Home > Level vs. Graded vs. Modified Final Expense Insurance > Modified Benefit Final Expense Insurance

Modified Benefit Final Expense Insurance: How the Waiting Period Works and Why You Were Placed Here

If you have been told you qualify for a modified benefit policy, you may be wondering what that means for you and your family. Modified benefit is the most restrictive tier of final expense insurance, built for people whose health history would otherwise lead to a decline. This guide explains what a modified policy pays during the waiting period, how the 24-month return-of-premium feature works, how modified differs from guaranteed issue, and why you were placed in this tier instead of a higher one. Modified benefit is a real safety-net option, not a trap, and the sections below walk through exactly what you are getting.

What Modified Benefit Actually Pays at Claim Time

Modified benefit is one of three waiting-period tiers in final expense insurance, and it is the most restrictive of the three. To understand what your policy will do for your family, the first thing to know is what “modified benefit” actually means when a claim is filed.

The Contractual Definition of “Modified Benefit”

The word “modified” describes a modified payout during the waiting period, not a different kind of policy. A modified benefit policy is still a small whole life insurance policy. What changes is how the death benefit is paid if you die in the first two years.

If death occurs during the waiting period from natural causes, the carrier does not pay the face amount. Instead, it returns the premiums you paid into the policy, plus a stated amount of interest. Many carriers pay roughly 10% in the first year and around 20% in the second year on the premiums paid in, though the exact figure varies by carrier.

After the waiting period ends, the policy pays the full face amount for any cause of death. So “modified” is about timing, not a watered-down product.

Why Modified Benefit Exists as a Product Tier

Modified is the carrier’s safety-net tier. It exists for applicants whose recent health events or current health would otherwise lead to a decline at most carriers.

Think of it as the carrier finding a way to say yes. The two-year waiting period is the carrier’s protection against insuring someone who applies only because they expect to pass away soon, which is sometimes called anti-selection.

If you were placed in modified, it means the carrier accepted your risk despite serious health concerns. You were not turned away. You were offered the tier built for exactly your situation.

