Home > South Carolina

Final Expense Insurance in South Carolina — Coverage for Seniors from the Upstate to the Coast

South Carolina’s final expense landscape reflects the state’s sharp regional contrasts, from the foothills of the Upstate down through the Midlands and Pee Dee into the Low Country. With more than 1.1 million residents age 65 and older, heavy retiree inflows to the Grand Strand and Hilton Head, and a significant military retiree population anchored around Charleston, Columbia, and Sumter, burial insurance demand in South Carolina skews older and more coastal than the national average. This page serves as the statewide hub for funeral cost data, insurance regulations, burial laws, and county-level coverage across all 46 South Carolina counties.

Funeral and Cremation Costs in South Carolina

South Carolina funeral prices generally track slightly below the national median, but costs vary meaningfully between the Upstate, the Midlands, the Pee Dee, and the Low Country. The table below shows the current statewide averages for the four most common disposition choices, followed by regional variation and the factors driving price differences across the state.

Statewide Averages

| Service Type | South Carolina Average | National Median (NFDA) |

|---|---|---|

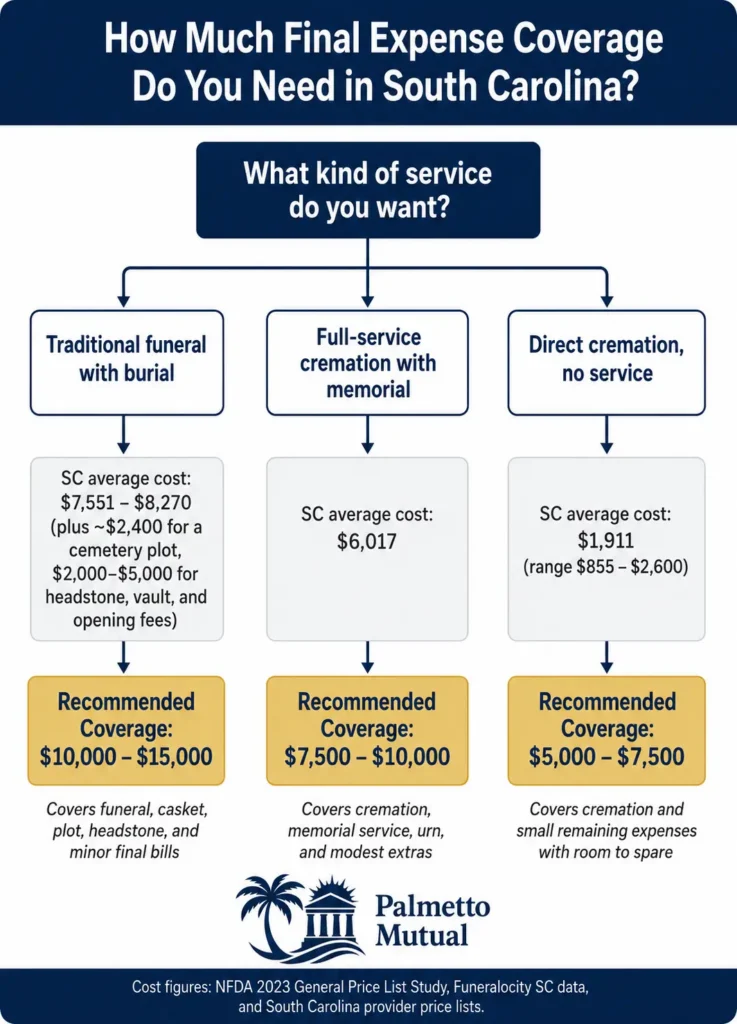

| Traditional funeral with burial | $7,551 – $8,270 | $8,300 (without vault) / $9,995 (with vault) |

| Direct burial (no ceremony) | $3,060 – $5,137 | $5,138 |

| Full-service cremation with memorial | $6,017 | $6,280 |

| Direct cremation (no service) | $1,911 (average); $855 – $2,600 (range) | $2,202 |

Figures drawn from Funeralocity’s 2025 South Carolina pricing data, the NFDA 2023 General Price List Study, and published General Price Lists from South Carolina providers including The Standard Cremation & Funeral Center, Cole Funeral Home, Upstate Cremation Services, and Sosebee Mortuary.

Cemetery plot costs are not included in any of the figures above. A burial plot in South Carolina adds roughly $2,400 on average, and headstone costs, opening and closing fees, and vaults add another $2,000 to $5,000 depending on the cemetery.

