Home > North Carolina

Final Expense Insurance in North Carolina — Coverage for Families From the Mountains to the Outer Banks

North Carolina stretches from the Blue Ridge Mountains through the Piedmont’s manufacturing and banking hubs out to the Coastal Plain and Outer Banks, and each region brings its own patterns to end-of-life planning. With more than 1.8 million residents over the age of 65 — concentrated in retirement destinations like Asheville, the Research Triangle, and the coast — final expense insurance is a common way North Carolina seniors cover funeral costs, cremation services, and outstanding bills without leaving the burden to family. This page walks through statewide funeral costs, how North Carolina regulates small whole life policies, the state’s burial and cremation laws, and the regions and counties we serve across the Tar Heel State.

Funeral and Cremation Costs in North Carolina

Funeral costs in North Carolina are slightly below the national median, but prices can change a lot depending on where a family lives and what type of service they choose.

Metro areas like Charlotte, Raleigh, Durham, and Cary usually cost more than the state average because of higher real estate, labor, and cemetery costs. Rural counties across the Mountains, Piedmont, and Coastal Plain often come in lower, although smaller markets may have fewer funeral homes to compare.

The figures below give North Carolina families a statewide baseline before they shop local funeral homes, cremation providers, and cemeteries.

Statewide Averages

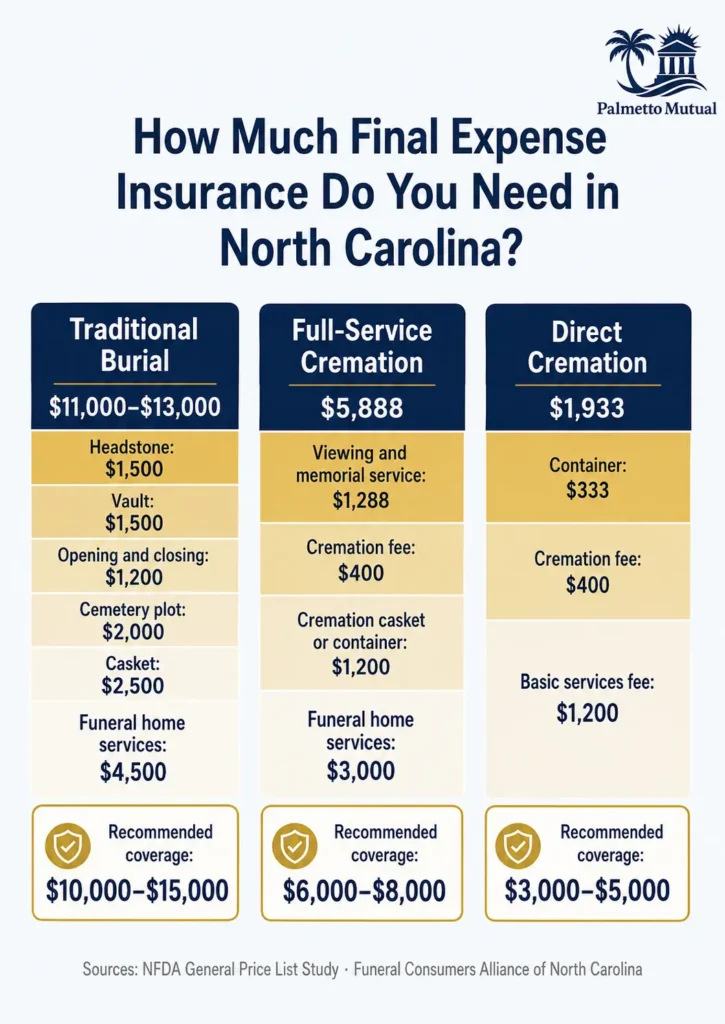

North Carolina’s funeral cost landscape generally breaks down into five common service types. Pricing data below is drawn from the National Funeral Directors Association, the Funeral Consumers Alliance of North Carolina, and aggregated state price surveys.

| Service Type | North Carolina Average |

|---|---|

| Traditional full-service funeral with burial | $8,136 |

| Full-service cremation with viewing | $5,888 |

| Cremation with memorial service | $2,600 – $5,000 |

| Direct cremation | $1,933, with some discount providers as low as $995 |

| Immediate burial / direct burial | $4,840 and up |

These figures do not include cemetery costs. In most North Carolina cemeteries, a burial plot, opening and closing fees, vault, and headstone can add another $3,000 to $6,000.

