Home > Level vs. Graded vs. Modified Final Expense Insurance > Graded Benefit Final Expense Insurance

Graded Benefit Final Expense Insurance: How the Payout Schedule Works and Why You Were Placed Here

If you have been told you qualify for a graded benefit policy — or you expect to be placed there — this page explains exactly what that means for your coverage. Graded benefit is the middle tier of final expense insurance, sitting between level benefit, which pays the full amount from day one, and modified benefit, which is reserved for higher-risk applicants. The way a graded policy pays out is genuinely different from both, so this guide walks through what graded pays at claim time, the year-by-year payout schedule, how to spot plans that are mislabeled as graded, and why your health history may have placed you here. Graded benefit is a legitimate, useful form of coverage — not a consolation prize.

What Graded Benefit Actually Pays at Claim Time

Graded benefit is one of the three main ways a final expense insurance policy can be structured, alongside level benefit and modified benefit. The difference between them is not the coverage amount or the monthly premium alone. The real difference is what your beneficiary receives if you pass away in the first two years of the policy.

A graded plan pays a portion of the coverage amount during that early window, and the portion grows the longer the policy has been in force. This is what makes graded its own tier, and it is the structure this page walks through in detail.

The Contractual Definition of “Graded Benefit”

The word “graded” refers to a graduated payout. During the first year, only a portion of the benefit is paid; in the second year, a larger percentage is paid; and the full benefit is not paid until the policy clears its waiting period.

Most graded plans run on a two-year, or 24-month, schedule. A common and representative structure pays 30% of the coverage amount in year one, 70% in year two, and 100% from month 25 forward. So “graded benefit” simply means the death benefit steps up over the first 24 months instead of paying in full right away.

It is worth knowing up front that the exact percentages vary by company. It is common to see something like a 30% to 40% payout in the first year and 50% to 75% in the second year, with the full death benefit becoming payable after two years. The detailed schedule and carrier differences are covered further down the page.

Why Graded Benefit Exists as a Product Tier

Graded exists because most final expense applicants fall somewhere between perfect health and serious illness. Level plans are built for the healthiest applicants, while graded plans are aimed at people with moderate health issues that are not an immediate threat. Modified and guaranteed issue plans sit below graded, for more serious or multiple conditions.

Being placed in graded means the carrier reviewed your health and chose to accept the risk with a waiting period. It is not a partial denial, and it is not the carrier turning you away. Plan types are tools, not “better” or “worse” labels, and the best plan is the one you can qualify for and keep paying for comfortably.

For older applicants with a manageable but flagged health history, graded is often the natural landing spot. Conditions such as Parkinson’s, lupus, liver disease, or COPD are examples that might place an applicant into a graded plan rather than level. This is why graded is one of the most common placements in burial insurance for seniors who are mostly stable but have something on their record.

How Graded Benefit Compares to Level and Modified at Claim Time

The clearest way to see the difference is to look at one policy and one moment in time. Imagine a $10,000 funeral life insurance policy where the insured passes away in month 12 from natural causes. Each tier pays a very different amount.

| Plan type | Payout in month 12 (natural cause) on a $10,000 policy | How the first two years work |

|---|---|---|

| Level benefit | $10,000 | Full benefit from day one |

| Graded benefit | About $3,000 (30%) | Pays a growing percentage of the face amount |

| Modified benefit | About $400–$500 | Returns premiums paid plus interest, not a percentage of the face amount |

Level pays the full amount right away. Graded pays a portion during the waiting period, while a modified plan instead returns the premiums paid plus interest during the first two years before paying the full benefit in year three. The modified figure is small in year one because it is based on the handful of premiums paid so far, not on the coverage amount.

The important takeaway is that all three tiers end up in the same place. After the two-year waiting period clears, a graded policy pays the full death benefit for any cause of death — exactly like a level plan. The next section walks through that year-by-year schedule in detail.

