Home > Final Expense Insurance > Cremation Insurance Coverage

Cremation Insurance: Coverage for Cremation Services

Cremation insurance is a small whole life policy that helps cover the cost of cremation and any related services. It is the same product as final expense insurance — just sized to fit what cremation actually costs. This guide explains how the coverage works, what a policy can pay for, how it stacks up against pre-paid cremation plans, and what you can expect to pay by age.

What Is Cremation Insurance?

Cremation insurance is not a special or separate product. It is the same small whole life policy people use to cover a burial — just set at a lower amount that fits what cremation costs. You may also hear it called burial insurance or funeral insurance, but it works the same way no matter the name.

Because cremation costs less than a traditional burial, most people don’t need a large policy to cover it. Coverage in this range usually runs from about $2,000 to $7,000. That smaller amount is the whole reason cremation insurance stays affordable for most buyers.

It helps to know roughly what cremation actually costs before choosing an amount. A direct cremation — no service, just the cremation itself — often runs around $1,500 to $2,500, though prices vary a lot by location. Add a memorial service, a nicer urn, or a viewing, and the total can climb to $5,000 or more.

So when you size a cremation policy, you are really just matching the coverage to the kind of send-off you want. A small policy covers the cremation. A slightly larger one leaves room for a service or a little extra for family.

The key thing to remember is this: a small face amount keeps the monthly premium low. Even at older ages, a policy built around cremation costs is usually one of the more affordable forms of final expense insurance a person can buy.

Do You Have to Stay Under $10,000? Coverage for Cremation Plus Extras

Not at all. Choosing cremation does not lock you into a small policy. Some people want enough to cover the cremation and a little more — a memorial service, an upgraded urn, a celebration of life, or simply some cash left behind for a loved one.

Cremation insurance has no ceiling that forces you to stay at $5,000 just because you’re planning cremation. If you want a larger policy, you can take out $10,000, $15,000, $25,000, or more. The coverage is sized to match what you want it to do.

A simple way to think about it is in three tiers, based on what you want the money to cover:

| What you want covered | Typical coverage range |

|---|---|

| Cremation only (the cremation and basic costs) | $2,000 – $7,000 |

| Cremation plus a memorial or ceremony | $7,000 – $15,000 |

| Cremation, extras, and money left for a beneficiary | Any amount above that |

The point here is flexibility, not buying more than you need. You decide what you want the policy to handle — just the cremation, a full ceremony, or a gift to family — and the coverage is built to fit that choice. A larger policy isn’t “better.” It’s simply the right size if you want it to do more.

This is one of the quiet advantages of funeral insurance over a fixed cremation plan: you are never boxed into a single dollar figure. The coverage bends to your wishes, not the other way around.

