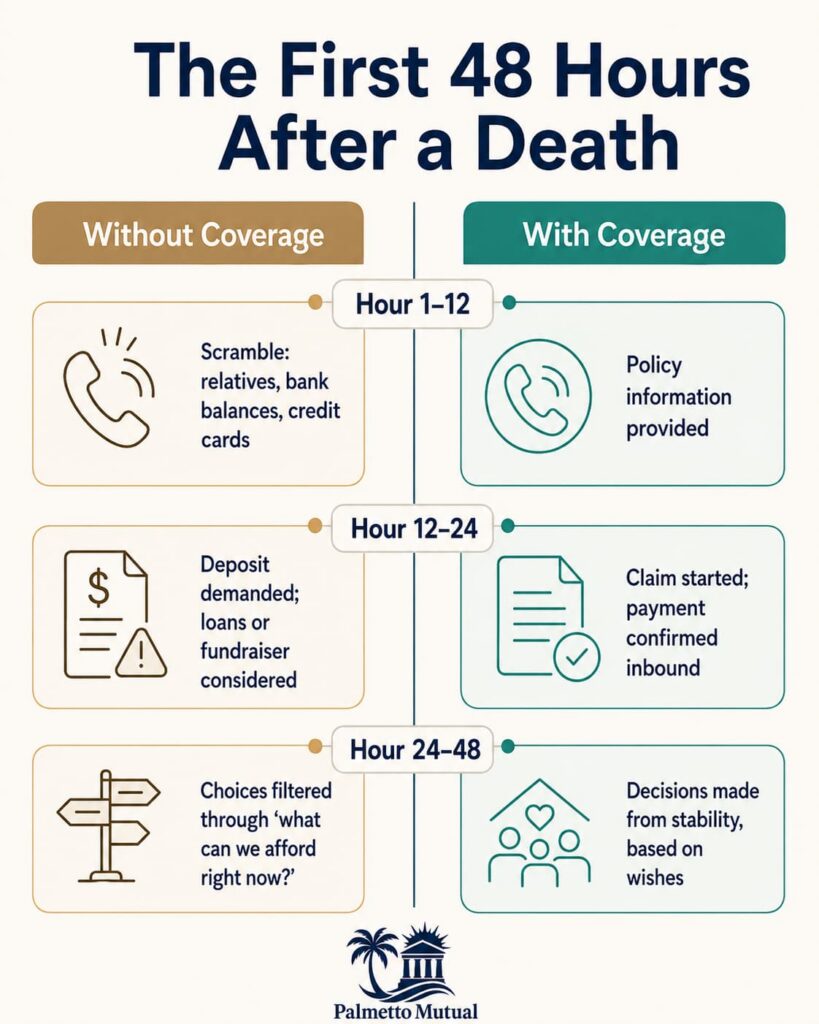

Hour 1 to 12 — The First Calls

In the first hours, the family contacts the funeral home. Often, questions about payment come up right alongside questions about arrangements.

Without coverage, the family lands in crisis mode quickly — calling relatives, checking bank balances, opening credit card apps, wondering whether to start a fundraiser. The grief and the math collide at once.

With burial life insurance in place, the conversation is calmer. The family shares the policy information, the funeral home can begin coordinating with the carrier, and everyone moves to the next decision instead of the next dollar.

Hour 12 to 24 — The Payment Request

Within the first day, funeral homes typically ask for a deposit or full payment to begin preparations. This is where the two paths separate sharply.

Without coverage, this is often where families strain — debating who pays, whether to pool money, whether to take out a funeral loan, whether to cut back on the service. Some turn to GoFundMe, but it’s a slow and uneven safety net: funeral campaigns do better than medical ones, yet roughly one in three still fall short of their goal, and success leans heavily on having a well-connected, well-off network. The money also trickles in over weeks, not hours.

With coverage, the claim has often already been started, and the funeral home has confirmation that payment is on the way.

Hour 24 to 48 — The Service Decisions

By the second day, families make the real choices — casket, service type, burial or cremation, headstone. These decisions carry weight.

Without coverage, every choice runs through one filter: “what can we afford right now?” That pressure often pushes families toward cheaper options chosen in a rush and regretted later.

With coverage, the family chooses based on what they actually want to do. The policy lifts the money question out of an already painful 48 hours.

The Side-by-Side Timeline

The contrast is clearest laid out hour by hour.

| Time | Without coverage | With coverage |

|---|---|---|

| Hour 1–12 | First call; payment questions trigger scramble — relatives, bank balances, credit cards | First call; policy information provided; funeral home begins carrier coordination |

| Hour 12–24 | Deposit requested; family debates funds, loans, or a fundraiser that may fall short | Claim started; funeral home has confirmation payment is inbound |

| Hour 24–48 | Service decisions filtered through “what can we afford right now?” | Service decisions made from stability, based on wishes |

This is the felt difference between the two paths. Same loss, same timeline — two very different experiences for the people left behind.

Claim Processing and Payout

A quick word on how the payout actually works. On a clean, complete claim filed outside the two-year contestability period, some final expense carriers can pay quickly — at best within a few days, with a handful advertising 24 to 72 hours — though many claims take from about a week to several weeks.

Payment goes to the named beneficiary by direct deposit or check, or directly to the funeral home through an assignment of benefits. The death benefit is paid income-tax-free to beneficiaries.

And because a living beneficiary is named on the policy, the payout passes outside of probate and reaches your family directly. That direct, fast, tax-free handoff is exactly what makes the “with coverage” timeline above possible.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.