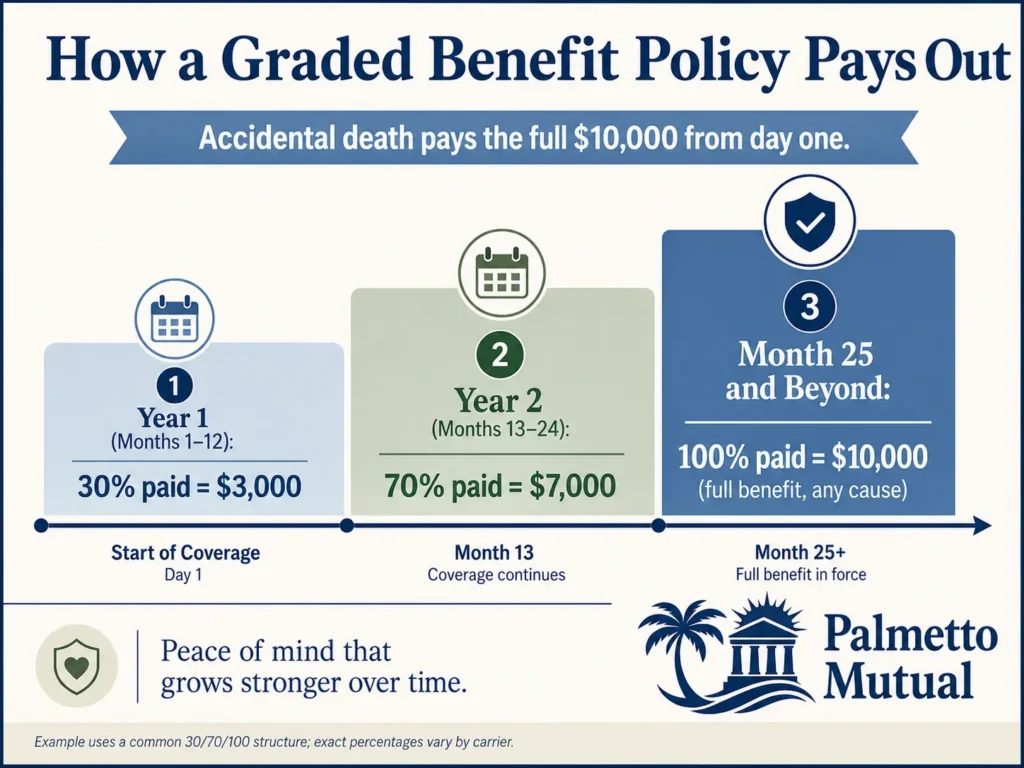

The Graded Payout Schedule: What Beneficiaries Receive in Years 1, 2, and 3

This is the heart of how a graded benefit policy works. The question every reader wants answered is simple: if I pass away at a given point, how much does my beneficiary actually get?

The schedule below uses the common 30/70/100 structure on a $10,000 policy so the dollar amounts are easy to follow. Your own policy may use slightly different percentages, which we cover at the end of this section.

| When death occurs (natural cause) | Percentage paid | Payout on a $10,000 policy |

|---|---|---|

| Months 1–12 (year one) | 30% | $3,000 |

| Months 13–24 (year two) | 70% | $7,000 |

| Month 25 and beyond | 100% | $10,000 |

| Any time, accidental death | 100% | $10,000 |

Year One: The 30% Payout Period

If death from natural causes happens in the first 12 months, most graded plans pay a fixed portion of the coverage amount. A common structure pays roughly 30% of the death benefit for a death in year one.

On a $10,000 burial insurance policy, that means the beneficiary receives about $3,000. The amount is the same whether death occurs in month 1, month 6, or month 11.

For most carriers, there is no further step-up inside year one. The 30% holds steady across the entire first 12 months, then the policy moves into the year-two tier on the first anniversary.

Year Two: The 70% Payout Period

Surviving past the first anniversary increases the payout meaningfully. For a non-accidental death in year two, a common structure pays 70% of the death benefit.