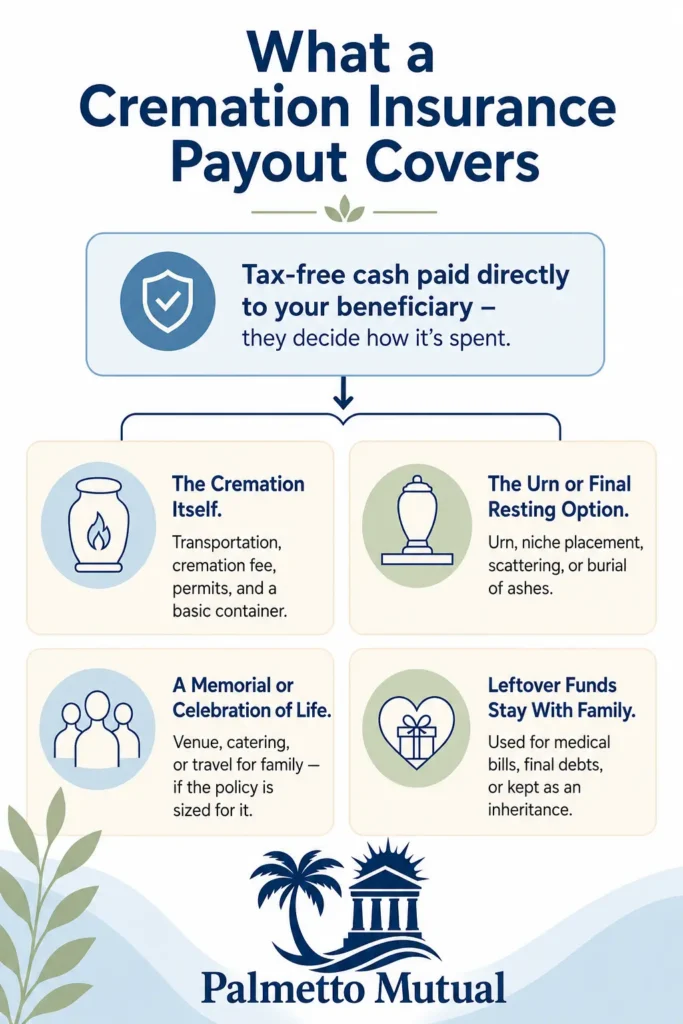

What a Cremation Insurance Payout Actually Covers

Here is the part that surprises many people: a cremation insurance policy does not pay a funeral home directly. It pays cash to the person you name as your beneficiary — usually a spouse, an adult child, or whoever you choose.

That money arrives as a tax-free check. Life insurance death benefits paid as a lump sum are generally not counted as taxable income. Your beneficiary does not owe income tax on it.

And there are no rules on how the money is spent. It does not have to go toward cremation at all. The beneficiary decides what to do with every dollar — that is simply how this type of final expense insurance works.

Below is a look at what the payout commonly goes toward.

The Cremation Itself

The most basic use is covering the cremation. That usually includes transporting the deceased, the cremation fee itself, the required permits and paperwork, and a simple cremation container.

For a direct cremation, this is often the bulk of the cost. A small policy is usually enough to cover this part with little trouble.

The Urn or Final Resting Option

After the cremation, the family decides what to do with the ashes. The payout can cover an urn, placement in a niche at a cemetery, a scattering service, or burial of the ashes if that is what the family prefers.

These choices range from very low cost to a few hundred dollars or more. Having cash on hand lets the family pick what feels right without worrying about the price.

A Memorial Service or Celebration of Life

If the policy is sized for it, the payout can also fund a gathering. That might be a memorial service, a venue rental, catering, or even travel costs so family members can attend.

This is where a slightly larger policy helps. A direct cremation may cost little, but a service with friends and family adds to the total.

Any Leftover Funds Go to the Beneficiary

This is the key point. Whatever is left after the cremation and any services belongs to the beneficiary. There is no rule that says unused money must go back to anyone.

The family can put it toward medical bills, final debts, or simply keep it as a small inheritance. That freedom — money that stays with your loved ones — is what sets a life insurance policy apart from a pre-paid plan, which is exactly what the next section covers.