Regional Cost Variation

Regional Funeral Cost Variation in South Carolina

Funeral pricing in South Carolina usually follows the same regional lines as the state’s cost of living.

The Upstate and Pee Dee tend to have the lowest funeral and cremation costs, while the Low Country is usually the most expensive region.

| South Carolina Region | Cities Included | Typical Pricing Pattern |

|---|---|---|

| Upstate | Greenville, Spartanburg, Anderson | Often among the lowest-cost areas |

| Pee Dee | Florence, Darlington, Marlboro | Generally more affordable than coastal markets |

| Midlands | Columbia, Lexington, Sumter | Usually close to the statewide average |

| Low Country | Charleston, Berkeley, Dorchester, Beaufort | Often the highest-cost region |

In the Upstate and Pee Dee, direct cremation packages may be posted as low as $855 to $925 at providers such as Sosebee Mortuary and Upstate Cremation Services.

In the Midlands, direct cremation prices usually sit closer to the statewide average. Families in Columbia, Lexington, and Sumter commonly see direct cremation packages between $950 and $1,500.

The Low Country tends to carry the highest funeral prices in South Carolina. In the Charleston area, cremation packages that include a memorial service commonly run between $2,500 and $4,995 at providers such as The Lowcountry Mortuary and The Standard Cremation & Funeral Center.

Traditional funeral totals in the Low Country can regularly exceed $9,000 once cemetery fees are added.

What Drives the Regional Spread?

Funeral costs in South Carolina vary because each region has different pricing pressures. Coastal areas tend to cost more, while inland and rural areas often have wider price gaps between providers.

Why the Low Country Costs More

The Low Country usually has higher funeral prices for the same reasons housing costs are higher in places like Charleston, Mount Pleasant, and Hilton Head:

- Coastal land is limited.

- Operating costs are higher in tourism-driven markets.

- Retiree-heavy communities create steady demand.

- Funeral home competition may be limited compared to demand.

That combination can push prices higher for both burial and cremation services.

Why the Upstate Is Often More Affordable

The Upstate tends to benefit from stronger competition among independent funeral homes and cremation providers.

Cities like Greenville and Spartanburg also generally have lower real estate and operating costs than coastal markets. That helps keep many funeral and cremation prices more competitive.

Why Rural Areas Have the Widest Price Swings

In parts of the Pee Dee and Midlands, the spread can be wider from one funeral home to another.

This is especially true for cash-advance items and optional services, including:

- Caskets

- Embalming

- Burial containers

- Transportation

- Memorial service add-ons

In some counties, the same service can vary by several hundred dollars between providers.

How South Carolina Compares Nationally

South Carolina still has a pricing advantage compared to many states.

The state’s 2025 cost of living is roughly 9% below the U.S. average, and South Carolina’s traditional burial and direct burial costs come in about 4% below national figures.

But cremation is rising here, too. The 2025 U.S. cremation rate is projected at 63.4%, and South Carolina’s coastal metros are tracking close to that trend.

What This Means for Burial Insurance

For most families buying burial insurance in South Carolina, the right coverage amount depends on the type of service they want.

A $10,000 to $15,000 final expense policy is usually enough to cover a traditional funeral with burial comfortably.

A $5,000 to $7,500 policy is often enough for direct cremation plus a modest memorial, with some room left over for smaller final expenses.

Final Expense Insurance Regulations in South Carolina

Burial insurance sold in South Carolina is regulated under Title 38 of the South Carolina Code of Laws, with additional life insurance and producer requirements found in Chapter 69 of the South Carolina insurance regulations.

For most consumers buying a small whole life final expense policy, the most important rules are simple:

- Who regulates the policy

- How long you have to cancel

- What happens if you miss a payment

- How claims are paid

- What protections exist if the insurance company fails

Who Regulates Final Expense Insurance in South Carolina?

The South Carolina Department of Insurance, also called the SCDOI, is the state’s main insurance regulator.

The department is responsible for:

- Licensing insurance agents and carriers

- Reviewing policy forms before they can be sold

- Enforcing South Carolina insurance laws

- Handling consumer complaints against insurance companies and producers

The SCDOI’s main office is located at 1201 Main Street, Suite 1000, Columbia, SC.

Consumers can also use the department’s website at doi.sc.gov to look up agent licenses, file complaints, and verify whether an insurer is authorized to do business in South Carolina.

Free Look Period

South Carolina gives every new life insurance policyholder a 10-day free look period starting on the day the policy is delivered.