Urban cemeteries in Charlotte and Raleigh-Durham often run higher than rural cemeteries, especially when land availability is limited.

Regional Cost Variation

North Carolina’s geography creates real pricing differences between the Piedmont, Coastal Plain, Mountains, and major metro areas. The table below reflects typical traditional funeral pricing by metro, based on 2026 state cost surveys.

| Region | Representative Metro | Traditional Funeral From |

|---|---|---|

| Piedmont / Triangle | Raleigh | $7,547 |

| Piedmont / Triangle | Cary | $7,855 |

| Piedmont / Charlotte Metro | Charlotte | $7,393 |

| Piedmont / Triad | Greensboro | $6,854 |

| Piedmont / Triad | Winston-Salem | $6,777 |

| Coastal Plain | Wilmington | $7,316 |

| Coastal Plain | Fayetteville | $6,700 |

| Mountains | Asheville | $7,162 |

Charlotte and Raleigh-Durham consistently price about 10% to 15% above the state average. Higher overhead, staffing costs, and cemetery land costs all push prices upward in these larger markets.

Triad cities like Greensboro, Winston-Salem, and High Point usually come in at or slightly below the state average.

The Mountains and rural Coastal Plain are often 10% to 20% below major metro pricing, although families in smaller counties may have fewer providers to choose from.

How North Carolina Compares Nationally

The National Funeral Directors Association lists North Carolina’s average funeral with burial at $8,023, placing the state in the middle of the South Atlantic region alongside Georgia, Florida, and Virginia.

That is about $275 below the 2023 national median of $8,300.

North Carolina’s cremation rate is about 51%, which is still below the national rate of 63%. However, cremation continues to grow as more families look for affordable and flexible funeral options.

What Drives Cost in North Carolina

Several state-specific factors affect funeral and cremation costs in North Carolina.

Metro density. Charlotte, Raleigh, Durham, and Cary tend to have higher funeral home overhead, staffing expenses, and cemetery land costs than smaller Piedmont and mountain markets.

Rural-urban pricing gaps. North Carolina has 100 counties, many of them small and rural. In some areas, one funeral home may serve most of the county, which can limit competitive pricing pressure.

Aquamation access. North Carolina is one of the more progressive states for water cremation. Providers in Hillsborough, Shelby, and Wilmington offer aquamation services from about $1,295 to $3,500.

Veterans benefits. Salisbury National Cemetery and state veterans cemeteries in Spring Lake, Jacksonville, and Black Mountain can provide free burial for eligible veterans. This can be a major cost offset for military families and retirees near Fort Liberty and Camp Lejeune.

For most North Carolina families, a $10,000 to $15,000 final expense insurance policy can help cover a traditional funeral and cemetery costs in their region.

A smaller $5,000 to $8,000 final expense policy may be enough for full-service cremation, direct cremation, or cremation with a memorial service.l and cemetery costs in their region. A smaller $5,000 to $8,000 policy typically covers a full-service cremation or direct cremation with a memorial service.

Final Expense Insurance Regulations in North Carolina

Final expense insurance in North Carolina is regulated under the same state laws that govern life insurance. These rules protect seniors before they apply, after the policy is issued, and when a family files a death claim.

Most final expense and burial insurance policies are small whole life policies, so several North Carolina rules apply directly to the type of coverage seniors commonly buy.

The North Carolina Department of Insurance

The North Carolina Department of Insurance, often called the NCDOI, oversees life insurance companies and agents across the state.