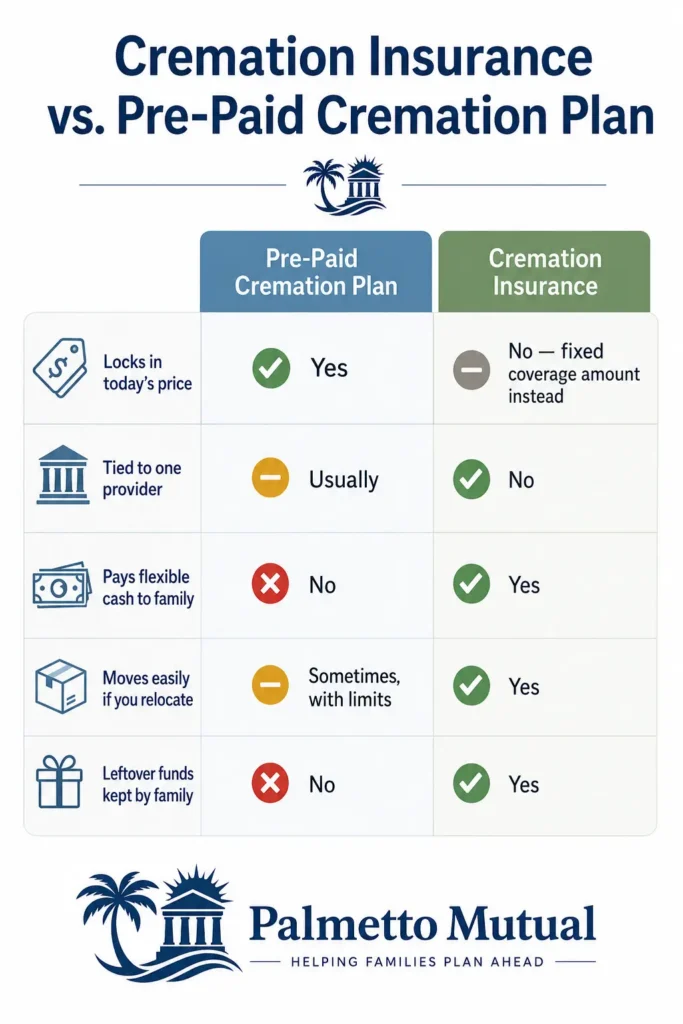

Cremation Insurance vs. Pre-Paid Cremation Plans

Let’s be fair from the start: pre-paid cremation plans are real, legitimate, and a reasonable choice for some people. At most funeral homes, you can prepay for a direct cremation, a memorial service, an urn, or even niche placement.

The biggest draw is price lock-in. You pay today’s price, and the plan protects you from future cost increases — a genuine benefit when funeral prices keep rising.

That said, a pre-paid plan can do some things a policy can’t, and a policy can do some things a plan can’t. Here is the short version before we walk through the details.

| Feature | Pre-paid cremation plan | Cremation insurance |

|---|---|---|

| Locks in today’s price | Yes | No (fixed coverage amount instead) |

| Tied to one provider | Usually | No |

| Pays flexible cash to family | No | Yes |

| Moves easily if you relocate | Sometimes, with limits | Yes |

| Leftover funds kept by family | No | Yes |

Your Money Is Locked to One Funeral Home

With a pre-paid plan, you have committed to a specific provider. You can often transfer the plan to another funeral home, but the new provider is not required to honor your original locked-in prices.

In many cases, only the cash value moves to the new home, and it acts as a credit toward that home’s current prices. With burial insurance, the cash goes to your beneficiary, who can use any cremation provider, anywhere.

You Lose the Ability to Shop Around

Cremation prices vary widely between providers, even in the same town. Price differences of $1,000 to $3,000 for the same service are common.

A new, more affordable cremation service might open near you five years from now. With a pre-paid plan, you can’t take advantage of it. With insurance, your family chooses whatever provider makes the most sense when the time comes.

If You Move, Your Plan May Not Move With You

Relocation is one of the biggest risks of a pre-paid plan. If you retire out of state or move closer to family, transferring the plan can mean paying administrative fees, accepting worse terms, or losing your price guarantee.

In some cases, the body may need to be transported back to the original funeral home — which defeats the purpose of prepaying. A cash payout from funeral insurance simply follows your family wherever they are.

State Protections for Pre-Paid Funds Vary

Pre-paid funeral money is regulated state by state, and the protections are uneven. According to the Funeral Consumers Alliance, only a couple of states come close to truly consumer-friendly pre-need laws.

Most states require the money to be held in a trust or an insurance policy separate from the funeral home. Still, if the funeral home goes out of business, how smoothly your family recovers the funds depends heavily on your state’s rules.

Insurance Pays Cash — Period

Here is the core advantage. A life insurance beneficiary receives a cash check and has full freedom over how, where, and with whom to arrange services.

No single provider. No locked plan. No price tied to one location. That freedom is the product.

Does Social Security or the VA Pay for Cremation?

Many people assume that some mix of Social Security, Medicare, or VA benefits will cover their cremation. It is worth knowing exactly what these programs do — and do not — pay before counting on them.

The short version is that government help exists, but it is limited. None of these programs is designed to fully cover cremation, which is why many families still choose a small final expense insurance policy to fill the gap.

