Home > Final Expense Insurance Cost

How Much Does Final Expense Insurance Cost In 2026?

For most healthy buyers, final expense insurance costs somewhere between $30 and $100 a month, with $10,000 to $15,000 of coverage often landing in the $40 to $70 range for someone in their sixties. That spread is wide for a reason — what you actually pay comes down to a handful of specific things: your age, your gender, whether you use tobacco, your health, how much coverage you buy, the plan type you qualify for, and the carrier you choose. Two people the same age can pay very different premiums for the very same coverage. This page answers the cost question two ways at once: it gives you the general numbers most buyers see, and it points you toward deeper guidance for your own situation. The sections ahead cover the average rates, every factor that moves your price, how much coverage you really need, how costs change by age, and an honest look at what “the cheapest final expense insurance” actually means.

Final Expense Coverage Calculator

Add up your final costs to find the right policy size for your family.

What Does Final Expense Insurance Actually Cost?

Before we break down every factor, here’s the baseline. The numbers below describe a healthy, non-tobacco buyer purchasing a typical amount of coverage, which is the most common type of final expense insurance shopper.

Final Expense Insurance Costs at a Glance

Most people who buy burial insurance are healthy, non-tobacco users in their 60s, choosing coverage of $10,000 to $15,000. For that buyer, the monthly premium usually falls between $48 and $85, depending on exact age and the amount of coverage they choose.

Women tend to pay toward the lower end of that range and men toward the higher end. A 65-year-old woman averages about $50 a month for $10,000 in coverage, while a man the same age averages about $66. Everything else on this page explains the details behind that headline number.

National Average Final Expense Rates by Coverage Amount and Age

This table is the foundation for the rest of the page. It shows average monthly premiums for a healthy non-tobacco applicant across the four most common coverage amounts and the most common purchase ages. Use it as a yardstick to judge any quote you receive elsewhere.

| Age | $10,000 | $15,000 | $20,000 | $25,000 |

|---|---|---|---|---|

| 55 | $36 | $52 | $69 | $85 |

| 60 | $44 | $64 | $84 | $105 |

| 65 | $56 | $83 | $110 | $136 |

| 70 | $75 | $110 | $146 | $182 |

| 75 | $100 | $148 | $197 | $245 |

| 80 | $140 | $208 | $276 | $345 |

| Age | $10,000 | $15,000 | $20,000 | $25,000 |

|---|---|---|---|---|

| 55 | $28 | $40 | $52 | $64 |

| 60 | $33 | $48 | $63 | $77 |

| 65 | $41 | $60 | $79 | $98 |

| 70 | $53 | $78 | $103 | $128 |

| 75 | $72 | $107 | $142 | $176 |

| 80 | $98 | $146 | $194 | $241 |

Rates shown are sample monthly premiums from Mutual of Omaha for non-tobacco applicants. Applying does not guarantee approval.

Why These Are Averages, Not Quotes

Averages are useful for ballpark planning, but they are not a price tag. Each insurer applies its own underwriting criteria, so the same applicant can get meaningfully different quotes for identical coverage.

Your actual number depends on your specific profile, the carrier’s rules, and the rate environment at the time you apply. The rest of this page explains why that variation exists and how to leverage it to your advantage.

The Factors That Determine What You’ll Pay for Final Expense Insurance

A handful of variables move your rate. Below is a brief explanation of each,

Age at Application

Age is the single biggest factor in what you pay for funeral insurance. Premiums climb gently through your 50s and 60s, then accelerate sharply in your 70s and 80s.

The steepest jump in the data falls between ages 75 and 80, where average rates rise about 44 percent for women and 45 percent for men. Because the rate locks in at the age you apply, buying earlier means a lower premium for the life of the policy. There’s a deeper look at this in the How Costs Change by Age section further down this page, along with pages for each decade.

Gender

Men and women are priced differently for the same coverage. Women typically pay roughly 15 to 30 percent less than men of the same age because women live longer on average, which lowers the insurer’s risk.