The Department is responsible for:

| NCDOI Responsibility | What It Means for Consumers |

|---|---|

| Licensing insurance companies | Carriers must be approved to sell life insurance in North Carolina |

| Licensing agents | Agents must hold an active North Carolina life insurance license |

| Reviewing policy forms | Life insurance contracts must comply with state law |

| Investigating complaints | Consumers can file complaints at no cost |

| Enforcing insurance rules | The Department can take action against companies or agents that violate the law |

Before buying final expense insurance in North Carolina, consumers can verify an agent’s license through the NCDOI license lookup tool.

The Department is headquartered in Raleigh and operates a consumer services division for policyholders who need help with complaints or insurance questions.

Governing Law for Final Expense Insurance

Life insurance in North Carolina is governed by Chapter 58 of the North Carolina General Statutes.

For final expense policies, the most important sections are:

| Law or Regulation | Why It Matters |

|---|---|

| Chapter 58 | Main body of North Carolina insurance law |

| Article 58 | Core life insurance contract rules |

| Article 60 | Life insurance disclosure requirements |

| Small Face Amount Life Insurance Disclosure Act | Applies to many burial insurance and final expense policies |

The Small Face Amount Life Insurance Disclosure Act is especially important because it applies to policies with smaller face amounts, which are common in the senior final expense market.

North Carolina’s 10-Day Free Look Period

North Carolina requires a minimum 10-day free look period on every new individual life insurance policy.

During this period, the policyholder can cancel the policy for any reason and receive a full refund of any premium paid.

| Free Look Situation | Minimum Free Look Period |

|---|---|

| New individual life insurance policy | 10 days |

| Replacement life insurance policy | 20 days |

| Policy purchased by mail | 30 days |

The free look period starts when the policy is delivered. The 10-day notice must appear on the face of the policy, either by sticker or printed language.

This gives North Carolina seniors time to review the policy, compare it to what they were told, and cancel if the coverage is not what they expected.

Small Face Amount Policy Protections

North Carolina’s Small Face Amount Life Insurance Disclosure Act applies to individual life insurance policies with a face amount of $15,000 or less.

That range includes many final expense insurance policies sold to seniors.

The law requires insurers to provide a written disclosure when the total cumulative premiums paid over the life of the policy could exceed the policy’s face amount.

In plain English, this protects seniors from buying a small burial insurance policy without realizing they may eventually pay more into the policy than the death benefit pays out.

For example, an older applicant buying a $10,000 final expense policy could pay premiums for many years. If those total premiums may exceed $10,000, North Carolina law requires that risk to be clearly disclosed.

Replacement Rules

North Carolina has specific replacement rules when a consumer is replacing an existing life insurance policy with a new one.

These rules are designed to protect seniors from churning, which happens when an agent pushes a replacement mainly to earn a new commission.

If a final expense agent recommends replacing an existing life insurance policy, the agent must provide written replacement documentation.

The new policy also receives a longer 20-day free look period, giving the consumer more time to compare the old policy against the new one.

This matters because replacing a policy can sometimes cause a senior to lose valuable benefits, restart a waiting period, or pay more for similar coverage.

Grace Period, Incontestability, and Claim Payment Rules

Three statewide protections apply to final expense insurance policies in North Carolina.

| Protection | North Carolina Rule |

|---|---|

| Grace period | At least 31 days to catch up on a missed premium before lapse |

| Incontestability period | Generally 2 years after the policy is in force |

| Claim payment standard | Interest may apply if benefits are not paid within 30 days after required documentation is received |

The 31-day grace period gives policyholders time to bring a missed premium current before the policy lapses for non-payment.

The two-year incontestability period limits the insurer’s ability to void the policy or deny a claim based on application errors after the policy has been in force for two years. Exceptions can still apply for non-payment, fraud, or misstatement of age or sex.

The 30-day claim payment standard requires insurers to handle death claims promptly. If a claim is not settled within 30 days after all required documentation is received, the unpaid benefit begins accruing interest under North Carolina law.

Guaranty Association Backstop

If a life insurance company becomes insolvent, the North Carolina Life and Health Insurance Guaranty Association provides a financial backstop for policyholders.

The Association protects up to:

| Benefit Type | Protection Limit |

|---|---|

| Death benefits | Up to $300,000 per insured |

| Cash surrender value | Up to $100,000 per insured |

For a typical $10,000 to $25,000 final expense insurance policy, this usually means the full death benefit is protected even if the insurance company fails.

