Home > Level vs. Graded vs. Modified Final Expense Insurance

Level vs. Graded vs. Modified Final Expense Insurance: How the Three Tiers Compare

If you have been comparing final expense insurance, you have likely run into three terms: level, graded, and modified. The difference between them comes down to two things — how soon the policy pays out the full death benefit, and how much you pay in premiums. Which tier you land in is not random; it is based on your health. This guide walks through who fits each tier, what each one pays, and how to find the best tier available to you across different carriers.

Side-by-Side Payout Comparison: First 24 Months Across All Three Tiers

When people compare final expense insurance, the first thing they want to see is simple: if I pass away, what does my family actually receive — and when? That answer depends on which tier you are placed in. Below is the payout picture for level, graded, and modified across the first two years and beyond.

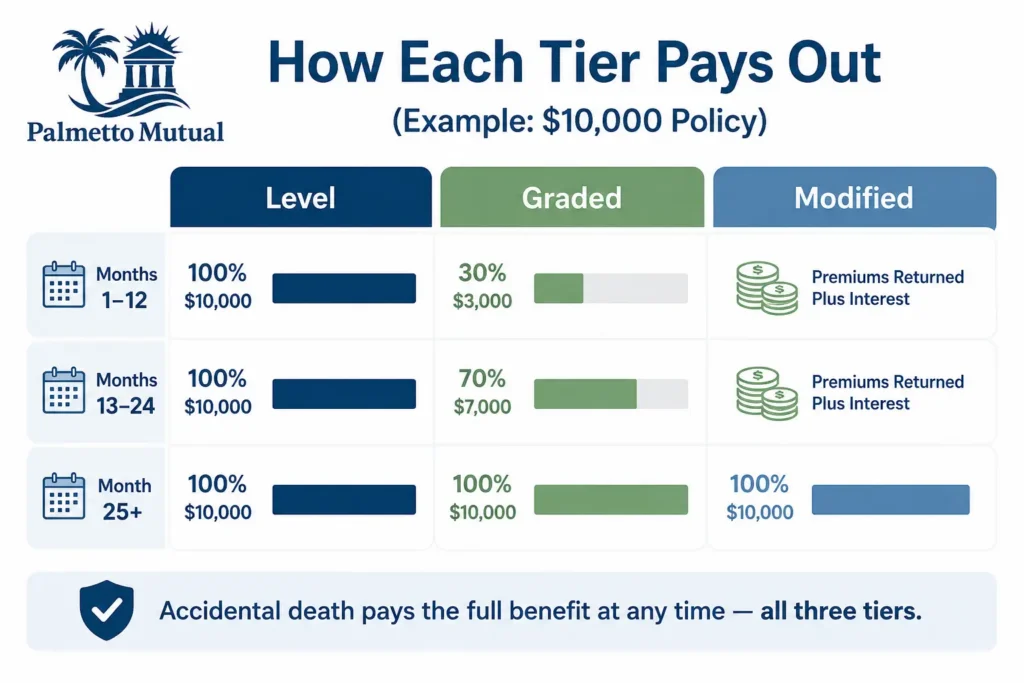

The Payout Comparison Table

The table shows what a beneficiary receives for a natural (non-accidental) death at three points in time. The accidental death column is separate because it works differently, which the next section explains.

A few things to keep in mind when reading this table.

Level benefit pays the full amount from day one, no matter the cause of death.

Graded benefit uses a partial payout during the first two years. The 30% / 70% / 100% pattern is the most common example, but it is not universal. Some carriers pay closer to 30–40% in year one and 50–75% in year two before the full benefit applies after two years. Always confirm the exact percentages with the specific carrier.

Modified benefit does not pay a percentage of the death benefit during the waiting period. Instead, it returns the premiums you paid plus interest — often around 10% — if death occurs within the roughly 24-month window. After the waiting period, it pays the full benefit.

How to Read the Comparison Table

The easiest way to see the difference is to run the same policy through each tier. Picture a $10,000 policy and three different death-month scenarios.

Say the person passes away in month 6 from natural causes. Under a level policy, the beneficiary receives the full $10,000. Under a graded policy, they receive about 30%, or roughly $3,000. Under a modified policy, they receive the premiums paid back plus interest — not a percentage of the $10,000.