How Modified Benefit Compares to Level and Graded at Claim Time

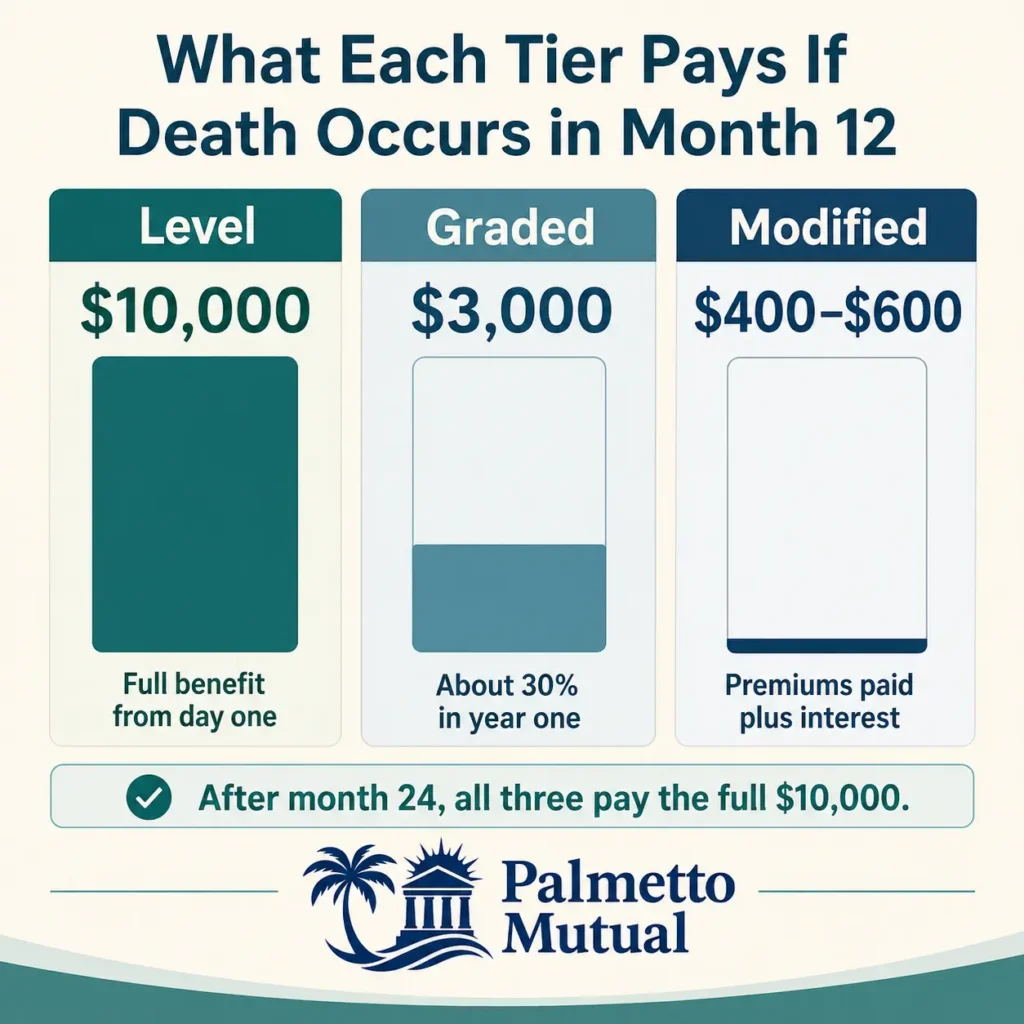

The three tiers differ most during the first two years. After that, they all pay the same thing. Here is how a $10,000 policy would pay if death from natural causes happened in month 12.

| Tier | What it pays in month 12 | What it pays after month 24 |

|---|---|---|

| Level | Full $10,000 from day one | Full $10,000 |

| Graded | A percentage of the face amount (often around 30% in year one), roughly $3,000 | Full $10,000 |

| Modified | Premiums paid plus interest, often $400 to $600 | Full $10,000 |

Modified clearly pays the smallest amount during the waiting period. But notice the right-hand column: all three tiers reach the full benefit once the waiting period is over. The next section walks through exactly how the modified payout is calculated month by month.

The 24-Month Return-of-Premium Mechanic: How Your Family Gets Paid During the Waiting Period

The return-of-premium feature is the heart of a modified policy. This section shows the math with real dollar amounts so you can see what your family would receive at any point in the first two years.

How the Return-of-Premium Calculation Works

The carrier keeps a running total of every premium you pay from the day the policy starts. If you die during the waiting period from natural causes, that running total is returned to your beneficiary, plus interest.

Here is a simple example. Say you have a $10,000 policy that costs $80 a month. After 12 months you have paid $80 × 12, which is $960.

With interest of about 10% on those premiums, your beneficiary would receive roughly $1,056 if death occurred at the 12-month mark. Some carriers step the interest up in the second year, so a death later in the waiting period returns more.

Why Modified Premiums Are the Highest of the Three Tiers

A modified policy costs more per month than a level or graded policy at the same coverage amount. The reason is risk.

The carrier is accepting an applicant with serious health concerns, so it charges more to balance that risk. The higher premium is the price of guaranteed acceptance into a tier that would otherwise be a decline.

So the trade-off is straightforward. You pay more each month, and in return you get into a policy that protects your family once the waiting period passes.