This is built directly into the rate rather than being something you can shop for. One exception worth knowing: Montana law requires insurers to charge men and women the same life insurance rates.

Tobacco Use

Tobacco status raises your rate, since insurers treat it as a higher health risk. The surcharge commonly runs about 30 to 60 percent above non-tobacco rates, though some analyses show a smaller gap, closer to 25 to 30 percent, depending on the carrier and your age.

What counts as a “tobacco user” and how far back a carrier looks both vary. Most insurers ask whether you’ve used tobacco in the past 12 months, while some look back two to three years. If you’ve recently quit, this matters a great deal, and the tobacco rate guide covers definitions, look-back windows, and re-rating after you stop.

Health and Medical History

Final expense insurance skips the medical exam, but your health still shapes both your price and which plan tier you qualify for. You answer a short health questionnaire, then the carrier runs a prescription database check and an MIB (Medical Information Bureau) review to confirm your answers, usually in minutes.

Carriers differ a lot in how they treat specific conditions. Some are lenient with diabetes and COPD, while others are strict. Conditions like diabetes, COPD, heart disease, and a cancer history are exactly where carrier choice and accurate answers matter most, and the health and conditions guide covers each one in detail.

Coverage Amount

The more coverage you buy, the higher your premium in absolute dollars. But the cost per dollar of coverage usually drops a little as the benefit amount increases, because the carrier’s fixed policy fee is spread across a larger benefit.

That can create small pricing quirks worth catching. In one 2026 analysis, the step from $25,000 to $30,000 added only about $7 a month, the smallest jump in the data. The “How Much Coverage You Need” section below walks through choosing the right amount, with a page for each coverage tier.