The $255 Social Security Death Benefit

Social Security pays a one-time lump sum of $255 to an eligible surviving spouse or, in some cases, a dependent child. You must apply within two years of the death.

That amount has not changed since it was capped in 1954. It will not make a real dent in cremation costs today. It helps a little, but that is all.

Medicare Does Not Pay for Cremation

Medicare is health insurance for the living. It does not cover funeral, burial, or cremation costs of any kind.

This surprises some families, but it is consistent across the board. Once a person passes, Medicare plays no role in paying for final arrangements.

VA Burial and Cremation Benefits Are Limited

For eligible veterans, the VA does provide some help, and it treats cremation the same as burial. Benefits can include burial in a national cemetery, a grave marker, a burial flag, and a partial allowance.

The dollar amounts depend on the type of death. For deaths on or after October 1, 2025, the VA pays up to about $1,002 for a non-service-connected death, plus a separate plot allowance, and up to $2,000 for a service-connected death.

Two things matter here. The VA pays the family back after they have already paid the provider — it is a reimbursement, not money up front. And for most non-service-connected deaths, the allowance covers only part of a full cremation plan.

So these benefits are genuinely helpful, but they rarely remove the need for a private burial insurance policy if the goal is to fully cover cremation without leaving a bill behind.

Cremation Insurance Rates by Age

The rates below are for readers looking to cover cremation specifically, usually in the $2,000 to $5,000 range. If you want more coverage for a ceremony or to leave extra funds behind, look back at the earlier section on coverage above $10,000.

The table below shows sample monthly premiums by age and coverage amount. These figures are populated from live carrier illustrations during production — the structure is set here for accurate, current rates to be dropped in.

| Age | $2,000 | $5,000 | $7,000 |

|---|---|---|---|

| 50 | $9 | $17 | $23 |

| 60 | $12 | $24 | $32 |

| 70 | $18 | $39 | $54 |

| 80 | $31 | $72 | $99 |

Sample monthly rates for male applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

| Age | $2,000 | $5,000 | $7,000 |

|---|---|---|---|

| 50 | $8 | $14 | $18 |

| 60 | $10 | $19 | $24 |

| 70 | $14 | $29 | $39 |

| 80 | $23 | $51 | $70 |

Sample monthly rates for female applicants, level benefit, non-tobacco. Rates require answering health questions, and approval is not guaranteed.

A few things shape what you actually pay. Rates vary by carrier, by your health class, and by gender, and they climb with age — which is why locking in a policy earlier usually means a lower lifetime premium.

The numbers above are representative examples, not guaranteed quotes. Your real rate depends on the carrier you qualify with and your personal details at the time you apply.

Which Carriers Write Cremation-Sized Policies?

Here is something most buyers never hear: not every final expense carrier will write a policy as small as $2,000. Some require a minimum of $5,000, $7,000, or even $10,000.

That matters a great deal if you only want cremation-sized coverage. Buying from the wrong carrier can mean paying for more coverage than you actually need.

Carriers That Start at $2,000

A smaller group of carriers will write policies with face amounts as low as $2,000. These are the specialists for cremation-only buyers who want to match the coverage closely to the cost.

Carriers That Start at $5,000 or Higher

Many of the larger, well-known final expense carriers set their floor at $5,000, $7,000, or $10,000. These are still good options if you are planning cremation plus a ceremony, or want some leftover funds for family.

But for a simple direct cremation, a $5,000-minimum policy may be more than you need. The coverage works fine — it is just larger than the bare cremation cost.

Why Working With a Broker Matters Here

This is where the type of agent you talk to makes a real difference. A captive agent works for a single company and can only offer that company’s minimums and pricing. If their floor is $10,000, that is your only option with them.

An independent broker is not tied to one carrier. They can match you to the company whose minimum face amount, underwriting, and price actually fit your cremation plan — whether that is a $2,000 policy or a larger one.

That freedom to shop across carriers is the core advantage of buying funeral insurance through a broker rather than calling one company off a television ad.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.