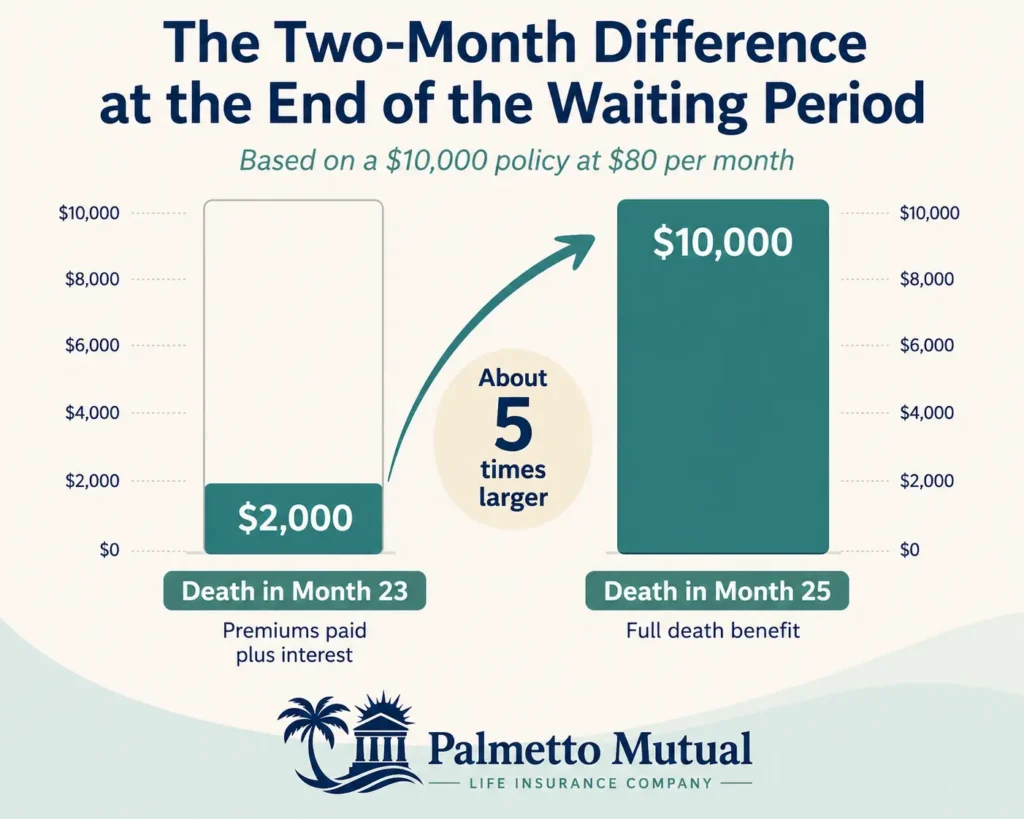

The Cliff Edge: What Happens at Month 25

The end of the waiting period is the single biggest financial moment in a modified policy. The difference between dying just before it and just after it is dramatic.

Imagine the same $10,000 policy at $80 a month. Here is what your beneficiary receives depending on timing.

| When death occurs (natural causes) | What the beneficiary receives |

|---|---|

| Month 23 | Premiums paid plus interest, roughly $2,000 |

| Month 25 | The full $10,000 |

A two-month difference produces about a 5x change in the payout. That is why outlasting the 24-month waiting period is the central goal of owning a modified policy.

How Accidental Death Bypasses the Waiting Period Entirely

There is one important exception. If death is caused by an accident, such as a car crash, a fall, or a drowning, the policy pays the full face amount right away, even during the waiting period.

This holds true across all three tiers. For a modified policyholder, it means the full coverage amount is effectively in force from day one for any non-natural cause of death.

So while the waiting period applies to natural causes, your family is fully protected against accidents the moment the policy starts.

Carrier Variation in Interest Rates and Waiting Period Length

Not every carrier handles modified the same way. The interest rate and even the length of the waiting period can differ.

Most carriers pay around 10% interest on returned premiums, but some pay less, around 7% to 8%, and a few pay more. The waiting period is usually 24 months, but some carriers use a three-year structure on modified plans.

These differences matter, and they are part of why working with an independent broker helps. A broker can compare carriers and identify which offers the most favorable modified terms for your specific situation.

Modified Benefit vs. Guaranteed Issue: Why the Two Products Are Often Confused

Modified benefit and guaranteed issue are easy to mix up. They can pay your family almost the same way during the waiting period, yet they are not the same product. This section clears up the confusion so you know which one you actually have.

A Quick Note on Graded vs. Modified for Readers Who Landed Here Confused

Some readers arrive here looking for a graded versus modified comparison. If that is you, here is the short version.

Graded and modified are both waiting-period tiers of final expense insurance, but they pay differently during those first two years. Graded pays a percentage of the face amount, while modified returns your premiums plus interest.

If you want the full graded breakdown, see our graded benefit guide [internal link: graded benefit spoke page]. From here on, this section focuses on a different comparison: modified benefit versus guaranteed issue.

The Two Products That Look Similar at Claim Time

Modified and guaranteed issue often pay the same way during the waiting period. Both commonly return premiums plus interest if death from natural causes happens in the first two years.

Both are also aimed at people with significant health concerns, and both tend to cost more than level or graded plans. So at claim time during those first two years, the two can look nearly identical.

That overlap is exactly why agents and buyers sometimes treat them as the same thing. The real difference shows up earlier, at the application stage.

The Critical Difference Is in Enrollment, Not Payout

The true difference is how you get in. Modified is something you are placed into; guaranteed issue is something you choose.

A modified benefit policy goes through full simplified-issue underwriting. You answer detailed health questions, and the carrier checks prescription databases and the Medical Information Bureau before deciding where you land. Modified is the result of that review.