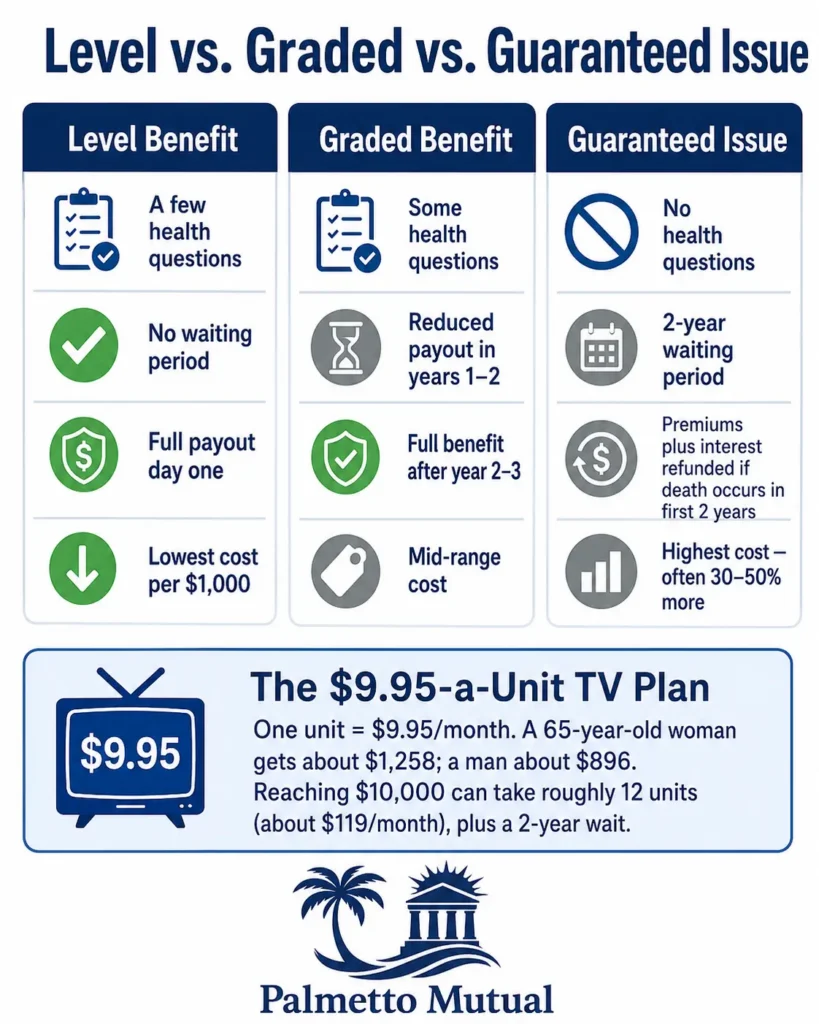

Plan Type (Whole Life, Graded Benefit, Guaranteed Acceptance)

The plan tier you qualify for has a large effect on price. Level benefit whole life is the cheapest per dollar and pays the full benefit from day one, but it requires reasonably good health.

Graded benefit costs more and limits the payout in the first couple of years. Guaranteed acceptance is the most expensive per dollar and asks no health questions, but it carries a waiting period. In one 2026 comparison, a guaranteed issue policy cost about 42 percent more than simplified issue for a 70-year-old man seeking $10,000 — roughly $99 versus $70 a month. Each tier has its own page: level/whole life, graded benefit, and guaranteed acceptance.

Carrier Selection

The same person can get very different prices from different companies. Two applicants with identical profiles often see rates that differ by 25 to 60 percent between carriers, and sometimes more, because each company has its own underwriting niches and pricing strategy.

This is why shopping multiple carriers matters so much with funeral life insurance. In a 2026 review of 50-year-old applicants, the gap between the cheapest and most expensive company was about $22 a month for women and $27 for men on a $10,000 policy. There’s a full breakdown of how carrier choice plays out further down the page.

How Much Coverage Do You Actually Need?

The right coverage amount isn’t a guess. It comes from matching your death benefit to the real costs your family will face.

How to Think About Coverage Amount

Start with three simple questions. What kind of funeral or service do you want? What debts and end-of-life bills would you leave behind? And do you want to leave anything extra for your family beyond covering those costs?

Where those three answers meet is your coverage amount. The sections below help you put real numbers to each one.

Anchoring on Funeral Costs

Your first anchor is the funeral itself, and costs vary widely by the type of service. Here are the current 2026 national ranges, drawn from National Funeral Directors Association data and major funeral-cost surveys.

| Type of Service | Typical 2026 Cost |

|---|---|

| Direct cremation (no service) | $1,500 – $3,000 |

| Cremation with a memorial service | $4,000 – $7,000 |

| Traditional burial with viewing | $9,000 – $12,000 |

| Premium or high-cost-area burial | $15,000 – $25,000+ |

The NFDA median for a funeral with viewing and burial is around $8,300 for funeral-home services alone, and the total typically reaches $11,000 to $13,000 once you add a cemetery plot, headstone, flowers, and a reception. Where you live matters a great deal, since Southern and Mountain West states often run well below the national median.

Beyond Funeral Costs — What Else the Death Benefit Should Cover

The funeral is rarely the only bill. Many families also face leftover costs that the death benefit can absorb.

End-of-life medical bills are common even with good insurance. In one federal analysis, nearly 4 million adults age 65 and older had unpaid medical bills, and about 70% had 2 or more sources of coverage. Residual hospital, hospice, and care costs often land in the low thousands to the low five figures.

Consumer debt is another piece. Seniors over 65 carry average credit card balances of roughly $4,000 to $5,000 each, so a household can easily hold $5,000 to $10,000 in consumer debt. Beyond that, family travel for a funeral can run $1,000 to $3,000 or more, and a surviving spouse may need a few months of mortgage or household support during the transition.

Coverage Amount Recommendations and What Each Tier Covers

Here’s a quick guide to who each coverage amount tends to fit.

A $5,000 policy is entry-level, best suited to someone planning a direct cremation with little else to cover. A $10,000 policy is the most common choice and covers a modest funeral with a little room to spare. A $15,000 policy gives comfortable, comprehensive coverage for a traditional burial plus some leftover bills.