During that time, the policyholder can cancel the policy for any reason and receive a full refund of all premiums paid.

The free look period is longer in certain situations:

- 10 days for most new life insurance policies

- 30 days for mail-order or direct-response policies

- 20 days when the new policy replaces an existing policy

Even if the insured dies during the free look period, the insurance company must still pay the death benefit to the beneficiary.

Grace Period for Missed Premiums

If a final expense policyholder misses a monthly premium, South Carolina law requires a minimum 30-day grace period before the policy can be canceled for nonpayment.

Most carrier contracts use a 31-day grace period.

If the insured dies during the grace period, and the claim is otherwise valid, the company must still pay the death benefit. The unpaid premium is usually deducted from the payout.

Contestability and Material Misrepresentation

Every life insurance policy sold in South Carolina has a two-year contestability period.

During the first two years, the insurance company can investigate the application if a claim is filed. If the carrier finds a material misrepresentation that would have changed the underwriting decision, it may be able to void the policy.

This is why accurate health disclosures matter when applying for final expense insurance.

Missing or incorrect information about medications, diagnoses, tobacco use, or major health conditions can put the death benefit at risk during the first two policy years.

After two years, the policy generally becomes incontestable, except in cases of fraud proven by clear and convincing evidence.

Replacement Rules — Regulation 69-12.1

South Carolina has specific consumer protections for life insurance replacements under SC Code of Regulations 69-12.1.

These rules apply when an agent recommends replacing an existing final expense, burial life insurance, or whole life insurance policy with a new one.

If a replacement is involved:

- The agent must provide written replacement notice.

- The notice must identify each existing policy being replaced.

- The replacing insurer must notify the existing insurer.

- The existing insurer has the right to contact the policyholder directly.

These rules help protect seniors from unnecessary policy replacements, sometimes called churning.

Churning happens when a new policy is sold mainly to generate a commission, rather than because it truly benefits the consumer.

Claims Settlement Timeline

Under SC Code Section 38-63-80, South Carolina life insurance companies must settle lump-sum life insurance and funeral life insurance claims within 30 days of receiving proof of death and all required claim documents.

If the claim is delayed beyond 30 days, the insurer must pay statutory interest on the death benefit, running back to the date of death.

Graded Death Benefit Rules

Some final expense insurance policies issued to seniors with health problems include a graded death benefit.

This means the full face amount may not be paid if the insured dies from natural causes during the first two policy years.

In South Carolina, SC Bulletin 2004-04 governs graded and delayed benefit policies.

The policy must clearly disclose:

- The graded benefit structure

- The waiting period

- The amount payable during the graded period

Accidental death is usually covered at the full face amount from day one, even under a graded benefit policy.

Healthier applicants may qualify for first-day full coverage, which is also widely available in South Carolina.

South Carolina Life, Accident, and Health Insurance Guaranty Association

If a South Carolina-licensed life insurance company becomes insolvent, the South Carolina Life, Accident, and Health Insurance Guaranty Association provides a safety net.

For life insurance death benefits, the guaranty association protects up to $300,000 per insured person.

That limit is far above the coverage amount on most burial insurance policies in South Carolina.

For consumers, this means a properly licensed final expense policy carries an additional layer of protection if the issuing carrier ever fails.

Preexisting Condition Exclusions

South Carolina does not allow life insurance companies to carve out specific preexisting condition exclusions from life insurance contracts.

A carrier may offer a graded death benefit policy based on health history, but it cannot exclude a specific illness from coverage the way health insurance once did.

This is especially important for seniors buying burial insurance in South Carolina.

Many applicants have chronic health conditions, and final expense insurance is often designed for people who may not qualify for traditional term life insurance.

Funeral and Funeral and Burial Laws in South Carolina

South Carolina funeral, burial, and cremation laws are handled through a mix of state statutes and board regulations.

For most families, the most important legal questions come up during the first week after death:

- Who files the death certificate?

- Is a burial permit required?

- Is embalming required?

- Who can authorize cremation?

- Are home funerals legal?

- Can a family choose green burial or private property burial?

Who Regulates Funerals and Burials in South Carolina?

Funeral homes, funeral directors, embalmers, crematories, and funeral establishments are regulated by the South Carolina State Board of Funeral Service.

That board operates under the South Carolina Department of Labor, Licensing and Regulation, also called SCLLR.