This protection is one reason families should buy coverage from licensed North Carolina insurers and licensed agents.

Graded Death Benefit Disclosures

Many final expense policies in North Carolina use a graded death benefit, especially guaranteed-issue policies that do not ask health questions.

During the graded period, which is often the first two policy years, death from natural causes may not pay the full face amount. Instead, the policy may return premiums paid plus interest.

Accidental death is usually treated differently and may pay the full benefit immediately, depending on the policy.

North Carolina does not prohibit graded death benefits, but the terms must be clearly disclosed at the time of sale.

A final expense agent should explain:

| Graded Benefit Question | What the Consumer Should Know |

|---|---|

| How long does the graded period last? | Often 2 years, but the policy controls |

| What happens if death is natural? | The policy may return premiums plus interest |

| What happens if death is accidental? | The full benefit may be available sooner |

| When does the full face amount apply? | Usually after the graded period ends |

Before buying final expense insurance in North Carolina, seniors should ask whether the policy is level, graded, modified, or guaranteed issue. That one detail can determine how much the family receives if death occurs during the first two policy years.ther than the full face amount. North Carolina does not prohibit graded benefits, but it does require the graded terms to be clearly disclosed at the time of sale under Article 60. Any final expense agent selling a graded policy in the state must walk through exactly how the graded period works, what triggers full benefit payment, and when the full face amount becomes available.

Funeral and Burial Laws in North Carolina

North Carolina law gives families a lot of flexibility when planning final arrangements.

The state has fewer funeral restrictions than many neighboring states. North Carolina allows home funerals, home burials, green burial, and aquamation, and it does not require embalming in most situations.

The rules below explain what North Carolina law requires, what families are allowed to do, and which state agencies oversee funeral homes, crematories, cemeteries, and preneed funeral contracts.

The North Carolina Board of Funeral Service

The North Carolina Board of Funeral Service, often called the NCBFS, regulates the funeral industry in North Carolina.

The Board is headquartered in Raleigh and licenses:

| License Type | What It Covers |

|---|---|

| Funeral directors | Individuals who arrange and direct funeral services |

| Embalmers | Individuals licensed to embalm human remains |

| Funeral establishments | Funeral homes operating in North Carolina |

| Crematories | Facilities that perform cremation |

The NCBFS also investigates consumer complaints, inspects funeral homes and crematories, and enforces North Carolina funeral service laws under Chapter 90, Article 13A of the North Carolina General Statutes.

Consumers can verify a funeral home’s license through the NCBFS website before signing a contract or paying for services.

Death Certificate Filing

In North Carolina, a death certificate must be filed with the local registrar of vital statistics within five days of death under G.S. 130A-115.

North Carolina uses an electronic death registration system.

| Party | Responsibility |

|---|---|

| Physician, physician assistant, nurse practitioner, or medical examiner | Completes and signs the medical portion of the death certificate |

| Funeral director | Completes the demographic portion and files the certificate |

| Family, in a home funeral | May complete and file the demographic portion without a funeral director |

Certified death certificates are issued by the North Carolina Department of Health and Human Services Vital Records office.

The typical cost is $24 for the first certified copy and $15 for each additional copy.

Families usually need certified copies to handle life insurance claims, bank accounts, real estate, pensions, Social Security, and other estate matters.

Burial-Transit Permits

North Carolina does not require a burial-transit permit for every death.

A burial-transit permit is only required under G.S. 130A-113 in certain situations.

| Situation | Is a Burial-Transit Permit Required? |

|---|---|

| Routine in-state burial | No |

| Routine in-state cremation | No |

| Death under medical examiner jurisdiction | Yes |

| Body transported out of North Carolina | Yes |

In medical examiner cases, the medical examiner issues and signs the burial-transit permit within five days of death.

For deaths outside medical examiner jurisdiction, the local registrar issues the permit when the body will be transported across state lines.

Embalming Rules in North Carolina

North Carolina does not require embalming for burial, cremation, aquamation, or in-state transportation.