On that same $10,000 policy, the beneficiary would receive about $7,000. As with year one, the percentage is steady across the whole period, so death in month 13, month 18, or month 23 pays the same amount.

This jump from 30% to 70% is why the second year matters so much. The longer the policy stays in force, the closer the payout climbs to the full coverage amount.

Month 25 and Beyond: Full Benefit

Once the 24-month waiting period clears, the picture changes completely. After the graded period has passed, beneficiaries receive the full death benefit no matter the cause of death.

From month 25 forward, a graded policy pays out exactly like a level policy. Once the grading period ends, the policy functions like a standard contract and pays the full face amount regardless of the cause of death.

The contrast right at the line is sharp. A natural-cause death in month 23 pays $7,000 on a $10,000 policy, while the same death in month 25 pays the full $10,000. That is why keeping the policy active through the waiting period is the single most important thing a graded policyholder can do.

How Accidental Death Bypasses the Graded Schedule Entirely

The percentage schedule applies only to natural-cause deaths. Accidents are treated differently. An exception to most graded benefit limitations is death by accident, which qualifies for the full death benefit amount.

This means a fatal car crash, fall, or drowning in the first two years typically pays the full coverage amount right away. Accidental deaths are generally covered from day one across policy types.

One caution worth noting: “accident” is defined narrowly in the contract and excludes many causes, so the exact definition is worth confirming in the policy. Still, the general rule is dependable — the waiting period and its percentages apply to natural causes, not accidents.

Carrier Variation in the Payout Schedule

The 30/70/100 schedule is a representative example, not a universal rule. The exact percentages are set by each carrier and written into the policy contract. It is common to see a 30% to 40% payout in year one and a 50% to 75% payout in year two before the full benefit becomes payable after two years.

Other structures exist as well. One example pays 25% to 40% in the first year, 65% to 75% in the second year, and 100% in the third year and beyond. A few carriers also run longer schedules. One carrier, for instance, does not pay the full death benefit on its graded policy until the fourth year.

Because the schedule varies this much, the specific numbers matter when comparing offers. An independent broker can compare these payout structures across carriers and steer you toward the plans with the most favorable graded schedule for your situation.