Now say the person passes away in month 18, still from natural causes. The level policy still pays the full $10,000. The graded policy now pays about 70%, or roughly $7,000. The modified policy still returns premiums plus interest, since it has no partial-payout step.

Finally, say the person passes away in month 30. By this point all three tiers behave the same way: each pays the full $10,000, because the waiting period is over.

There is one important exception that applies no matter which tier you are in. If the death is accidental — not from natural causes — the full $10,000 is paid right away, even during the waiting period. That holds true across all three tiers. The next section explains why this structure exists in the first place.

Why Final Expense Has Three Tiers and How Waiting Periods Define Each One

To understand why level, graded, and modified exist, it helps to step back and look at what burial insurance was built to do. The three tiers are not arbitrary labels — they are how carriers offer coverage to people across a wide range of health situations while keeping the product affordable and available.

Why the Three-Tier System Exists

Traditional whole life insurance usually requires a medical exam and full underwriting. People with significant health conditions are often charged much more or turned down completely.

Final expense insurance was designed to fill that gap. It skips the medical exam, relying instead on a short health questionnaire and, in many cases, public database checks like prescription and motor vehicle records. This makes coverage reachable for older adults and people with health issues that traditional policies reject.

The three-tier system is how carriers manage the added risk of insuring people without an exam. Healthier applicants who pass the health questions qualify for the lowest-cost coverage with no waiting period, because the insurer sees a lower chance of an early claim. Applicants with more serious or recent health events are still offered coverage, but at a higher cost and with a delayed full payout. In short: better health earns better terms, and the tiers protect riskier applicants instead of declining them.

What a Waiting Period Actually Is

A waiting period is the time between when your policy starts and when your beneficiary becomes eligible for the full death benefit. During that window, a natural-cause death pays out differently depending on your tier.

Carriers use waiting periods to protect against what the industry calls anti-selection (sometimes called adverse selection). Without health screening, someone with a severe or terminal condition could otherwise buy coverage right before death and have a full benefit paid almost immediately. The waiting period prevents that, which keeps the product sustainable and affordable for everyone else.

Each tier handles the waiting period differently. Level has no waiting period at all — full coverage starts on day one. Graded uses a partial waiting period, paying a portion of the benefit if death occurs in the first two years. Modified uses a return-of-premium waiting period, paying back the premiums you paid plus interest if death occurs during that window.

The Accidental Death Exception (Universal Across All Three Tiers)

There is one situation where the waiting period does not apply at all: accidental death. This covers things like car accidents, falls, and drownings.

If death is accidental, the full death benefit is paid out immediately — even during a graded or modified waiting period. This protection works the same way across all three tiers.

This is one of the most misunderstood parts of funeral insurance. Many people assume that a waiting period means no real coverage for the first two years, but that is not true for accidents. The waiting period only limits payouts for natural-cause deaths; an accidental death is covered in full from the start, no matter which tier you are in.

Who Qualifies for Level Benefit (And Why It’s the Tier to Aim For)

Level benefit is the tier most people hope to land in, and the good news is that more applicants qualify for it than expect to. With burial insurance, level coverage means your family gets the full death benefit from the very first day. This section covers who typically qualifies and what level pays.

The Health Profile That Lands You in Level Benefit

Level benefit is built for people whose health is stable, even if it isn’t perfect. Common conditions like high blood pressure, high cholesterol, controlled Type 2 diabetes, and sleep apnea are seen by insurers every day and often still qualify for first-day coverage when they are stable and under treatment.

Chronic conditions are usually fine as long as they are managed. Diabetes on its own is generally not a tier-determining condition; most diabetic applicants — including many who are insulin-dependent — qualify for level day-one coverage at the right carrier. Even controlled respiratory conditions like mild COPD without oxygen use can sometimes qualify for immediate level coverage.