Guaranteed issue asks no health questions at all. As long as you fall inside the carrier’s age range, you are accepted automatically. In short: modified is where your health places you, while guaranteed issue is where you go when you already know your health will not pass underwriting.

Not Every Carrier Offers Guaranteed Issue

Here is a market detail many buyers miss. Most final expense carriers offer the three underwritten tiers, level, graded, and modified, as their standard lineup.

But guaranteed issue is a separate product line, and not every carrier sells it. Some companies only offer underwritten policies.

That means guaranteed issue is not always sitting there as a ready alternative to modified. It depends entirely on which carriers you are shopping. This is one place an independent broker earns their keep, by knowing which carriers in your market actually offer guaranteed issue.

When Guaranteed Issue Is the Right Choice Over Modified

Guaranteed issue makes sense in specific situations. The clearest one is when your health is serious enough that you would likely be declined even during modified underwriting.

Profiles like a terminal diagnosis, a very recent serious health event, or current hospice care can push you past what modified will accept. In those cases, guaranteed issue may be the only door still open.

There is also a simpler reason some people choose it. If you could pass modified underwriting but would rather skip the health questions for privacy or convenience, guaranteed issue is still a valid path, you just typically pay more for that no-questions acceptance.

Why You Were Placed in Modified Benefit: Conditions, Triggers, and Carrier Variation

If you landed in modified, there is a reason tied to your health history. Understanding that reason helps you see whether a different carrier might treat you differently, and whether the policy is worth buying. This is the most practical section of the guide on final expense and burial insurance placement.

Health Events That Trigger Modified Placement

Modified is usually triggered by recent or serious health events. These are the conditions that most often move an applicant out of level or graded and into modified.

Common modified-tier triggers include:

- A recent stroke or heart attack, often within the carrier’s critical window of roughly 12 to 24 months

- Active cancer treatment or a recent cancer diagnosis

- Dialysis or end-stage kidney disease

- Insulin-dependent diabetes with significant complications

- A recent major surgery

- Current oxygen use for COPD

If you recognize your own situation here, that is likely the reason for your placement. The common thread is that these events are recent or ongoing.

Medication Combinations That Flag Modified Placement

Your prescriptions can place you in modified on their own, even apart from how you answer the health questions. Carriers check prescription databases, and certain combinations point clearly to a serious condition.

Examples that tend to flag modified placement:

- Insulin combined with several cardiac medications

- Cancer treatment drugs combined with immunosuppressants

- Multiple medications that together signal an advanced chronic illness

When the medication picture points to a high-risk condition, that can drive placement automatically, regardless of the answers on the application. The database often tells the underwriter more than the questionnaire does.

How the MIB and Recent Medical Records Affect Placement

Two more sources shape where you land: the Medical Information Bureau and your recent medical history. The MIB is a shared industry database that stores coded flags from prior insurance applications.

It does not hold your full medical chart. It holds short codes that signal to other member carriers that something earlier was significant enough to record, which can surface a health event you did not mention.

Recent records carry the most weight, usually the last 24 to 36 months. That is because the underwriter is specifically checking whether your recent events fall inside the carrier’s critical lookback windows. The more recent the event, the more it affects placement.

How Different Carriers Treat the Same Modified-Tier Profile

The same health profile does not always produce the same result. Carriers set their own lookback windows, so one company’s modified can be another company’s graded.

Take a heart attack that happened 22 months ago. A carrier with a 24-month cardiac lookback would place that applicant in modified, while a carrier with an 18-month lookback might offer graded for the exact same history. The number of years carriers look back typically ranges from 2 to 5, depending on the condition.

The takeaway is simple. Being placed in modified at one carrier does not mean modified is your only option across the whole market.

When Modified Is Still the Right Choice (And When It Isn’t)

Modified is not automatically good or bad. It depends on your situation, and you deserve a straight answer either way.

Modified is often the right choice when:

- You have been declined, or would likely be declined, at several carriers

- You need guaranteed acceptance and are willing to pay more for it

- You expect to outlast the 24-month waiting period and want the long-term value of a whole life policy that stays in force

Modified may not be the right choice when:

- You could qualify for graded or level at a different carrier and the case has not been shopped around

- Your life expectancy is severely limited, which makes a return-of-premium-only payout the most likely outcome

- You could realistically set aside the same amount of money in dedicated savings instead

If your case has not been shopped across multiple carriers, that is worth doing before you accept modified, because the lookback differences above can change your tier. An independent broker can run your profile across carriers to confirm whether modified is truly your best available option.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.