A $20,000 policy adds a real cushion for debts and family support, in addition to the funeral. A $25,000 policy starts to cross into small-legacy territory, leaving something behind after costs. A $30,000 policy is squarely legacy planning rather than pure final expense.

At $40,000 and $50,000, you’re at the outer edge of this product, and many buyers at that level are better served by a different type of policy. An honest agent will tell you when you’ve outgrown burial insurance.

When You Should Consider More Coverage Than You Initially Thought

Many people start at $10,000 because it sounds sensible, then reconsider once they see the real numbers. After reading regional funeral costs and adding in leftover medical bills and debt, $15,000 or $20,000 often fits the actual need better.

There’s no pressure here, just arithmetic. If your funeral plans and outstanding costs exceed your starting figure, it’s worth pricing the next tier up before you decide.

When You Should Consider Less Coverage Than You Initially Thought

Overbuying is just as real a mistake. A shopper who picks $50,000 but actually plans a direct cremation is paying for coverage that doesn’t match the plan.

The same goes for a $30,000 buyer with no dependents who would be well covered at $15,000. If a larger amount would strain your monthly budget without serving a clear purpose, a smaller policy you can comfortably keep for life is the better choice.

How Final Expense Costs Change by Age

Age is the primary factor that affects your premium. This section shows how the curve behaves and what each decade looks like in practice.

The Final Expense Pricing Curve by Age

Final expense premiums don’t rise in a straight line. They climb gently through your 50s and 60s, then steepen noticeably in your 70s and accelerate hard in your 80s.

The jump from age 70 to 80 roughly doubles the premium for the same coverage, and the single sharpest increase occurs between ages 75 and 80, where average rates rise by about 44 to 45 percent. Because your rate locks in at the age you apply, that curve is the core reason buying earlier saves money for the life of the policy.

Average Monthly Rates by Age for Common Coverage Amounts

This table tracks the age progression for the three most common coverage amounts, based on a healthy, non-tobacco profile. It’s the same underlying data as the matrix earlier on the page, arranged to show the climb by age.

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 55 | $36 | $52 | $69 |

| 60 | $44 | $64 | $84 |

| 65 | $56 | $83 | $110 |

| 70 | $75 | $110 | $146 |

| 75 | $100 | $148 | $197 |

| 80 | $140 | $208 | $276 |

| Age | $10,000 | $15,000 | $20,000 |

|---|---|---|---|

| 55 | $28 | $40 | $52 |

| 60 | $33 | $48 | $63 |

| 65 | $41 | $60 | $79 |

| 70 | $53 | $78 | $103 |

| 75 | $72 | $107 | $142 |

| 80 | $98 | $146 | $194 |

Rates shown are sample monthly premiums from Mutual of Omaha for non-tobacco applicants. Applying does not guarantee approval.

Final Expense Insurance in Your 50s

Your 50s are the planning-ahead decade. You’ll see the healthiest underwriting, the lowest rates, and the longest runway of level premiums.

One thing worth checking at this age: if you have a temporary need, such as a mortgage or dependents, term life insurance may be a better fit than burial insurance. There’s deeper guidance on this stage for final expenses on the final expense in your 50s page.

Final Expense Insurance in Your 60s

The 60s are the heart of the market, where most people actually buy. Underwriting is still favorable, rates are still reasonable, and the need starts to feel real.

This is often the sweet spot for locking in a level benefit policy at a comfortable price. The final expense in your 60s page covers the decade in detail.

Final Expense Insurance in Your 70s

The 70s are the narrowing-options decade. Premiums climb noticeably, more applicants get steered toward graded benefit plans, and choosing the right carrier matters more than ever.

The math of total premiums paid also starts to matter here. The final expense in your 70s page walks through how to navigate it.

Final Expense Insurance in Your 80s

The 80s are the qualify-if-you-can decade. Most insurers cap final expense and guaranteed issue policies at age 85, and some stop accepting new applicants at 80, so guaranteed acceptance becomes the default for many people.