Refrigeration is an accepted alternative.

Many funeral homes require a body to be refrigerated or embalmed if it remains in their custody longer than 24 hours, but that is usually a funeral home policy rather than a statewide embalming law.

Federal Trade Commission rules require funeral providers to tell consumers in writing that embalming is not generally required by law.

Practical exceptions may apply when there is an extended public viewing over multiple days or when a body is shipped by air to another state.

Cremation Authorization and Waiting Period

Cremation in North Carolina is governed by Chapter 90, Article 13F.

A cremation cannot take place until the required paperwork and authorizations are complete.

| Requirement | What Must Happen |

|---|---|

| Death certificate | A signed death certificate must be filed |

| Written authorization | The legal next-of-kin must authorize cremation |

| Medical examiner authorization | Required unless the death was from natural disease and occurred in a hospital |

North Carolina has a 24-hour waiting period before cremation can occur.

The medical examiner may waive the waiting period in certain communicable disease cases. In real life, the full paperwork process often takes 48 to 72 hours, and many cremations occur within 5 to 7 days after death.

Who Can Authorize Cremation in North Carolina?

North Carolina follows a legal priority order for cremation authorization.

| Priority Order | Person or Group |

|---|---|

| 1 | Surviving spouse |

| 2 | Adult children |

| 3 | Parents |

| 4 | Adult siblings |

| 5 | More distant relatives |

This order matters when family members disagree about cremation or final disposition.

North Carolina law also prohibits cremating more than one body in the same chamber at the same time under G.S. 90-210.129, with narrow exceptions for multiple fetuses or infants from the same mother and birth.

A traditional casket is not required for cremation. The body must be placed in a suitable, rigid combustible container.

Home Funerals

Home funerals are legal in North Carolina.

Families may care for their own dead, file the death certificate themselves, and hold a visitation at home without hiring a funeral director.

North Carolina does not set a specific statewide deadline for final disposition of the body. Families may use refrigeration, dry ice, or other appropriate cooling methods to preserve the body for a reasonable period before burial or cremation.

This makes North Carolina one of the more family-friendly states for home funeral arrangements.

Home Burial

Home burial is legal in North Carolina, and no state statute broadly prohibits burial on private property.

However, families should check county and local zoning rules before planning a private burial. Some urban and suburban jurisdictions restrict where private cemeteries or family burial plots may be located.

A few statewide rules still apply.

| Home Burial Rule | North Carolina Requirement |

|---|---|

| Burial depth | Top of burial vault or encasement must be at least 18 inches below the ground surface |

| Public water supply distance | Cemeteries must be at least 300 feet from any public water supply |

| Local zoning | County or municipal rules may limit private burials |

Because local rules can vary, families should contact the county planning office before creating a family cemetery or burial plot on private land.

Burial at Sea

Burial at sea is legal off the North Carolina coast under federal EPA rules.

For full-body burial at sea, the burial must take place at least three nautical miles offshore in water at least 600 feet deep. The EPA must also be notified within 30 days.

Scattering cremated remains at sea is also allowed.

North Carolina’s long Atlantic coastline, from Corolla and the Outer Banks down to Bald Head Island, gives families many options for coastal memorials and ash scattering.

Green Burial and Aquamation

North Carolina is one of the more progressive states for alternative funeral and burial options.

Green burial is legal in North Carolina, and the state has several Green Burial Council-certified or hybrid burial grounds.

Examples include:

| Cemetery or Burial Ground | Location / Type |

|---|---|

| Carolina Memorial Sanctuary | Mills River; certified conservation burial ground |

| Bluestem Conservation Cemetery | Cedar Grove; conservation cemetery |

| Green Hills | Asheville; hybrid cemetery |

| Oakwood | Raleigh; hybrid cemetery |

| Pine Forest Memorial Gardens | Wake Forest; hybrid cemetery |

Aquamation, also called alkaline hydrolysis or water cremation, is legal in North Carolina under the state cremation statutes.

Current aquamation providers operate in Hillsborough, Shelby, and Wilmington, with pricing typically ranging from $1,295 to $3,500.