What level benefit generally requires is the absence of recent major health events. The typical level applicant has:

- No heart attack, stroke, or cancer treatment within the carrier’s lookback window (often the past 24 months)

- No terminal diagnosis

- No current hospice or nursing home care

- Chronic conditions that are controlled and stable, not recently worsening

In practice, immediate coverage is often available even with pre-existing conditions if your diabetes is well-managed or a heart attack happened more than 24 months ago. The exact line depends on the carrier, which is why two people with similar health can get different answers.

What Level Benefit Pays and Costs

Level benefit is the simplest tier to understand. It pays the full death benefit from day one, for both natural and accidental death, with no waiting period.

It also carries the lowest premiums of the three tiers. Simplified-issue level coverage costs the least precisely because the insurer sees a lower chance of an early claim. The exact monthly rate depends on your age, your health profile, the coverage amount, and the carrier.

For live pricing tied to your specific situation, use the quoting tool at the top of this page rather than a general estimate. For a full breakdown of level benefit plans, see the dedicated level benefit guide linked below.

Who Lands in Graded Benefit (And Why It’s Not a Bad Outcome)

If your health history includes a more recent or more serious event, you may be placed in graded benefit rather than level. This is not a bad outcome — graded final expense insurance still provides real, permanent coverage, with a partial payout structure during the first two years that becomes a full benefit after that. This section covers who typically lands here and what graded pays.

The Health Profile That Lands You in Graded Benefit

Graded benefit is generally offered to applicants with moderate health complications — often a diagnosis or hospitalization that is still inside the carrier’s lookback window, or a “yes” to one of the application’s middle-tier health questions.

A few conditions commonly steer an applicant toward graded. Carriers vary, but conditions such as Parkinson’s disease, systemic lupus, liver disease, or COPD may place an applicant in a graded plan. Many carriers route applicants to graded when a “yes” appears on questions covering neurological conditions like multiple sclerosis or Parkinson’s, or lung impairments like COPD, chronic bronchitis, and emphysema.

Timing matters as much as the condition itself. At some carriers, conditions like COPD are graded if diagnosed or treated within the past two to three years, but can move up to immediate coverage once they fall outside that window.

One honest caveat on the outline’s example list: congestive heart failure is treated more harshly than the other conditions here. At many carriers, a congestive heart failure diagnosis is a knockout question that disqualifies an applicant from both level and graded coverage, pushing them toward modified or guaranteed issue. So while some carriers may consider it, CHF is better described as carrier-dependent and often more restrictive than COPD or Parkinson’s, not a reliable graded fit.

What Graded Benefit Pays and Costs

Graded benefit uses a partial payout during the roughly 24-month waiting period, then pays the full death benefit after that. A common pattern is around 30% in year one and 70% in year two before full benefits apply, though the exact percentages vary by carrier. Accidental death pays the full benefit at any time, as covered earlier.

On price, graded sits in the middle of the three tiers — higher than level, lower than modified. The added cost reflects the higher risk the carrier takes on during the waiting period.

As with level, your real rate depends on age, coverage amount, and carrier, so the quoting tool at the top of the page is the most accurate source for pricing. The graded benefit spoke page below covers the structure in more depth.

Who Gets Placed in Modified Benefit (And When It Still Makes Sense)

Modified benefit is the tier for applicants whose health history includes a recent, serious event. It carries the longest effective wait for a full payout and the highest premiums, but it serves an important purpose: it gives coverage to people who would otherwise be declined. For many, modified burial insurance is the difference between having a policy and having nothing.

The Health Profile That Lands You in Modified Benefit

Modified benefit is generally offered after a recent, significant health event — the kind that falls inside a carrier’s most restrictive lookback questions. Conditions that commonly place an applicant into a modified plan include stroke, angina, aneurysm, and cancer.

The most common path to modified is a serious event within roughly the past two years. The typical modified applicant has one or more of:

- A heart attack, stroke, or cancer treatment within the past 24 months

- Insulin-dependent diabetes paired with complications

- Other high-risk markers a carrier treats as a knockout for level and graded

Cancer history depends heavily on the type, stage, treatment, and how long someone has been cancer-free; recent treatment often points to graded or guaranteed issue rather than level. The same logic applies to recent cardiac and neurological events.

It helps to think of modified as a safety-net tier rather than a penalty. When someone truly cannot pass the health questions because of severe or recent medical issues, the waiting-period option at least guarantees they can still get coverage instead of being declined altogether.