The board enforces major funeral and cremation laws, including:

- Title 40, Chapter 19 — Embalmers and Funeral Directors

- Title 32, Chapter 8 — Cremation Authorizations and Procedures

The South Carolina Department of Public Health, or DPH, handles the death certificate and burial permit side of the process through the Bureau of Vital Statistics.

Death Certificate Filing Process

Under SC Code Section 44-63-74, every death that occurs in South Carolina must be filed with the Bureau of Vital Statistics within 5 days of the date of death.

In most cases, the funeral director files the death certificate through South Carolina’s electronic death registration system, known as the Web Deaths portal.

The medical certifier is usually the:

- Attending physician

- Coroner

- Medical examiner

The medical certifier must complete the cause-of-death section within 48 hours of being notified.

Late filings can result in daily administrative penalties under South Carolina law.

Electronic Death Certificate Filing

A 2022 law, H.3325, made electronic death certificate filing mandatory in South Carolina.

There is one important exception.

If a family member is handling the final disposition without compensation, such as in a natural funeral or home funeral, the medical certification still has to be submitted electronically, but the family may file the rest of the certificate on paper.

Certified Copies of the Death Certificate

Certified copies of a South Carolina death certificate are ordered through SC DPH Vital Records.

The current cost is:

- $12 for the first certified copy

- $3 for each additional copy ordered at the same time

Families often order 8 to 10 certified copies because they may be needed for:

- Life insurance claims

- Bank accounts

- Social Security

- Property transfers

- Estate matters

For the first 50 years after death, certified copies are limited to immediate family members and legal representatives. After 50 years, the death record becomes public.

Burial Permit Requirements

South Carolina requires a Burial-Removal-Transit Permit before a body can be:

- Buried

- Cremated

- Transported across state lines

The permit is issued by the county coroner or subregistrar in the county where the death occurred.

In most cases, it is issued within 48 hours of death and handled by the funeral director as part of the disposition process.

For deaths that happen outside a hospital, nursing home, or other institution, the county registrar must require the coroner to issue the permit under SC Code Section 44-63-84.

Embalming Rules

South Carolina does not require embalming for every death.

Embalming is only legally necessary in limited situations, including:

- When the body will be publicly viewed

- When remains are transported by common carrier, such as airplane or commercial rail

For many other arrangements, embalming is optional.

That includes:

- Direct burial

- Direct cremation

- Private home viewing

- Timely burial without public viewing

Funeral homes without refrigeration may recommend embalming, but that does not automatically mean it is legally required.

The Federal Trade Commission Funeral Rule also requires funeral providers to disclose that embalming is not required by law except in limited cases.

In South Carolina, embalming costs often range from $300 to $1,995.

Cremation Authorization Rules

Cremation in South Carolina is governed by the South Carolina Safe Cremation Act, found in Title 32, Chapter 8.

Three rules matter most for families.

1. South Carolina Has a 24-Hour Cremation Waiting Period

State law requires a minimum 24-hour waiting period between the time of death and cremation.

This gives time for authorizations, medical review, and any required coroner inquiry.

2. Written Cremation Authorization Is Required

Cremation must be authorized in writing.

Authorization can come from:

- The person before death through a pre-signed authorization

- The next of kin after death, following South Carolina’s legal order of priority

The usual next-of-kin order begins with the spouse, then adult children, parents, adult siblings, and other relatives.

3. A Coroner Permit Is Required Before Cremation

The county coroner or medical examiner must issue a cremation permit before the cremation takes place.

Pacemakers and other battery-powered or pressurized medical devices must be removed before cremation for safety reasons.

South Carolina law also now defines cremation to include alkaline hydrolysis, also called water cremation or aquamation, following 2024 amendments.

If cremated remains are unclaimed by the next of kin, South Carolina law allows the funeral home or crematory to dispose of them after 60 days.

Home Funeral Legality

Home funerals are legal in South Carolina.

Families may care for their own dead without hiring a funeral director. That can include:

- Washing the body

- Dressing the body

- Holding a viewing at home

- Transporting the body to a cemetery or crematory

South Carolina law does not set a specific deadline for burial or cremation, and there is no general embalming requirement.

Families handling a home funeral must still complete the legal paperwork.

That includes:

- Filing the death certificate within 5 days

- Getting the medical certification from the physician, coroner, or medical examiner

- Obtaining the Burial-Removal-Transit Permit

- Getting the cremation permit if cremation is chosen

- Following the 24-hour cremation waiting period

One practical note: some crematories only accept remains delivered by a licensed funeral director. Families planning a home funeral with cremation should confirm the crematory’s policy before making arrangements.