Scattering Cremated Remains

North Carolina law requires cremated remains to be removed from their container before scattering.

Ashes may generally be scattered:

| Location | Rule |

|---|---|

| Private property | Allowed with the property owner’s permission |

| Public lands | Follow any permit rules or agency restrictions |

| At sea | Follow federal EPA guidelines |

| From aircraft | Allowed under federal aviation rules if remains are removed from the container first |

Families should always check local rules before scattering ashes in parks, public beaches, waterways, or protected natural areas.

Preneed Funeral Contracts

North Carolina tightly regulates preneed funeral contracts.

A preneed funeral contract allows a consumer to pay in advance for specific funeral services. Only licensed funeral establishments with a separate preneed license may sell these contracts.

Preneed funds must be protected through a trust or a dedicated insurance policy.

This is different from final expense insurance.

| Option | How It Works |

|---|---|

| Preneed funeral contract | Usually tied to a specific funeral home and specific funeral plan |

| Final expense insurance policy | Pays cash to a beneficiary, who can use the money at any provider |

This distinction matters. A preneed funeral contract can help lock in arrangements with one funeral home, while a final expense insurance policy gives the family more flexibility to pay for funeral costs, cremation costs, cemetery expenses, medical bills, travel, or other end-of-life expenses.

Regions and Major Metros in North Carolina

North Carolina stretches more than 500 miles from the mountains to the coast. The state divides into three primary geographic regions, and each region has its own economy, population pattern, funeral cost structure, and senior demographic.

Understanding where a family lives helps anchor everything from funeral pricing to county-level senior resources.

North Carolina has 100 counties, the second-most of any state east of the Mississippi. Those counties group naturally into the regions below.

North Carolina’s Three Primary Regions

North Carolina’s three official geographic regions are based on landforms and are recognized by the North Carolina Department of Public Instruction and NCpedia, a reference published by the State Library of North Carolina.

| Region | What It Covers | Main Population Anchor |

|---|---|---|

| Mountains | Western North Carolina, including the Blue Ridge and Great Smoky Mountains | Asheville |

| Piedmont | Central plateau from the Blue Ridge foothills to the fall line near Raleigh | Charlotte, Raleigh-Durham, Greensboro-Winston-Salem |

| Coastal Plain | Eastern North Carolina from the fall line to the Atlantic Ocean | Wilmington, Fayetteville, New Bern, Outer Banks |

The Mountains

The Mountains are North Carolina’s westernmost region.

This area includes the Blue Ridge Mountains, the Great Smoky Mountains, and smaller counties with older median ages. Asheville is the main anchor metro.

The Mountains attract many retirees because of the cooler climate, scenery, and slower pace of life. Counties like Henderson, Buncombe, Transylvania, and Polk have strong senior populations and steady retirement in-migration.

The Piedmont

The Piedmont is the central region of North Carolina.

It runs from the foothills of the Blue Ridge east to the fall line near Raleigh. This is where most North Carolinians live.

The Piedmont includes all three of the state’s largest metro areas:

| Piedmont Metro | Common Name |

|---|---|

| Charlotte-Concord-Gastonia | Metrolina / Charlotte metro |

| Raleigh-Durham-Cary | Research Triangle |

| Greensboro-Winston-Salem-High Point | Piedmont Triad |

Together, these metros form what demographers often call the Piedmont Urban Crescent.

For final expense planning, this matters because metro areas usually have higher funeral home, cemetery, and operating costs than smaller rural counties.

The Coastal Plain

The Coastal Plain is North Carolina’s largest region by land area. It covers roughly 45% of the state, running from the fall line east to the Atlantic Ocean.

The Coastal Plain is often split into two sub-regions.

| Coastal Plain Sub-Region | What It Includes |

|---|---|

| Inner Coastal Plain | Farmland and mid-size cities like Rocky Mount, Goldsboro, and Fayetteville |

| Outer Coastal Plain / Tidewater | Wilmington, New Bern, the Outer Banks, and coastal counties |

The Coastal Plain includes both rural agricultural counties and fast-growing coastal retirement areas.