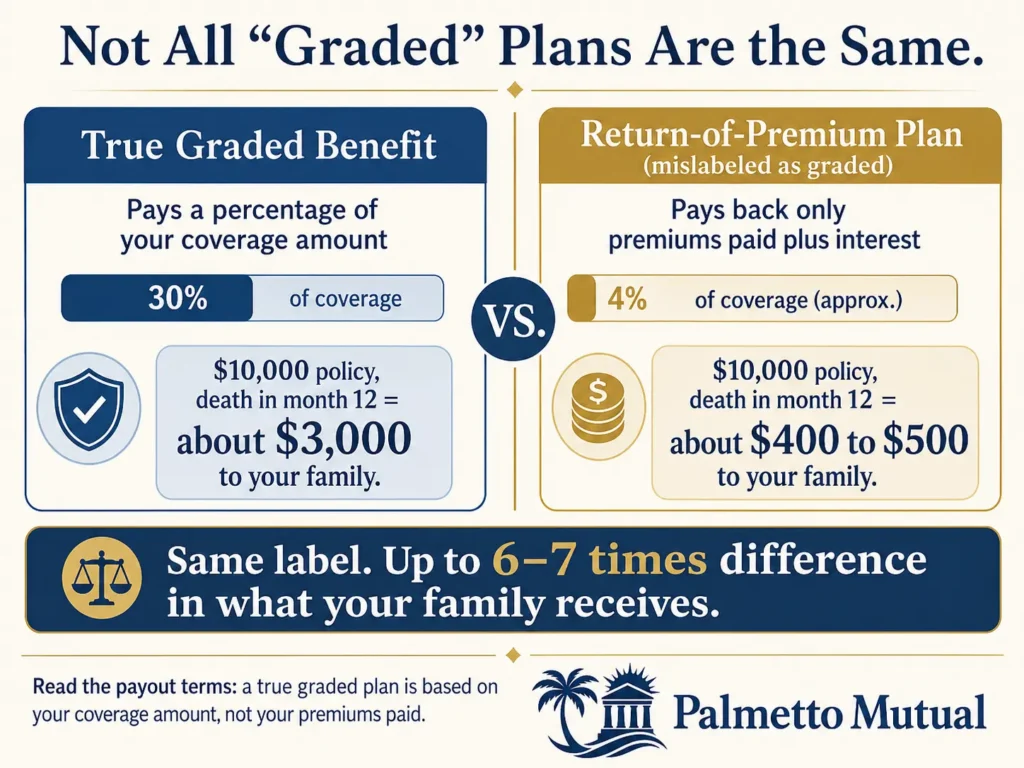

True Graded Benefit vs. Return-of-Premium Plans Mislabeled as Graded

This is one of the most important things to understand before you sign anything. The word “graded” gets used for two very different products, and the difference can mean thousands of dollars to your beneficiary.

A little care up front protects your family. This section shows you how to tell a true graded benefit plan from a return-of-premium plan wearing the same label.

The Two Different Structures Both Called “Graded”

A true graded benefit plan pays a percentage of the coverage amount during the waiting period. A 30/70/100 graded policy pays 30% of the face amount in the first year, 70% in the second year, and 100% after that for natural-cause deaths, while accidental death pays the full amount from day one.

A return-of-premium (ROP) plan works very differently. An ROP plan returns only the premiums paid so far plus a set interest rate if death occurs during the restricted period — for example, premiums plus 10% interest during the first two years.

The problem is that both get loosely called “graded.” But an ROP plan is structurally the same as a modified benefit plan, not a true graded plan. Modified plans return premiums plus a percentage during the two-year waiting period rather than paying a share of the face amount.

How to Identify a True Graded Benefit Policy

You identify the real thing by reading the payout structure, not the product name. Look for language in the quote or contract that lists a percentage of the coverage amount by year.

If the contract says something like “30% in year one, 70% in year two,” that is a true graded benefit plan. If it instead says “return of premium plus X% interest” during the waiting period, the plan is structurally modified, no matter what the brochure calls it.

A simple test helps here. Ask one question: during the waiting period, is the payout based on my coverage amount or on the premiums I have paid in? A funeral life insurance plan tied to the coverage amount is true graded; one tied to premiums paid is return-of-premium.

Why the Mislabeling Matters at Claim Time

The labels look similar, but the outcomes are not. Here is the same $10,000 policy with a natural-cause death in month 12 under each structure.

| Plan as written | What the beneficiary receives in month 12 |

|---|---|

| True graded benefit (30% year one) | About $3,000 |

| Return-of-premium plan called “graded” | About $400–$500 (premiums paid plus interest) |

The gap is large. A true graded plan pays a percentage of the face amount, while an ROP plan pays back only the cumulative premiums plus interest during the restricted period. On a low monthly premium, a year of payments plus interest is only a few hundred dollars.

That is roughly a six to seven times difference in what your family receives, driven entirely by which structure hides behind the word “graded.” This is why reading the payout terms is worth the few minutes it takes.

Carriers Known for True Graded Benefit Structures

Some carriers offer true percentage-based graded plans, while others sell return-of-premium plans under the graded label. One published agent review, for example, describes a carrier whose true graded program gives partial first-day coverage for hard-to-place conditions like Parkinson’s, certain kidney and liver issues, and COPD. That carrier’s graded program provides partial first-day coverage for neurological diseases such as Parkinson’s, kidney issues short of dialysis, liver issues like Hepatitis C, and COPD.

Because these product structures and the carriers offering them change over time, current specifics should be verified against active underwriting guides before being published.