Burial at Sea

Burial at sea is an option for some South Carolina families, especially in coastal areas like the Low Country and Grand Strand.

Federal EPA rules apply.

For full-body burial at sea, the burial must generally take place:

- At least 3 nautical miles from shore

- In water deeper than 600 feet

Cremated remains may also be scattered or buried at sea at least 3 nautical miles from land.

A burial-at-sea report must be filed with the EPA within 30 days.

Families in areas such as Charleston, Beaufort, and Horry County may be able to work with charter captains who handle full-body or cremated-remains burial-at-sea services.

Green Burial Legality

Green burial is legal in South Carolina.

A green burial usually means burial:

- Without embalming

- In a biodegradable container or shroud

- Without a concrete vault

South Carolina does not have a state law requiring embalming, caskets, or burial vaults.

Vault requirements usually come from cemetery policy, not state law.

South Carolina also has certified green burial grounds, including Ramsey Creek Preserve in Westminster, Oconee County, known as the first certified conservation burial ground in the United States.

Families considering green burial should confirm in writing that the cemetery will accept:

- Unembalmed remains

- A biodegradable casket

- A burial shroud

- Burial without a vault or liner

Burial on Private Property

South Carolina does not have a state law that broadly prohibits burial on private property.

Private family cemeteries have a long history in rural parts of the Upstate, Pee Dee, and Midlands.

However, local rules may still apply.

Before planning a private-land burial, families should check with:

- The town or county clerk

- The local health department

- Any applicable zoning office

When a body is buried on private land, the burial should be documented with the property deed.

The property owner may also need to disclose the burial location to future buyers when the property is sold.

Regions and Major Metros in South Carolina

South Carolina is commonly divided into four major regions:

- Upstate

- Midlands

- Pee Dee

- Low Country

Each region has its own geography, economy, cost of living, and senior population trends.

Understanding these regions helps readers quickly find where their county fits — and makes it easier to connect them to the right local South Carolina final expense insurance page.

The Four Regions of South Carolina

Upstate South Carolina

The Upstate sits in the northwestern corner of South Carolina near the foothills of the Blue Ridge Mountains.

It is also called the Upcountry or Piedmont region.

The Upstate is anchored by major cities like:

- Greenville

- Spartanburg

- Anderson

This region is known for manufacturing, economic growth, cooler temperatures, four distinct seasons, and the highest elevations in South Carolina.

Midlands South Carolina

The Midlands sit in the center of South Carolina.

This region includes Columbia, the state capital, and serves as the center of state government, higher education, and military activity.

The Midlands include:

- Rolling Sandhills terrain

- The Saluda and Congaree river corridors

- The University of South Carolina

- Fort Jackson

The region gets its name from its location between the Upstate and the Low Country.

Pee Dee South Carolina

The Pee Dee covers the northeastern part of South Carolina.

The region takes its name from the Pee Dee River and the Pee Dee Native American tribe.

The Pee Dee includes both coastal and inland communities, including:

- Horry County

- Georgetown County

- Myrtle Beach

- Florence

- Darlington

- Sumter

This region includes the Grand Strand, a 60-mile stretch of coastline centered around Myrtle Beach.

The Pee Dee is one of the most affordable regions in South Carolina and one of the state’s fastest-growing retirement destinations.

Low Country South Carolina

The Low Country covers the southern coastal part of South Carolina.

It stretches from Georgetown and Berkeley counties down through:

- Charleston

- Beaufort

- Hilton Head

- The Savannah River border with Georgia

The Low Country is known for salt marshes, tidal creeks, barrier islands, Spanish moss, live oaks, and Gullah cultural heritage.

It is also South Carolina’s tourism anchor and one of the highest cost-of-living regions in the state.

South Carolina Counties by Region

The table below groups all 46 South Carolina counties by region using standard state regional definitions.