At these ages it’s fair to ask whether a policy is still worth it, and family members often help pay the premiums. The final expense section on your 80s page covers the remaining options.

Why Locking In Coverage Earlier Saves Substantial Lifetime Premiums

Final expense insurance is whole life, so the premium locks in at your age when you apply and never changes. Waiting five or ten years to buy means a permanently higher premium, not a temporary one.

Waiting also carries a second risk: if your health declines during the wait, you could drop from a level plan to a graded or guaranteed issue plan, further raising the cost. For most people, buying sooner wins by a wide margin over the life of the policy. This is honest math, not a sales pitch — the right time to buy is when you have a real need and can comfortably afford the premium.

What Is the Cheapest Final Expense Insurance? An Honest Answer

“Cheapest” is the most-searched question in this space, and it deserves a straight answer rather than a sales hook.

The Cheapest Final Expense Insurance Depends on Your Profile

There is no single cheapest final expense product. The cheapest option depends on your age, gender, tobacco status, health, coverage amount, and which carrier underwrites your specific combination most generously.

Anyone advertising “the cheapest funeral insurance” is either oversimplifying or selling. The honest version of the question is: what’s the cheapest coverage available to me, specifically?

Realistic Paths to Lower Premiums

There are real, honest ways to lower your premium. The most direct approach is to choose a smaller coverage amount that still meets your actual needs.

Beyond that: qualifying for a better plan tier, since level benefit costs much less than graded or guaranteed issue for the same coverage; improving your underwriting profile by quitting tobacco or getting a chronic condition under control; and comparing multiple carriers, where the same applicant can see 25 to 60 percent rate variation. Avoiding a guaranteed-issue product when you’d actually qualify for level or graded coverage is often the single biggest saver.

Why TV-Advertised Final Expense Often Isn’t the Cheapest

The heavily advertised “guaranteed approval, no health questions” products are built to be the easiest path to a sale, not the cheapest path to coverage. The classic example is the $9.95-a-month plan sold on television.

That $9.95 buys one “unit” of coverage, and the per-unit cost shrinks with age. For a 65-year-old woman, $9.95 a month buys a death benefit of only about $1,258. To reach $10,000, a 65-year-old man would need roughly 12 units at about $119 a month, and he could often get a $20,000 to $25,000 policy elsewhere for a similar price.

The lesson is that ease of purchase and lowest premium are two different things. Many buyers who could answer a few health questions and get day-one coverage 20 to 65 percent cheaper instead default to the advertised guaranteed-issue plan.

When the Cheapest Option Isn’t the Right Option

Sometimes the rock-bottom premium comes with tradeoffs that cost more later. A bargain carrier might have weaker financial strength, fewer rider options, a longer waiting period, or a slower claims process.

The smarter question isn’t “what’s absolutely cheapest” but “what’s the best mix of price, plan tier, carrier strength, and features for my situation.” Day-one coverage from a solid carrier at a few dollars more is usually worth it over a cheaper plan with a two-year wait.

Where to Find the Cheapest Coverage for Your Specific Profile

Different profiles lead to different “cheapest” answers. Healthy buyers in their 50s and 60s usually find it through a level benefit whole life. Buyers with controlled chronic conditions often find it through graded benefit plans.

Buyers with disqualifying conditions may find their only option is guaranteed acceptance. Tobacco users have their own carrier-shopping considerations, and people with conditions like diabetes have specific paths. The cheapest answer for you depends on which path applies, and the dedicated guides in this section cover each one in depth.

Frequently Asked Questions

About the Author

Dvir Mosche is an award-winning independent insurance agent and the founder of Palmetto Mutual, a trusted insurance brokerage specializing in Final Expense Life Insurance. Since entering the industry in 2017, he has been recognized multiple times as a top agent for his dedication to educating and assisting seniors in finding the proper coverage. His mission is to simplify the process, provide honest and personalized guidance, and ensure that every client gets coverage they can depend on for life.