This is one more reason an independent broker matters. A captive agent who represents a single company can only offer that company’s structure, even if it is a return-of-premium plan labeled as graded. An independent broker can compare true graded options across multiple carriers and match you to the structure that actually pays a percentage of your coverage.

Why You Were Placed in Graded Benefit: Conditions, Triggers, and Carrier Variation

If you were offered a graded plan, there is a specific reason rooted in how the carrier read your health history. Understanding that reason helps you decide whether to accept it or look further.

This section covers the conditions and events that most often lead to graded placement, how prescriptions factor in, and why the same person can be quoted differently by different companies.

Health Conditions That Most Often Trigger Graded Placement

Graded placement usually reflects a manageable but flagged condition — something that is stable now but raises the carrier’s risk. Conditions such as Parkinson’s, systemic lupus, liver disease, or COPD are examples that can place an applicant into a graded plan.

Other common graded-tier profiles include controlled congestive heart failure outside the most critical windows, COPD that does not require supplemental oxygen, and several chronic conditions managed together with multiple medications. For COPD, carriers weigh stage and severity, recent hospitalizations, and oxygen use, with oxygen use being a major dividing line that can push an applicant toward a graded or modified plan.

Diabetes can also land in graded when complications are present. Diabetic complications such as amputation, diabetic coma, or nephropathy within the past 12 to 24 months commonly require either graded coverage or guaranteed issue with a waiting period. Higher A1C readings and multiple managed conditions tend to point the same direction.

Recent Medical Events That Push Level-Eligible Applicants to Graded

Timing is often the deciding factor. The same event can be a level disqualifier at one carrier and acceptable history at another, depending on how far back each company looks. Carriers set look-back periods for major events such as cancer, COPD, kidney failure, or congestive heart failure, and they adjust these underwriting rules frequently.

A heart attack, stroke, or cancer treatment that falls just inside a carrier’s look-back window can move you from level to graded. One carrier, for example, uses a two-year look-back on heart events such as heart attacks and strokes.

This is why the gap between a 12-month and a 24-month look-back matters so much. A hospitalization 18 months ago might be invisible to a carrier with a 12-month window but disqualifying for level at a carrier with a 24-month window.

Medication Combinations That Flag Graded Placement

Carriers do not rely only on what you write on the application. Underwriting typically includes a prescription drug check and a review of medical information through the MIB to confirm that application answers match the database.

Certain prescription combinations signal a more serious underlying picture than any single drug. Insulin combined with cardiac medications, several psychiatric medications taken together, or blood thinners paired with other cardiovascular drugs can all flag graded placement.

The key point is that the prescription database reveals these patterns even if a condition was not listed on the application. The combination often carries more weight in the decision than any one medication on its own.

How Different Carriers Treat the Same Health Profile

The same applicant can get different answers from different companies. One carrier treats insulin use on its own as level-eligible but moves diabetes with complications to modified, while another company may weigh the same facts differently.

Consider someone with controlled COPD and Type 2 diabetes. One carrier with stricter rules on combined respiratory and metabolic conditions might place that person in graded, while a carrier that evaluates the two conditions more independently might offer level. Because each carrier has its own underwriting rules, applying with a single company and accepting its graded offer often leaves better options unexplored.

The takeaway is that a graded offer reflects one carrier’s rules, not the whole market.

When to Accept Graded Placement and When to Shop Other Carriers

A graded offer from one company does not mean graded is your only option everywhere. The primary remedy is simple: compare your health profile across multiple carriers before settling. Many people accept the first graded offer or decline they receive and assume it is the best available, when shopping other carriers often opens up better options.

Graded is genuinely the right answer in some cases. When several carriers all return graded for the same profile, that is a strong signal it reflects the real market for your health, and graded burial insurance is still meaningful, valuable coverage.

It is worth pushing for a second opinion when only one company has reviewed your file. It is wise to ask whether you qualify for a level or graded plan first, since settling unnecessarily for a more restrictive plan means overpaying every month. An independent broker can run that comparison for you in a single conversation.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.