Regional boundaries are not always perfect. Some counties near the edges may be grouped differently by different agencies, but this layout gives readers a practical way to find their local county page.

| Region | Counties |

|---|---|

| Upstate | Abbeville, Anderson, Cherokee, Greenville, Greenwood, Laurens, McCormick, Oconee, Pickens, Spartanburg, Union |

| Midlands | Aiken, Barnwell, Chester, Edgefield, Fairfield, Kershaw, Lancaster, Lexington, Newberry, Richland, Saluda, York |

| Pee Dee | Chesterfield, Clarendon, Darlington, Dillon, Florence, Georgetown, Horry, Lee, Marion, Marlboro, Sumter, Williamsburg |

| Low Country | Allendale, Bamberg, Beaufort, Berkeley, Calhoun, Charleston, Colleton, Dorchester, Hampton, Jasper, Orangeburg |

Top Metros in South Carolina

South Carolina’s population is concentrated in a handful of major metro areas.

| Metro Area | Approx. MSA Population | Region |

|---|---|---|

| Greenville–Anderson–Spartanburg | ~1.4 million | Upstate |

| Columbia | ~840,000 | Midlands |

| Charleston–North Charleston | ~800,000 | Low Country |

| Myrtle Beach–Conway–North Myrtle Beach | ~550,000 | Pee Dee |

| Hilton Head Island–Bluffton | ~230,000 | Low Country |

| Florence | ~200,000 | Pee Dee |

| Sumter | ~105,000 | Pee Dee |

At the city level, Charleston is the largest city in South Carolina, with roughly 155,000 to 161,000 residents.

It is followed by:

- Columbia

- North Charleston

- Mount Pleasant

- Rock Hill

- Greenville

- Summerville

- Goose Creek

- Greer

- Myrtle Beach

Metro-to-County Clusters

South Carolina’s largest metro areas often cross county lines.

That matters because many families search by city, but insurance and funeral cost pages are often organized by county.

Charleston Metro

The Charleston metro covers the tri-county area:

- Charleston County

- Berkeley County

- Dorchester County

Columbia Metro

The Columbia metro includes:

- Richland County

- Lexington County

- Fairfield County

- Kershaw County

- Calhoun County

- Saluda County

Greenville–Spartanburg Metro

The Greenville–Spartanburg metro includes:

- Greenville County

- Spartanburg County

- Anderson County

- Pickens County

- Laurens County

- Union County

Oconee and Cherokee counties are also nearby and often connected to the broader Upstate market.

Grand Strand / Myrtle Beach Metro

The Grand Strand and Myrtle Beach metro center on Horry County and extend into Georgetown County.

This is one of South Carolina’s strongest retirement migration areas.

Hilton Head Metro

The Hilton Head Island–Bluffton metro covers:

- Beaufort County

- Jasper County

Rock Hill / Fort Mill

Rock Hill and Fort Mill are located in York County.

This area is part of the larger Charlotte metro area, which crosses the North Carolina–South Carolina border.

Demographics Relevant to Final Expense Insurance

South Carolina has one of the fastest-growing senior populations in the country.

The state has roughly 1.1 million residents age 65 and older, representing about 19% of South Carolina’s total population.

That is above the national average and creates strong demand for:

- Final expense insurance

- Burial insurance

- Cremation planning

- Small whole life insurance policies

- Senior-focused end-of-life planning

Retirement Migration to the Coast

Coastal counties have seen major retiree growth over the past two decades.

This is especially true in:

- Horry County

- Beaufort County

- Georgetown County

- Charleston County

Horry County grew by about 23% between 2010 and 2020, with much of that growth tied to retirees relocating to Myrtle Beach and the Grand Strand.

Beaufort County continues to attract retirees to Hilton Head and Bluffton.

These coastal counties have some of the highest senior concentrations in South Carolina.

Military Retiree Population

South Carolina also has a large military retiree population.

Major military communities include:

- Fort Jackson in Columbia

- Shaw Air Force Base in Sumter

- Joint Base Charleston

- Marine Corps Recruit Depot Parris Island in Beaufort

Many military retirees supplement VA benefits, SGLI, or other military-related coverage with private final expense insurance.

Rural Senior Communities

The Pee Dee and inland Midlands have older, more rural populations.

Many of these counties also have lower median household incomes.

In these areas, the most common final expense insurance products are usually small-face-amount burial policies, often in the $5,000 to $15,000 range.

These policies are commonly paid by monthly bank draft or Social Security direct draft.

Statewide Growth Driver

South Carolina’s population is projected to reach about 6.4 million by 2042.

Much of that growth is expected to come from retirees and working-age adults moving in from other states.

As the elderly population continues to grow, South Carolina is becoming one of the strongest states in the country for senior-focused insurance, burial insurance, and end-of-life planning services.

Counties We Serve in South Carolina

Palmetto Mutual writes final expense insurance across all 46 counties in South Carolina, from the Blue Ridge foothills of the Upstate down to the barrier islands of the Low Country. Use the directory below to find your county and continue to the local page for county-specific funeral costs, cemetery options, and final expense information tailored to your area.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.