What Modified Benefit Pays and Costs

Modified benefit does not pay a percentage of the death benefit during the waiting period. Instead, if a non-accidental death occurs in the first two years, the policy returns the premiums paid plus a percentage — commonly around 10% in year one and 20% in year two — then pays the full benefit from year three onward. Accidental death pays the full benefit at any time.

Modified premiums are the highest of the three tiers. The carrier is taking on the most risk, so it charges the most for the same coverage amount.

Because modified pricing varies widely by carrier, the quoting tool at the top of the page is the most reliable way to see your actual rate. The modified benefit spoke page below covers the structure and the trade-offs in more detail.

Why the Same Person Gets Different Tiers from Different Carriers (And What It Costs You)

Here is the part most people never hear: your tier is not a fixed fact about you. The very same health history can land you in level at one company, graded at another, and a decline at a third. With final expense insurance, the tier you end up in often says more about which carrier reviewed your application than about your actual health.

How Underwriting Differs From Carrier to Carrier

Every carrier writes its own underwriting rules. Each sets its own health questions, its own lookback windows, and its own list of knockout conditions.

That is why the same condition gets different treatment depending on where you apply. At one carrier, COPD is a graded condition if treated within the past two to three years; at another, the same condition outside that window may qualify for immediate coverage. Some carriers will issue an immediate, level policy for a condition like COPD without oxygen use that other carriers would only cover with a graded plan, or decline outright.

Carriers also pull from your prescription history and other databases, so two companies can read the same medication list and reach different conclusions. The result is that your tier is really a measure of how a specific carrier’s rules score your specific profile.

A Real-World Example of Tier Variation Across Carriers

Picture a 67-year-old who had a heart attack 30 months ago and now has well-controlled Type 2 diabetes. Their tier depends entirely on each carrier’s cardiac lookback window.

A carrier with a 36-month cardiac lookback still counts that heart attack, because 30 months falls inside the window. That applicant gets placed in graded.

A carrier with a 24-month cardiac lookback no longer counts the same heart attack, because 30 months is now outside the window. That same applicant can qualify for level — full coverage from day one. Carrier underwriting questions routinely use a defined window, such as “during the past 24 months,” for events like heart attack, stroke, and TIA, so a few months can flip the entire result. Nothing about the applicant changed — only the ruler they were measured against.

The Financial Cost of Being Placed in the Wrong Tier

Being placed in a higher tier than necessary costs money in two ways. The first is premium.

Modified premiums run well above level for the same coverage. If a level placement runs, say, $60 a month and a modified placement on the same $10,000 policy runs $95, that $35 monthly gap is about $420 a year — and over 12 to 15 years of payments, roughly $5,000 to $7,500 in extra premium for coverage you may have qualified to get more cheaply.

The second cost is the payout itself. If a death occurs during a waiting period — for example, in month 18 of a graded plan — the family has to bridge the gap between the limited payout and the actual cost of the funeral. Sitting in a waiting period you did not need means your beneficiary could receive far less than the full benefit if a claim happens early.

Put together, a wrong-tier placement can mean thousands in extra premium and a smaller payout when it matters most. That is the real price of applying to the wrong carrier.

Why Captive Agents Can’t Solve This (And Independent Brokers Can)

This is where the type of agent you work with makes a direct financial difference. A captive agent represents a single carrier and can only offer that one company’s underwriting result. If their carrier puts you in graded or modified, that is the only answer they can give you — even if a different carrier would have offered level.

An independent broker works the other way. An independent broker compares multiple carriers and targets the companies whose underwriting guidelines best fit your profile, which matters most when you have a medical history, take several medications, are older, or have been declined before. The most expensive mistake seniors make is applying to the wrong carrier for their health profile, and working with an independent agent who knows senior underwriting across multiple carriers is the most practical way to avoid it.

The takeaway is simple. The only way to know your true best tier is to have your case shopped across several carriers and measured against each one’s rules. That is exactly what working with an independent broker like Palmetto Mutual provides — one application reviewed against many carriers, so you land in the best tier actually available to you.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.