Brunswick County, New Hanover County, Carteret County, and Dare County are especially important for senior population growth and final expense insurance demand.

The Sandhills

The Sandhills are a smaller sub-region between the Piedmont and the Inner Coastal Plain.

This area includes parts of:

| Sandhills Counties |

|---|

| Richmond |

| Scotland |

| Hoke |

| Cumberland |

| Harnett |

| Lee |

| Moore |

| Montgomery |

Moore County is especially important because of Pinehurst and Southern Pines. This area is one of North Carolina’s best-known golf and retirement destinations.

Counties by Region

The table below groups North Carolina’s 100 counties into their primary region.

Some border counties may be classified differently by different sources, but these groupings follow the most widely used state geographic framework.

| Region | Counties |

|---|---|

| Mountains | Alleghany, Ashe, Avery, Buncombe, Burke, Caldwell, Cherokee, Clay, Graham, Haywood, Henderson, Jackson, Macon, Madison, McDowell, Mitchell, Polk, Rutherford, Swain, Transylvania, Watauga, Wilkes, Yancey |

| Piedmont | Alamance, Alexander, Anson, Cabarrus, Caswell, Catawba, Chatham, Cleveland, Davidson, Davie, Durham, Forsyth, Franklin, Gaston, Granville, Guilford, Iredell, Lee, Lincoln, Mecklenburg, Montgomery, Moore, Orange, Person, Randolph, Richmond, Rockingham, Rowan, Stanly, Stokes, Surry, Union, Vance, Wake, Warren, Yadkin |

| Coastal Plain / Inner | Bladen, Columbus, Cumberland, Duplin, Edgecombe, Greene, Halifax, Harnett, Hoke, Johnston, Jones, Lenoir, Nash, Northampton, Robeson, Sampson, Scotland, Wayne, Wilson |

| Coastal Plain / Outer Tidewater | Beaufort, Bertie, Brunswick, Camden, Carteret, Chowan, Craven, Currituck, Dare, Gates, Hertford, Hyde, New Hanover, Onslow, Pamlico, Pasquotank, Pender, Perquimans, Pitt, Tyrrell, Washington |

Top Metros in North Carolina

North Carolina has several major metros that anchor the state’s population and senior insurance markets.

| Metro Area | Region | Population Estimate |

|---|---|---|

| Charlotte-Concord-Gastonia, NC-SC | Piedmont | 2,883,370 |

| Raleigh-Durham-Cary | Piedmont | 2,439,501 |

| Greensboro-Winston-Salem-High Point | Piedmont | 1,760,496 |

| Fayetteville | Coastal Plain / Sandhills | 529,000 |

| Asheville | Mountains | 475,000 |

| Wilmington | Coastal Plain / Outer | 470,000 |

| Hickory-Lenoir-Morganton | Piedmont / Mountains | 370,000 |

The three largest population centers are Charlotte, the Research Triangle, and the Piedmont Triad. These metros drive much of North Carolina’s growth, health care access, and senior insurance activity.

Which Counties Cluster Into Each Major Metro

Metro boundaries do not always follow region lines. They are based more on commuting patterns, employment markets, and economic connection.

The table below shows which North Carolina counties fall into each major metro area.

| Metro | Constituent North Carolina Counties |

|---|---|

| Charlotte metro / Metrolina CSA | Anson, Cabarrus, Cleveland, Gaston, Iredell, Lincoln, Mecklenburg, Rowan, Stanly, Union |

| Research Triangle | Chatham, Durham, Franklin, Granville, Johnston, Orange, Person, Vance, Wake |

| Piedmont Triad | Alamance, Davidson, Davie, Forsyth, Guilford, Randolph, Rockingham, Stokes, Surry, Yadkin |

| Fayetteville metro | Cumberland, Hoke |

| Asheville metro | Buncombe, Haywood, Henderson, Madison |

| Wilmington metro | Brunswick, New Hanover, Pender |

| Hickory-Lenoir-Morganton | Alexander, Burke, Caldwell, Catawba |

This helps readers connect their local county page to the broader regional market.

For example, a family in Brunswick County is part of the Wilmington metro, while a family in Henderson County is tied more closely to the Asheville retirement market.

Senior Demographics and Retirement Patterns

North Carolina has become one of the fastest-growing retirement destinations in the Southeast.

Several regional patterns shape where the state’s senior population is concentrated.

Mountain Retirement Communities

Western North Carolina attracts retirees from Florida, the Northeast, and other parts of the Southeast.

Counties with strong retirement patterns include:

| Mountain Retirement Area | Why It Matters |

|---|---|

| Henderson County | Hendersonville has an older median age and strong retiree base |

| Buncombe County | Asheville anchors the mountain retirement market |

| Transylvania County | Brevard attracts retirees seeking scenery and smaller-town living |

| Polk County | Popular with retirees looking for quieter mountain communities |

These counties tend to have strong demand for final expense insurance, burial insurance, Medicare planning, and long-term senior resources.

Sandhills Retirement

The Sandhills are another major retirement belt.

Moore County, anchored by Pinehurst and Southern Pines, is one of the oldest counties in North Carolina by median age.

This area is well known for golf communities, planned retirement neighborhoods, and older homeowners relocating from other states.

Coastal Retirement

North Carolina’s coastal counties also attract a large senior population.

Brunswick County is one of the strongest examples. Communities like Southport, Oak Island, Leland, and Calabash have drawn retirees for more than a decade.

Other coastal retirement counties include:

| Coastal County | Senior Market Pattern |

|---|---|

| Brunswick County | Fast-growing retirement corridor |

| Dare County | Outer Banks retirement and seasonal population |

| Carteret County | Coastal retirement and boating communities |

| New Hanover County | Wilmington-area retirees and health care access |

These areas often have strong demand for cremation planning, final expense insurance, and burial insurance because many retirees move there without extended family nearby.

Military Retiree Concentrations

North Carolina also has one of the largest military retiree populations in the country.

Several counties are tied directly to major military installations.

| County | Military Connection |

|---|---|

| Cumberland County | Fort Liberty, formerly Fort Bragg |

| Hoke County | Fort Liberty area |

| Onslow County | Camp Lejeune |

| Craven County | MCAS Cherry Point |

| Rowan County | Salisbury National Cemetery |

Military retirees may qualify for VA burial benefits, but those benefits do not always cover every end-of-life cost.

Many families still use a final expense insurance policy to help pay for non-covered expenses such as transportation, family travel, cemetery upgrades, memorial services, or remaining household bills.

Veterans Cemetery Options in North Carolina

Salisbury National Cemetery, located in Rowan County, is the only VA national cemetery in North Carolina currently open for new interments of both casketed and cremated remains.

North Carolina also has state veterans cemeteries in:

| State Veterans Cemetery Location |

|---|

| Spring Lake |

| Jacksonville |

| Black Mountain |

These cemetery options can provide meaningful burial cost relief for eligible veterans and their families.

Why These Regional Patterns Matter

Across all 100 counties, more than 1.8 million North Carolinians are age 65 or older.

That senior population is roughly the size of the entire Piedmont Triad.

Final expense and burial insurance demand tends to cluster most heavily in:

| High-Demand Area | Why Demand Is Strong |

|---|---|

| Mountains | Older median ages and retirement in-migration |

| Sandhills | Pinehurst, Southern Pines, and golf-retirement communities |

| Outer Coastal Plain | Coastal retirees and fast-growing senior communities |

| Military counties | Veterans, military retirees, and families planning around VA benefits |

For families comparing funeral costs, cremation costs, cemetery options, and final expense insurance in North Carolina, region matters. A senior in Asheville, Pinehurst, Wilmington, Charlotte, or a rural Coastal Plain county may face very different planning needs.

Counties We Serve in North Carolina

Palmetto Mutual writes final expense, burial, and funeral life insurance for seniors across every one of North Carolina’s 100 counties. The directory below lists every county in the state alphabetically so families can quickly find their local page with regional cost data, cemetery information, funeral home guidance, and coverage options specific to where they live. Over time this list will be replaced with a searchable county menu as each county page is published.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.